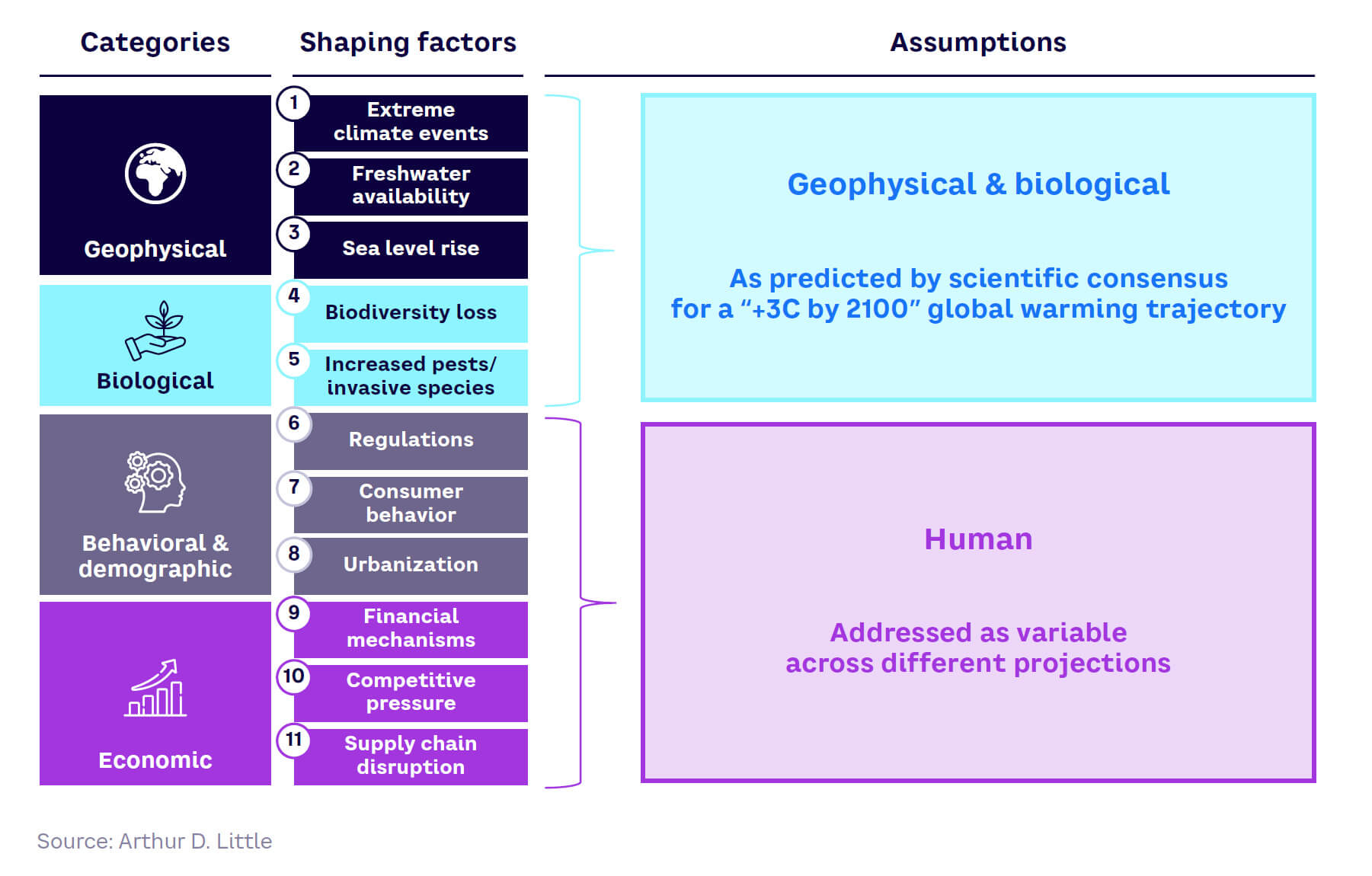

Based on our research and corroborated by our surveys and expert interviews, we have identified 11 shaping factors that affect climate change adaptation, grouped into geophysical, biological, behavioral/ demographic, and economic categories (see Figure 4).

Shaping factors for climate change adaptation

Geophysical

- Extreme climate events — phenomena outside the normal

range of weather patterns characterized by their severity,

duration, or frequency (e.g., heat waves, droughts, storms,

wildfires, landslides, and flooding) - Freshwater availability — a decrease in the amount of clean

and usable water accessible for human use and consumption - Sea level rise — an increase in the average level of the

ocean’s surface over time, due to melting glaciers and thermal

expansion of seawater, leading to the erosion and submersion

of coastlines

Biological

- Biodiversity loss — a severe decline in yield from key crops and livestock, as well as mass vegetal and animal species extinctions

- Increased pests/invasive species — an increase in the activity of destructive insects and animals, leading to damage to ecosystems and possible transmission of diseases to humans

Behavioral & demographic

- Regulations — legislation and practices put in place by governments and local authorities to promote or impose adaptation to climate change

- Consumer behavior — patterns of individual purchasing decisions that reflect adaptation to climate change

- Urbanization — an expansion of cities and towns as populations migrate due to extreme weather, moving from rural to urban areas

Economic

- Financial mechanisms — an ecosystem of polices, investors, and financial instruments that mandate or promote adaptation investment

- Competitive pressure — major players in the value chain assuming climate adaptation leadership, driving a dynamic market and forcing behavior change onto competitors and suppliers

- Supply chain disruption — interruptions or significant slowdowns in the transportation and distribution of raw materials, resources, goods, and services

During our analysis, we assumed that factors within the geophysical and biological categories will behave in line with the “+3°C by 2100” global warming trajectory (see sidebar “The ‘+3°C by 2100’ trajectory”). However, the impact and scope of the behavioral/ demographic and economic categories will vary between the different projections outlined later in this chapter.

Impacts by category

Geophysical

The impacts of geophysical factors will be widespread and large-scale,

as evidenced by projections[4] and estimates from a variety of sources.

For example:

- Heat waves are likely to be longer and more intense over the coming decades, with minimum temperatures rising by at least

+3°C, and an accentuation of up to +8°C at the poles, according to the IPCC. Additionally, the combination of high temperature and high humidity is likely to become more prevalent, increasing the “wet bulb effect,” which limits the human body’s ability to cool down from evaporation or sweat.

The “+3°C by 2100” trajectory

The “+3°C by 2100” trajectory falls within the confidence interval for the IPCC’s RCP 6.0, which predicts a temperature increase of ~+2.8°C versus preindustrial levels, with a possible range between +2.0° and +3.7°C. This trajectory considers the likely target gap in 2030 based on current delays in policy and climate action at large. It therefore allows for a cautiously pessimistic outlook, which puts the challenges of adaptation for companies into sharper focus.

Global GHG emissions

A +3°C global increase by the end of the century is forecast to bring temperatures beyond +3°C above preindustrial levels in the second half of the century, as it is assumed temperature will peak before mitigation measures allow it to plateau and decrease. Treating the geophysical and ecosystemic/biological ramifications of global warming as givens helps make impacts concrete and solutions pragmatic. We purposely do not integrate the Shared Socioeconomic Pathways (SSPs) approach into our baseline temperature for projections, as we treat patterns of human development as uncertainties.

- Conditions will be more favorable for the formation of tropical cyclones, particularly affecting areas in the Pacific Ocean. For example, by 2050, the annual likelihood of an intense tropical cyclone in Japan is likely to more than double from 4.6% in 2020 to nearly 14%.[5]

- By 2040–2050, the likelihood of wildfire events will increase by nearly 30% globally, according to the IPCC, particularly due to higher temperatures causing vegetation — including rainforests, permafrost, and peatland swamps that would not usually burn — to dry out and combust.

- By the late 21st century, the share of the global land area and population affected by agricultural, ecological, and hydrological droughts is projected to increase substantially — from around 15% to 20% at a moderate or severe drought, and from around 3% to nearly 10% in the extreme or exceptional drought.[6] Some areas are more exposed to droughts, particularly Africa, South America, and the Mediterranean coast, which will see drought hazard increase by 82%.[7,8]

- Extreme precipitation events will be accentuated by climate change, increasing the risk of flooding, particularly in Southeast Asia. This will also lead to soil erosion due to extreme rainfall, a trend increasing over 80%-85% of the global land surface.[9] By 2050, experts project an increase in the frequency or intensity of precipitation events, especially in North America and Europe. In New York, annual rainfall is expected to increase from 45.6 to about 49.7 inches in that timeline.[10]

- As of 2022, 2.2 billion people lacked access to safely managed drinking water.[11] Other sources project that demand for water will rise by a further 20 to 25% by 2050.[12]

- The consequences of sea level rise will be global, with local variations in risks and damages. Some regions are more vulnerable than others; for example, 17% of Bangladesh is predicted to be submerged by 2050, displacing over 20 million people.[13]

Taking action on extreme heat

Exposure to extreme heat results in more deaths than any other climate-related hazard, and the impacts are increasing. Rising global temperatures, primarily caused by climate change due to GHG emissions, are leading to more frequent and severe heat waves. Alongside the impact on human health, heat waves also affect economies and infrastructure and can compound other climate and non-climate risks, such as drought and wildfires. The threat of extreme heat will continue to increase, and by 2030, between 160 million and 200 million people in India could live in regions with a 5% average annual probability of experiencing a deadly heat wave that exceeds the “survivability threshold” for a healthy human being. Extreme heat’s impacts on human health and the economy are unequal and vary depending on vulnerability and exposure. People with chronic diseases, older people and the very young, low-income individuals, underserved populations, people living alone, pregnant women, and unhoused people are most at risk to extreme heat. While extreme heat can occur in most populated areas, the intensity is accentuated in urban areas, with dense populations and economic activity. Moreover, extreme heat exposes populations to multiple negative outcomes, impacting health, the workforce, productivity, and transportation. Extreme heat can compound or even instigate other climate-related risk events. Creating resilience in economies and communities is a necessity, but it is also an opportunity. Heat resilience stands as a pivotal opportunity for global corporations and organizations of all sizes to innovate and help society adapt. Extreme heat mitigation and adaptation is a great chance for innovation that benefits society and brand image and should be prioritized by forward-looking chief risk, innovation, and finance officers. (Read more from Climate Resilience Consulting’s Joyce Coffee and Robert Macnee on extreme heat in the Appendix.)

Biological

A variety of biological factors will impact ecosystems, farming, and the spread of infectious diseases, such as:

- Crop and livestock productivity decline and biodiversity loss attributed to climate change are already endangering the whole range of “ecosystem services.” Maize yields, for example, are projected to decline further by 24% by the late 21st century, even as the global demand for cereal for animal feed and food alone is expected to increase by 50%-60% compared to 2000.[14]

- A global increase is predicted in crop pest damage to wheat, rice, and maize production of 10%-25% per degree of global warming.[15]

- The threat of zoonotic disease transmitted between vertebrates and humans is increasing dramatically due to the disruption of natural habitats by climate change (and other human factors like deforestation and urbanization). A greater probability of mosquito-borne West Nile Virus infection is expected in 2025, especially in eastern Croatia, northeastern Türkiye, and northwestern Türkiye, with further range expansion in 2050.[16]

Behavioral & demographic

The way humans react to climate change determines profound

political, demographic, and societal trends:

- Regulation has so far been the major lever in climate change mitigation efforts. However, for adaptation, while there have been some regulations in place since 2008 (see Table 1), they are still sparse, limited to specific industries, and lacking in enforcement power. Whether regulation will ever drive adaptation with the same force as mitigation is very much open to question.

- While consumers in industrialized countries show some signs of behavioral shifts related to climate change adaptation, counteradaptation behavior is also being seen. For example, in the US real estate market, homes near sea level rise areas are now sold for, on average, 7% less than comparable homes.[17] Yet at the same time, population growth is strong in the hottest, driest, and most vulnerable parts of the country. As an example, more than 800,000 people have moved from California to Phoenix, Arizona, since 2012.[18]

- Urbanization rates are expected to keep increasing, further boosted by the influx of refugees from affected areas, particularly in the Global South, where 70% of those displaced by climate change are moving to cities.[19]

We consider regulation and behavioral shifts in more detail in the next section.

Economic

- Climate change will profoundly impact key economic drivers on a global scale, with tangible effects on businesses. Financial mechanisms for adaptation are in development, spearheaded by international development institutions, with insurance particularly active. However, while adaptation finance for climate change hit a record $63 billion in 2021/2022, increasing by 28%, it is still significantly below the $212 billion yearly need projected by 2030 for developing countries alone.[20]

- Industry leaders have transformed entire supply chains with their climate-mitigation efforts, pressuring customers and competitors to change. For example, Apple is demanding that its entire value chain reduce its impact on global warming.

- Supply chains are likely to be disrupted by rising sea levels and other factors, potentially leading to major changes in global economic structures. For example, severe droughts have limited transits through the Panama Canal to 25 per day (down from 36) since January 2024, causing significant supply chain delays and repercussions on costs.[21]

- Commodity prices are highly volatile due to market conditions, and future supply chain disruptions could significantly increase them. For example, cocoa market prices increased dramatically in 2023 due to heavy rainfalls in West Africa.

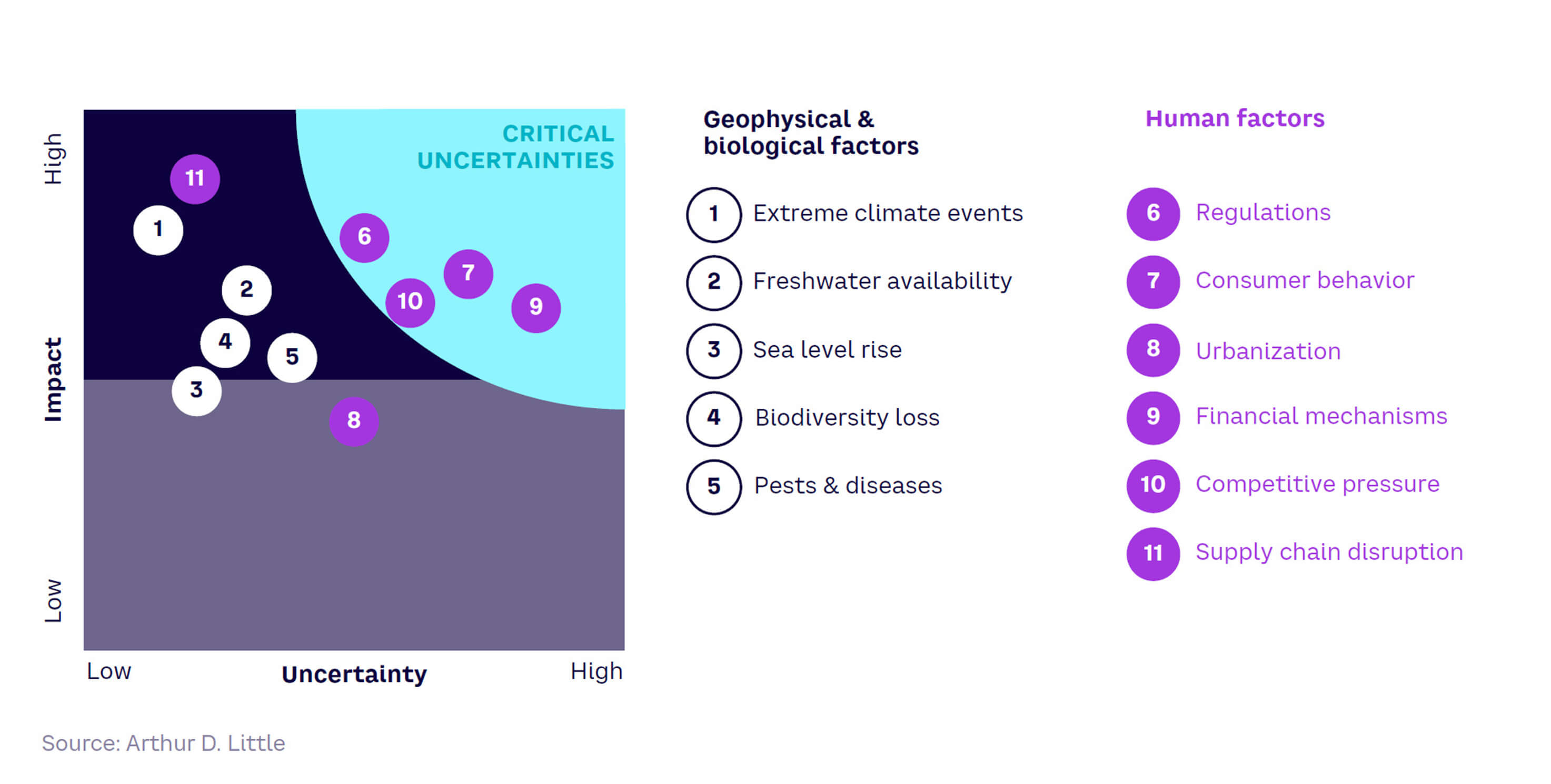

The impact of human shaping factors

In our analysis, we captured all the geophysical and biological factors (1-5 in Figure 4) as part of our underlying assumption of a “+3°C by 2100” trajectory, effectively taking these factors as a given. To explore plausible futures, we scored the “human shaping factors” (6-11 in Figure 4) according to their impact and degree of uncertainty, using the results of a survey polling 60 experts and corporate executives (see Figure 5). In the matrix:

- A maximum degree of uncertainty (scored 5 out of 5) refers to a 50/50 probability of a particular factor being realized. Conversely, a score of 1 out of 5 reflects near certainty.

- Impact is a qualitative appraisal of the intensity and range of consequences of a particular factor on societies, businesses, and humans. A score of 5 out of 5 reflects very high impact across the board, while 1 out of 5 reflects little or no impact.

The factors that gained the highest scores of uncertainty and impact, placing them in the top right-hand quarter of the matrix, constitute “critical uncertainties.” These comprise regulations, consumer behavior, financial mechanisms, and competitive pressure. Supply chain disruption has relatively high certainty and major impact and was thus integrated as a given into all the future projections. Urbanization has relatively less impact than the other factors, so it was deprioritized in the analysis.

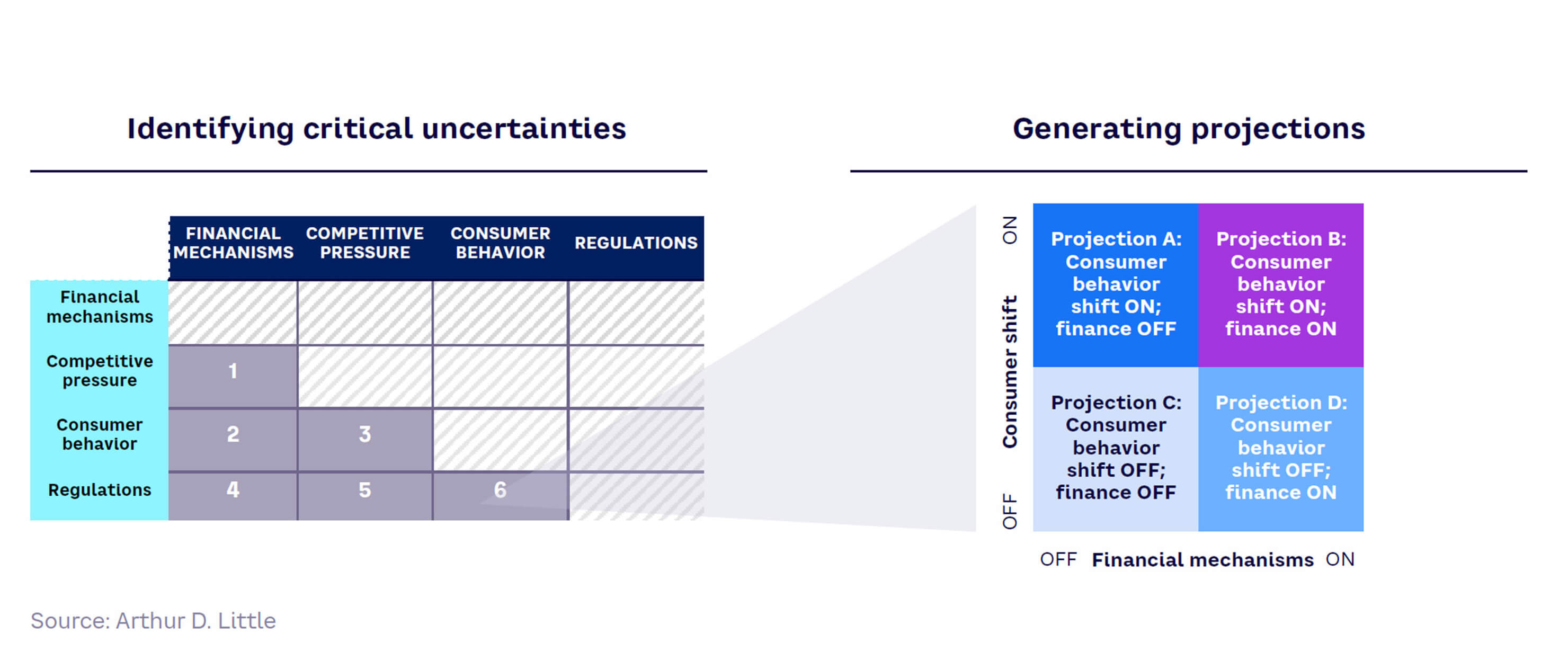

The projection methodology

To build our future projections, we followed a structured methodology (see Figure 6). The methodology comprised four steps:

- Rank the four critical uncertainties listed in Figure 5.

- Identify intersections between these uncertainties.

- Generate on/off projections for the intersections between the four critical uncertainties.

- Filter the resulting 24 projections down to five, considering:

- Plausibility. Is this scenario internally consistent, or is it self-contradictory?

- Differentiation. Is it sufficiently differentiated from others to tell us something new?

- Technological relevance. Does this scenario enable us to predict which technologies will be useful for adaptation?

This approach yields projections not strictly exclusive of each other, as each only highlights two aspects of the future. Projections may be compatible in a single world (e.g., there is a single possible world with high levels of regulation, high competitive pressure, low consumer behavior shift, and low financial resources available). However, our approach addresses this result in two separate projections. We believe this approach more closely mimics realworld decision-making than multivariate scenario-building, which often proves an intractable exercise, especially when each variable displays high degrees of uncertainty. Additionally, this approach allows for thoroughly exploring the tension that arises at the confluence between shaping factors, demonstrating clearly where contradictions, challenges, and opportunities arise.

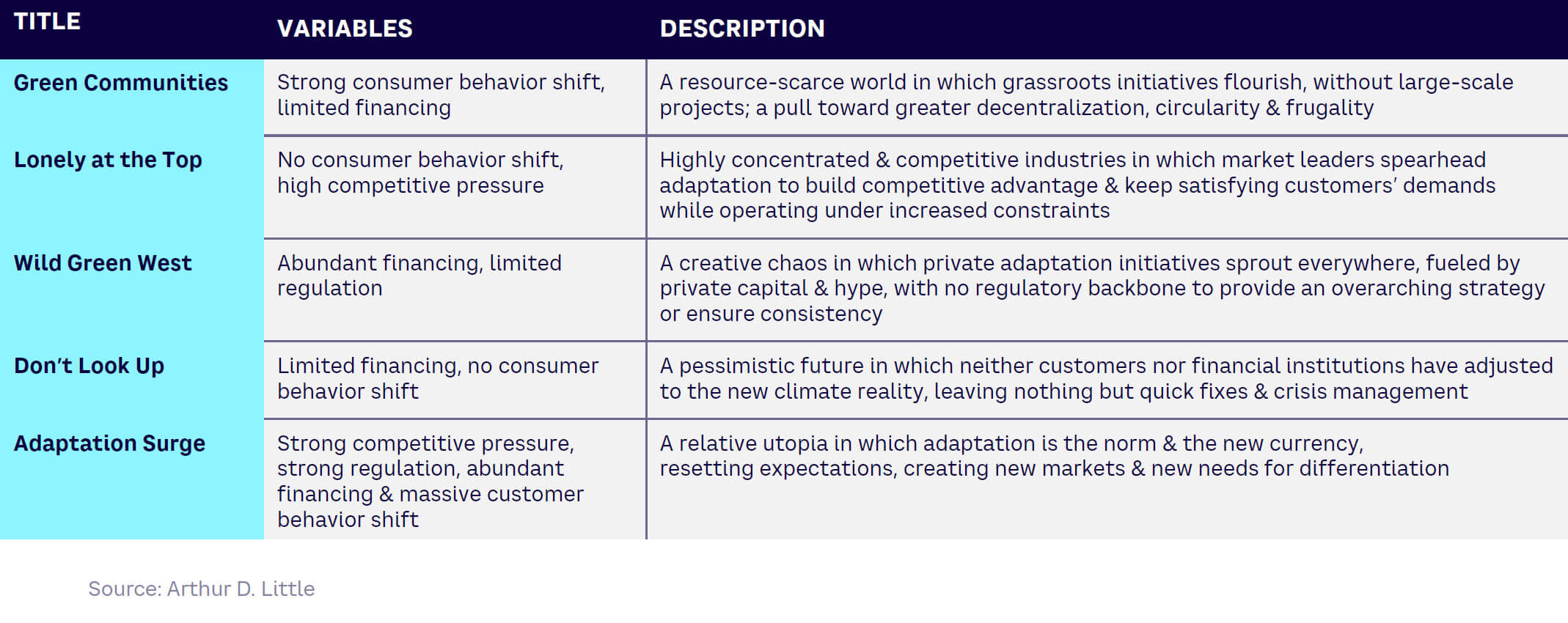

5 projections for the future

Through this process, we have identified five projections, chosen for their internal consistency, differentiation, and relevance for technology (see Table 2). With the help of our design fiction partner Making Tomorrow, in this section we share “artifacts from the future” based on the five projections.

Projections

Using our projection methodology and identifying featured projections based on plausibility, differentiation and technology relevance, we have identified 5 featured projections.

Click on the featured projection to read in detail about this potential future.

Scenario Quadrants

How did we get there?

- In response to recent climate catastrophes, governments worldwide enacted strict adaptation regulations like prohibiting construction in vulnerable costal areas to mitigate further damage, as well as increased demand from consumers on adaptation measures

- Aiming at supporting adaptation projects, public sector unlocked some funding, but it is still not sufficient and requires the support of the private sector

international economy

- Characterized by increased globalization in the form of cooperation on climate initiatives and technology exchange and an increased state intervention focusing efforts and resources on climate adaptation

- Disparities between North and South still exist with an inequal access to financial resources but the South being crucial for agriculture and electronics, new ways of cooperations are developed and knowledge is shared, and large metropolis are primary laboratories for adaptation

Societies

The relative alignment between business leaders and the public creates a catalyst for change, with change in daily life and basic need: food production relies on lab-grown meats and vertical farming to limit land use and water consumption, remote and digital collaboration is predominant, electrification has spread among cars and trains.

Winners & Losers

- Success stories are found in risk-takers companies rapidly developing climate adaptation technologies, benefiting particularly the food and infrastructure industries, some companies (e.g., Nestlé) achieving near-monopoly status

- As it is an extreme race, less innovative firms or the ones too slow struggle. Industry stuck in a pattern of “maladaptation” decline leading to entire regions to collapse (e.g. textile in Bangladesh)

Cultural shifts

- Sobriety, localism and resiliencies the trend in modes of consumption

- Sourcing of raw materials is affected by stricter environmental regulations and consumer behavior shifts. Information and traceability technologies enable significantly reduction in food waste

- Farming practices adapt to biodiversity loss and water shortage and develop water management systems & lab-grown techniques

- Industries reliant on mineral extraction are facing stricter regulations on environmental impact, leading to limitations in raw material use

- Geo/climate-engineering techniques are developed to increase productivity of crops

- Manufacturing processes are redesigned and now involve adaptation tech (digital twins, predictive analytics), which requires an upfront investment but leads to long-term savings

- Driven by consumer demand and regulations, the textile industry shift to a closed-loop manufacturing process using circular economy to minimize waste and water usage

- Due to increased heatwaves, working hours have been adapted in exposed industries (e.g. construction)

- To limit operation interruptions and productivity loss, firms invest in technologies securing energy supply (e.g. retractable solar panels)

- Insurances develop more sophisticated risk assessment models and push through incentives for climate resilience infrastructure leading firms to invest in protective measures of their assets

- Public investments increase in protecting densely populated areas & industrial hubs, by building major infrastructures, such as sea-walls

- Businesses are relocating their assets in less exposed areas of floodings or hurricanes

- New built plants/assets are resilient to extreme climate events

- In this extreme race for adaptation, the focus is on the speed of development of technologies. Market leaders invest in talents and set the pace for innovation forcing rivals to keep up or risk obsolescence

- Firms adapt to the shift in consumer preferences for "climate appropriate" goods and product differentiation is essential

How did we get there?

- In response to recent climate catastrophes, governments worldwide enacted strict adaptation regulations like prohibiting construction in vulnerable costal areas to mitigate further damage, as well as increased demand from consumers on adaptation measures

- Aiming at supporting adaptation projects, public sector unlocked some funding, but it is still not sufficient and requires the support of the private sector

international economy

- Characterized by increased globalization in the form of cooperation on climate initiatives and technology exchange and an increased state intervention focusing efforts and resources on climate adaptation

- Disparities between North and South still exist with an inequal access to financial resources but the South being crucial for agriculture and electronics, new ways of cooperations are developed and knowledge is shared, and large metropolis are primary laboratories for adaptation

Societies

The relative alignment between business leaders and the public creates a catalyst for change, with change in daily life and basic need: food production relies on lab-grown meats and vertical farming to limit land use and water consumption, remote and digital collaboration is predominant, electrification has spread among cars and trains.

Winners & Losers

- Success stories are found in risk-takers companies rapidly developing climate adaptation technologies, benefiting particularly the food and infrastructure industries, some companies (e.g., Nestlé) achieving near-monopoly status

- As it is an extreme race, less innovative firms or the ones too slow struggle. Industry stuck in a pattern of “maladaptation” decline leading to entire regions to collapse (e.g. textile in Bangladesh)

Cultural shifts

- Sobriety, localism and resiliencies the trend in modes of consumption

- Sourcing of raw materials is affected by stricter environmental regulations and consumer behavior shifts. Information and traceability technologies enable significantly reduction in food waste

- Farming practices adapt to biodiversity loss and water shortage and develop water management systems & lab-grown techniques

- Industries reliant on mineral extraction are facing stricter regulations on environmental impact, leading to limitations in raw material use

- Geo/climate-engineering techniques are developed to increase productivity of crops

- Manufacturing processes are redesigned and now involve adaptation tech (digital twins, predictive analytics), which requires an upfront investment but leads to long-term savings

- Driven by consumer demand and regulations, the textile industry shift to a closed-loop manufacturing process using circular economy to minimize waste and water usage

- Due to increased heatwaves, working hours have been adapted in exposed industries (e.g. construction)

- To limit operation interruptions and productivity loss, firms invest in technologies securing energy supply (e.g. retractable solar panels)

- Insurances develop more sophisticated risk assessment models and push through incentives for climate resilience infrastructure leading firms to invest in protective measures of their assets

- Public investments increase in protecting densely populated areas & industrial hubs, by building major infrastructures, such as sea-walls

- Businesses are relocating their assets in less exposed areas of floodings or hurricanes

- New built plants/assets are resilient to extreme climate events

- In this extreme race for adaptation, the focus is on the speed of development of technologies. Market leaders invest in talents and set the pace for innovation forcing rivals to keep up or risk obsolescence

- Firms adapt to the shift in consumer preferences for "climate appropriate" goods and product differentiation is essential

How did we get there?

- Not all customers are feeling the heat yet, those who are not constrained to adapt, especially the wealthiest in developing countries, do not. Insurance has not caught up, public funding for adaptation in developing countries remains limited, and private funding (inc. PE) remains largely limited to projects profitable in the short term.

International economy

- Central banks struggle to curb inflation as prices of raw materials rise. International division of labor remains in place, apart for a handful of critical materials subject to state intervention such as semiconductors. Local solutions are deployed in climate vulnerable regions with access to capital such as the ME, but do not propagate elsewhere

Societies

Societies remain stuck on the brink of widespread change.

Policies that promote both solidarity and climate adaptation have not been

developed, hence resistance remains widespread, especially among groups

who feel the brunt of the risk: farmers, hospitality workers, workers in

vulnerable industries or locations, disenfranchised urban populations.

Greater inequality gaps form between those who can afford price increases,

and those (still in the minority) who must radically change lifestyles - e.g.,

live without a car and limit their mobility as a result. The disappearance of

entire communities, towns and landscapes due to fires, hurricanes and sea

level rise create large-scale trauma and challenging migration flows, both

within and across countries.

Winners & Losers

Asset-light companies in the digital realm, companies

whose production facilities are located in low-risk areas, reap benefits from

continuous production. Companies that have already regionalized their

production for regulatory reasons (e.g. life sciences) or transportation

constraints (e.g. manufacturers of large car parts, construction materials)

are more resilient. Manufacturers of commodity consumer goods (textile,

plastics), and smaller agricultural producers are immediately threatened.

Cultural shifts

- The public remains torn between adaptation to climate change and more pressing concerns, such as fighting inflation. Some efforts by regulators and some industry leaders remain insufficient to move the needle, feeding a sense of hopelessness and frustration

- Smaller agricultural producers are not protected by insurance and lack the funds to invest in protection or optimization improvements, face major consolidation

- Shortages and delays become a given – most companies focus on managing the disruptions, as they cannot afford to limit them

- Raw material substitution is often needed, requiring machines that can function with a broader range of inputs

- Only manufacturers whose industrial processes are very vulnerable to increased climate events introduce new/innovative changes in small scales

- Unable to finance large-scale asset protection projects, companies focus on limiting/controlling damages

- Preventative maintenance is also an area of focus, to avoid structures and machines breaking under climate pressures

- More focus is placed on selecting the right site when purchasing or building a new facility, according to multiple criteria. Datacenters, in growing demand, take the prime spots

- Increased demand on connectivity, satellite is encouraged over terrestrial means (fiber, cable) due to lower vulnerability

- Remaining affordable is the primary concern of many industries producing “middle of the range” products, esp. cars

- Lack of financing mechanisms cause lower readiness in key sectors, such as Pharma R&D for vaccines or drugs addressing climate-borne illnesses

How did we get there?

- A heightened awareness of climate change has dawned on consumers globally as a result of catastrophic climatic events and shortages. They have largely adapted their purchasing habits and lifestyles to current or impending climate impacts. The finance world has not evolved to take climate adaptation into account – with short-term ROI remaining the main objective and metric. Insurers refuse to insure large swathes of climate hazards

International economy

- Globalized flows of capital and goods are limited by geostrategic conflicts and supply chain disruptions – but no effort towards regionalization or localization is underway. The North-South division of labor remains largely in place, South East Asia and Central America’s hubs suffering from climate impacts. Lack of financial mechanisms for adaptation mean significant disruptions to production and loss of productivity, primarily concentrated in areas vulnerable to severe climate events

Societies

Frustration grows at the lack of investment deployed in what is perceived by most consumers and citizens as a critical strategic issue, as well as at the ensuing interruptions in service delivery and production of everyday necessities

Winners & Losers

- Businesses and industries that are very asset light (first and foremost, digital) or whose assets are located in low-vulnerability zones, gain a competitive advantage. Extraction industries (oil, mining), heavy industry (metals, chemistry), or manufacturing (automobile) and to some degree, telecommunications (cable over ground) in vulnerable regions are heavily hit – as relocation is not always possible or economical, and repairs are costly

Cultural shifts

- The seeming inability of existing financial mechanisms to address the climate adaptation fuels reflections around alternative models, including increasing levels of state intervention or radical approaches to property of means of production – but no successful attempts on a large scale

- Customers have adapted their demands, consuming more local and in-season produce, and less meat (in developed countries)

- Recycling of manufactured goods, especially electronics, is on the rise, partially relieving pressure on battery components and microchips

- Unable to invest, businesses have to substitute ingredients (e.g. rice for wheat), discontinue product lines or features (e.g. natural vanilla extract disappears), or alter performance

- Innovation in manufacturing is frugal, focuses on design-to-cost (as consumers’ expectations become more basic) and optimization of productivity

- Large overhauls in manufacturing processes can’t be financed, so any productivity improvements remain marginal and piecemeal

- Any gains in productivity are threatened by losses from climatic hazards, especially for industries that consume a lot of water (chemicals, nuclear), or whose processes are temperature and humidity sensitive (pharma)

- In the absence of insurance mechanisms, most industrial assets remain uninsured, causing regular interruptions in production

- Use of advance warning systems develops. Firms rely on crisis management measures to limit damage

- Entire geographies become unattractive for the deployment of new assets, including formerly attractive manufacturing regions

- Nature-based solutions (e.g., mangroves against freshwater salination) become increasingly attractive due to their low cost

- Scrappy ventures offering lower-cost solutions for “strategic adaptation” or mitigation of damages thrive, e.g., inflatable solutions to keep inventory dry should your warehouse be flooded

- Maintenance/repairs services thrive, occasionally supported by robots/drones that can operate in challenging weather conditions

- Recycling is supported by consumers and partially solves material scarcity issues but lacks financing to be economically viable; only local attempts are made

- The wellness and healthcare industries thrive by helping humans prevent and treat conditions caused by climate change (heat stroke, new epidemic diseases, etc.)

- Innovation to meet new customer demands is frugal, finds inspiration in traditional/ancestral techniques, e.g. adobe or cut stone for construction

- Consumption of digital services has evolved to account for the energetic cost of compute and storage – more efficient AI models are developed

How did we get there?

- Forward looking companies with cash reserves have prepared for the future, betting on a much broader societal and economic move towards adaptation. Consumers, however, have not kept up with that trend, largely due to competing priorities such as rising inequality and higher costs of living

International economy

- Globalized supply chains and international division of labor subsist, albeit disrupted by geopolitical conflicts and climate change impacts. Manufacturing hubs migrate to less vulnerable locations within countries (away from coasts and typhoon prone regions). Some industrial relocation (to developed countries) takes place, aided by generous government subsidies

Societies

With regards to many social structures such as labor, education, care, and family, a two-speed society emerges: some aspects have adapted to climate change in a nimble way, others have not.

Winners & Losers

- Consolidation in consumer goods industries (fashion, personal care…) as only firms with money to invest in adaptation survived. Leading companies reap the benefits of their adaptation investments and have locked in their suppliers, thus gaining competitve advantage

Cultural shifts

- In developed countries, there is a growing cultural polarization between those who embrace a shift in norms, lifestyle and consumption habits to and those who resist that shift – further feeding the “culture wars”

- Because customer demand for rare raw materials (e.g. rare earths for batteries, fruit, meat, dairy) has not adapted, ingenious ways to procure these goods are blooming (e.g. vertical farming)

- There is growing lobbying for synthetic biology in agriculture to help grow resilient species while meeting the unchanging preferences of consumers

- Constraints on manufacturing operations and processes in many sectors (automotive, electronic goods, pharma, F&B) have increased: manufacturers must demonstrate resilience to power cuts, resource and workforce shortages, or challenging working conditions (such as extreme heat)

- Manufacturers have to compromise on other metrics, including quality and price, leading to brand reputation issues

- Other manufacturing sectors (e.g. construction, military) that are globally integrated keep prioritizing productivity and profitability

- Services (e.g. personal care, education, hospitality, transportation) provided locally are not subject to the same demands – are therefore slower to adapt

- Disconnects between companies' visions & customer preferences have led to commercial failures (e.g. Tesla's amphibious car), making firms wary of disruptive product innovation

- In a world of fragmented demand, players benefit from serving strong affinity niches (e.g., red meat lovers): solutions that help sense contradictory demand signals in an accurate and timely manner become extremely valuable

How did we get there?

- Governments are still focusing on mitigation, with a fear of imposing further heavy costs on industries to adapt. This has led to a lack of rules/practices in place to promote or impose adaptation to climate change. We see a market-driven approach to climate change adaptation, with businesses voluntarily investing in adaptation to remain competitive

International economy

- Leading companies invest in advanced adaptation technologies to protect their businesses from extreme climate events disruptions. In contrast, poorer and more vulnerable regions (such as South-east Asia) struggle to access these funds, due to lack of strong institutions with the manpower, data and know-how necessary to structure bankable adaptation initiatives

- Business investments in climate change adaptation show benefits, but the lack of societal focus on equality and long-term planning results in reactionary measures with increased societal costs. This leads to most actions being short-term, increasing societal costs. Such costs not only burden communities but also impact private companies, hindering overall progress towards sustainable and inclusive growth

Societies

- A growing split emerges between generations: one prioritizing innovating new ways of living, while the other strives to maintain traditional lifestyles

- Dependence on government support diminishes, increasing the geopolitically inflammatory nature, with a lawless race for resources

Winners & Losers

- With the missing regulations, sectors with higher economic returns or strategic importance (such as agriculture, energy, and coastal real estate) receive more investment compared to others, neglecting crucial areas like biodiversity and public safety

Cultural shifts

The culture's focus on creativity as a catalyst for technological progress, in the absence of robust regulations, has led to ethical dilemmas and debates over moral standards. The consequences of unchecked innovation could have devastating effects, reshaping cultural and political mentalities

- The race to secure resources drives innovation in supply chain management, but also prompts concerns over resource monopolization and environmental degradation

- We are seeing companies investing in desalination infrastructure, to secure water availability, as well as local grids to secure productivity

- With support from local funds, larger agricultural businesses are investing in adaptation tech such as precision irrigation, vertical farming, sensors for monitoring

- Lack of regulations in adaptation are still discouraging innovations such as GMOs not allowed in EU

- We see creative adaptations in manufacturing processes to enhance their efficiency and productivity, mainly within industries with high raw material and/or electricity costs, such as heavy industries, automotive and production of metals and chemicals

- With higher prices on raw materials, manufacturing companies such as OEMs etc. need to focus on cost optimization in their production lines, such as reducing machine time, increase standardization, and improve resource efficiency

- Companies invest independently in protecting their assets, leading to a wide range of solutions with varying degrees of effectiveness, such as predictive weather tools, usage of advanced materials, etc.

- Nature-based solutions, whose ROI is challenging to quantify, are less likely to be supported by traditional financial strategies

- Industries that are directly engaged with adapting to climate impacts thrive and introduce new goods and services, such as construction industry specializing in resilient building tech., water mgmt. industry focusing on water conservation/recycling, and agriculture industry developing drought-resistant crops and precision agriculture technologies

Projection 1 - Green Communities

How did we get here?

A heightened awareness of climate change has dawned on consumers globally following catastrophic climatic events and shortages. This has led them largely to adapt their purchasing habits and lifestyles to cope with current or impending climate impacts. However, the investment world has not evolved to take climate adaptation into account, due mainly to its lack of adequate short-term ROI. Insurers either require highly inflated premiums or else refuse to insure large swathes of climate hazards.

The international economy

Globalized flows of capital and goods are limited by geostrategic conflicts and supply chain disruptions. The North-South division of labor remains largely in place, while Southeast Asia’s and Central America’s hubs suffer greatly from climate impacts. A partial re-localization of supply chains takes place, and local means of production develop. The lack of financial mechanisms for adaptation means there are significant disruptions to production and consequent losses in productivity, primarily concentrated in the areas most vulnerable to severe climate events.

Society

Frustration grows at the lack of investment in what is perceived by most consumers and citizens as a critical strategic issue (adaptation), as well as at the ensuing interruptions in service delivery and production of everyday necessities.

Winners & losers

Businesses and industries that are very asset-light (first and foremost digital players) or whose assets are located in low-vulnerability zones gain a competitive advantage. Extraction industries (oil, mining), heavy industry (metals, chemistry), or manufacturing (automotive) — and to some degree, telecommunications delivered through overhead lines in vulnerable regions — are heavily hit, as moving assets is not always possible or economically viable, repairs are costly, and there are no funds for large-scale adaptation projects to shield infrastructure.

Cultural shift

The seeming inability of existing financial mechanisms to address climate adaptation drives a move to alternative models, including increasing levels of state intervention and radical approaches to ownership of the means of production. However, none of these are successful on a large scale.

Impact on the source/make/protect/sell model

-

Source. Customers have adapted their demands to consume more local, seasonal produce and less meat in developed countries. Recycling of manufactured goods, especially electronics, is on the rise at a local level, partially relieving pressure on sourcing battery components and microchips. Unable to invest in adaptation due to a lack of finance, businesses must substitute ingredients (e.g., rice for wheat), discontinue product lines or features (e.g., natural vanilla extract disappears), or alter the performance of products.

-

Make. Innovation in manufacturing is frugal, focusing on design-to-cost (as consumer expectations become more basic) and optimizing productivity. Major changes to manufacturing processes can’t be financed, so any productivity improvements remain marginal and piecemeal. Any productivity gains are threatened by losses from climate hazards, especially for those industries that consume a lot of water (chemicals, nuclear) or whose processes are temperature- and humidity-sensitive (pharmaceuticals). At the same time, scrutiny from climate-conscious customers grows, imposing reputational constraints on operations.

-

Protect. Many industrial assets remain uninsured, causing regular interruptions to production while they are fixed. Advanced warning systems are increasingly used, while businesses rely on crisis management measures to limit damage. Entire geographies, including former manufacturing hubs, become unattractive for the deployment of new assets, while nature-based solutions (e.g., planting mangroves to combat freshwater salination) become increasingly attractive due to their low cost.

-

Sell. Scrappy ventures offering lower-cost solutions for “strategic adaptation,” or damage mitigation thrive, such as companies providing inflatable solutions to keep inventory dry when warehouses flood. Maintenance/repair services flourish, occasionally supported by robots/drones that can operate in challenging weather conditions. Recycling is supported by consumers, partially solving material scarcity issues, but a lack of financing prevents fully fledged, large-scale circular economies from developing. The wellness and healthcare industries grow by helping humans prevent and treat conditions caused by climate change (e.g., heat stroke and new epidemic diseases). Frugal innovation finds inspiration in traditional/ancestral techniques (e.g., using adobe or cut stone for construction). The consumption of digital services has evolved, with more efficient AI models developed to reduce the energy costs of computing and storage.

Green Communities: Sowing sustainable seeds for success

It is 2040, and the food and beverage industry is one of the first sectors to be significantly impacted by climate change. Volatile crop pricing and performance, frequent shortages, and disrupted value chains are causing major challenges. Consumers have largely adapted to the new climate reality — partly by choice, partly due to price constraints — and are pulling through new product trends and climate-related requirements, in particular an increased focus on food miles or embodied carbon. Consumer preferences are driving a love away from carbon-inefficient uses of land, such as extensive cattle farming for beef and dairy. Meanwhile, moves to decouple food production from climate threats are stalling, as the large-scale funds necessary for technologies such as indoor farming remain limited.

How will the food and beverage industry survive this tension? At least four levers stand out: (1) partnerships along value chains, (2) climate-conscious product development, (3) synthetic biology (SynBio), and (4) increased responsiveness to fragmented consumer trends, including new ways of using land, crops, and animals (and how we value them).

Unlike the pharmaceutical industry, the food industry is not a monolith but a complex, global network of people and organizations. Lack of funds for large scale solutions can be remedied, partially, by careful collaboration across players in agrifood value chains. These relationships, particularly between large processors and farmers, like the Cargill Regenerative Agriculture Program launched back in 2019, need to mature to ensure resilience in the face of climate change and are only possible where direct relationships between the producer and user have been cultivated. Data sharing and analysis along the supply chain plays a crucial role in allowing retailers and consumers to make climate-positive choices. By 2040, this means the free and open sharing of complete information on growing practices, processing steps, and shipping and transport history for all ingredients, based on automated systems at every stage in the supply chain.

Product development is also a key lever for adaptation to climate change. Companies must adjust their recipes to locally available ingredients, especially when customers request ingredients with low or zero “food miles.”[1] Substitution may be achieved by identifying third-party manufacturers with similar formulations to safeguard against short-term ingredient shortages rather than changing existing recipes and lines. Regardless, such changes require a robust supply quality assurance system, which invokes further supply chain regionalization. Under this paradigm, increasing “air miles” to source ingredients that meet requirements (e.g., flying Kenyan green beans to Europe for freshness) is no longer an option. (For more on this topic, read the ADL Viewpoint “Strengthening Resilience in Food & Beverage Product Development“.) Climate change–induced shortages brought about by droughts or extreme weather events (e.g., Californian almonds in 2022 or Canadian mustard seeds in 2023) demonstrate the need for food and beverage companies to be proactive in securing resilient supply chains. As droughts and storms become more intense and frequent, these shortages pose even greater challenges.

SynBio, currently used in the pharmaceutical industry, could trickle down to the food industry as costs decrease and scale increases. Gene editing could accelerate breeding, particularly for high-value crops like drought-resistant tomatoes. Biotechnology companies such as Pairwise, Tropic Biosciences, or AgBiome are at the forefront of such developments but face regulatory hurdles in the short term and funding challenges in the Green Communities projection. In a more fruitful turn of events, one could see the development of a “return to roots” with the reintroduction of heritage vegetable and fruit varieties, once outcompeted on productivity, price, homogeneity, or (occasionally) taste, but now hailed for their climate resistant properties, such as the drought-tolerant Hopi corn in the Southwestern US.

Although consumers are adapting to climate change, aggregate behavior is nuanced and seemingly contradictory in parts. While the trend toward reduced meat consumption is expected to continue well into the 2040s for environmental and economic reasons, it may bring less anticipated effects along with it. A continuation of the somewhat counterintuitive trend of “permissive indulgence” (where people consume more “pleasure foods” like chocolate biscuits and cookies) is to be expected. As meals get less interesting and people look elsewhere for delight, the demand for indulgent snacks grows, supporting the segment for packaged goods companies. To thrive in the indulgence-snacking world, however, producers must be up front about their climate impact and nudge consumers toward more choices that promote climate adaptation and mitigation, including “net zero ingredients.”[2]

Given the demand for adaptive products, food producers up and down the value chain must evaluate their forwardlooking capability set, ensuring their supply, operations, R&D, regulatory, supplier assurance, and quality teams are all up to the task of refactoring products and logistics to compete in the future landscape. ADL has supported businesses in the consumer package goods and specialty ingredient space to evaluate the critical build-make-buy decisions for future-proofing the business, with sustainability and decarbonization standing as core pillars of future strategies. Identifying key strategic partnerships and instituting innovation ecosystem approaches may be the most cost-effective approach to changing the system.

Simon Norman, Manager, Technology & Innovation Management Practice, ADL

Phil Webster, Partner, Technology & Innovation Management Practice, ADL

Notes

- “Food miles” refer to the distance over which food is transported before it reaches the customer (including ingredients of processed foods).

- “Net zero ingredients” are ingredients for which an overall balance is achieved between the GHGs they create and the emissions removed from the atmosphere (e.g., through the plantation of trees or other systems that sequester carbon from the air).

Projection 2 - Lonely at the Top

How did we get here?

Forward-looking companies with cash reserves have prepared for the future, betting on a much broader societal and economic move toward adaptation. However, most consumers have not kept up with that trend, largely due to competing priorities, such as rising inequality and higher living costs.

The international economy

Globalized supply chains and the international division of labor continue, albeit disrupted by geopolitical conflicts and climate change impacts. Manufacturing hubs migrate to less vulnerable locations within countries, away from coasts and typhoon-prone regions. Some industrial relocation to developed countries takes place, aided by generous government subsidies.

Society

Regarding many social structures — such as labor, education, care, and family — a two-speed society emerges. Ecosystems organized around powerful, global supply chains transform fastest: large industrial hubs and cities are reengineered to limit heat, build shelters, and protect mobility. Working hours are adapted both for these urban employees and their children at school, who also receive preventative healthcare. At the same time, communities on the periphery of global trade, especially in rural areas, do not undergo significant change.

Winners & losers

There is major consolidation in pharmaceuticals, automotive, electronics, and consumer goods industries like fashion and personal care — as only those firms with the money to invest in adaptation survive. Leading companies reap the benefits of their adaptation investments and have locked in their suppliers, thus gaining a competitive advantage.

Cultural shift

In developed countries, there is a growing cultural polarization between those who embrace a shift in norms, lifestyle, and consumption habits and those who resist that shift — further feeding the “culture wars.”

Impact on the source/make/protect/sell model

-

Source. Customer demand for goods made from rare raw materials including critical metals (lithium, cobalt, tellerum), rare earths, and crops (bananas, cocoa) has remained high. In particular, the fruit, meat, and dairy industries have been compelled to maintain their product range despite rising pressures from climate change. Ingenious ways to procure these crops bloom, such as with vertical farming. There is a growing lobby for SynBio to be applied in agriculture to help grow resilient species while meeting the unchanging preferences of consumers.

-

Make. Constraints on manufacturing operations and processes in many sectors (automotive, electronic goods, pharma, food and beverage) have increased. Manufacturers must develop resilience in the face of power cuts and resource/workforce shortages, as well as challenging working conditions, such as extreme heat. When it comes to products, manufacturers have to compromise on other metrics, including quality and price, leading to brand reputation issues. Other manufacturing sectors that are globally integrated, such as construction and defense, continue to prioritize productivity and profitability, while services (including personal care, education, hospitality, and transportation) provided locally are not subject to the same pressures and are therefore slower to adapt.

-

Protect. Leading businesses have mandated that their partners’ and suppliers’ assets be protected or insured against the main climate risks. Those companies unable to comply are no longer in business, including many in previously manufacturing-heavy regions in South/Southeast Asia and Central America.

-

Sell. Disconnects between companies’ visions and customer preferences have led to commercial failures, such as Tesla’s amphibious car, making firms wary of disruptive product innovation. In a world of fragmented demand, players benefit from serving strong affinity niches, such as red meat eaters. Solutions that can help sense contradictory demand signals in an accurate and timely manner therefore become extremely valuable.

Lonely at the Top: The promise of SynBio

In 2040, the leading global life sciences companies are “lonely at the top.” They have invested earlier than others into R&D for SynBio, as well as for components not usually produced in a fermentation setting. As supply chain disruptions and extreme weather events endanger global supplies of natural drug ingredients and raise the costs of raw materials, they remain resilient to shocks, further enhancing their competitive advantage. Those impacted by the growing disruptions of climate change have no choice but to adapt, and one sustainable approach to doing so is by implementing SynBio. The ability of SynBio to provide substitutes for climate-vulnerable ingredients has been demonstrated since the early 2000s. Since its foundation in 2003, California biotechnology start-up Amyris has used SynBio to produce artemisinin, the active pharmaceutical ingredient in antimalarial drugs. Artemisinin is traditionally derived from the sweet wormwood plant, a wetland plant whose distribution area will be negatively impacted by rising global temperatures.[1] By engineering yeast to produce artemisinin, Amyris has been able to create a more stable and sustainable source of this critical drug component. In a world of flooding and warmer waters that drive increases in malaria cases (+5 million cases; i.e., +2% globally from 2021 to 2022[2]), SynBio helps address pandemic risk by providing climate-resilient alternatives for effective treatments.

In 2019, Roche partnered with Boston, Massachusettsbased Gingko Bioworks to develop a more sustainable production method for oseltamivir phosphate, the active ingredient in its antiviral drug Tamiflu, a critical and widely used drug for the treatment of Influenza A and B. Oseltamivir phosphate is currently derived from shikimic acid, which is extracted from the Chinese star anise plant. This plant is vulnerable to climate change, and its supply has been affected by extreme weather events, including the 2010 droughts in Guangxi and Yunnan. By engineering bacteria to produce shikimic acid, Ginkgo Bioworks aims to create a more reliable and sustainable source of this essential drug component, helping to ensure Tamiflu’s continued availability.

Other life science giants have shown interest in SynBio research as well. In 2018, Bristol Myers Squibb entered into a research collaboration with the biotechnology company Synthorx to develop novel immunotherapies using Synthorx’s SynBio platform. This platform, called the “Expanded Genetic Alphabet,” allows for the incorporation of non-natural amino acids into proteins, which can potentially lead to the development of innovative therapeutics with improved properties. In 2020, Pfizer participated in a $300 million funding round for Zymergen, a company that uses machine learning (ML) and SynBio to engineer microorganisms for the production of various chemicals and materials.

Previous investments in SynBio biology pay dividends in shielding life science companies against future disruptions in supply and skyrocketing ingredient prices. They also hold much promise as a competitive edge in developing a wide range of new products with sought-after properties, sustainably and at an attractive cost. The SynBio market grew at 20% per annum to 2030 overall,[3] driven by sustainability concerns but also by healthcare needs, demands for manufacturing efficiency, and (on the supply side) increasing investment, low technology costs, and growing ecosystems.

The benefits and potential gains that SynBio offers are clear. However, companies must have a well-defined strategy in place to successfully implement it. Key considerations are investing in the right technologies for scale-up and cost-efficiency and ensuring sufficient production capacity. Given the diversity of SynBio, companies should carefully consider which specific fields are relevant for their business and conduct realistic market-based assessments. With an everincreasing acceleration in technology developments, timing is a further key consideration. (For more about SynBio, see the ADL Blue Shift Report “The Brave New World of Synthetic Biology.”)

Dr. Ulrica Sehlstedt, Global Practice Leader, Healthcare & Life Sciences Practice, ADL

Dr. Franziska Thomas, Partner, Healthcare & Life Sciences Practice, ADL

Notes

- Wang, Danyu, et al. “Global Assessment of the Distribution and Conservation Status of a Key Medicinal Plant (Artemisia Annua L.): The Roles of Climate and Anthropogenic Activities.” Science of The Total Environment, Vol. 821, May 2022.

- “World Malaria Report 2023.” World Health Organization, 30 November 2023.

- Meige, Albert, et al. “The Brave New World of Synthetic Biology.” ADL Blue Shift Report, 2024.

“The Forest Spirit gives life and takes life away. Life and death are his alone.” — Moro, Princess Mononoke

Projection 3 - Wild Green West

How did we get here?

Governments are still focusing on mitigation, with a fear of imposing further heavy costs on industries around adaptation. This has led to a lack of globally agreed-upon regulations/practices to promote or impose adaptation to climate change. We see a market-driven approach to climate change adaptation, with businesses voluntarily investing to remain competitive.

The international economy

Leading companies invest in advanced adaptation technologies to protect their businesses from disruption by extreme climate events. In contrast, poorer and more vulnerable regions (e.g., Southeast Asia) struggle to access investment, due to the lack of strong institutions with the necessary manpower, data, and know-how to structure bankable adaptation initiatives. Business investment in climate change adaptation shows benefits, but the lack of societal focus on equality and long-term planning results in a lack of coordination and negative externalities. Such costs not only burden communities but also impact private companies, hindering overall progress toward sustainable and inclusive growth.

Society

A growing split emerges between generations: one prioritizes innovative new ways of living, while the other strives to maintain traditional lifestyles. Reliance on international and national government support diminishes, with private sector companies, regions, and local communities taking more of the initiative.

Winners & losers

Due to a lack of regulation, sectors that are strategically important (e.g., agriculture, energy, and coastal real estate) or have higher economic returns receive more investment than others, leading to crucial areas like biodiversity and public safety being neglected.

Cultural shift

The overwhelming focus on creativity as a catalyst for technological progress, in the absence of robust regulation, has led to ethical dilemmas and debates over moral standards. The consequences of unchecked innovation could have devastating effects, reshaping cultural and political mentalities.

Impact on the source/make/protect/sell model

-

Source. The race to secure resources drives innovation in supply chain management but also prompts concerns over resource monopolization and environmental degradation. Companies invest in desalination infrastructure to secure water availability as well as local grids to secure productivity. With support from local funds, larger agricultural businesses invest in adaptation technology, such as precision irrigation, vertical farming, and sensors for monitoring.

-

Make. We see creative adaptations in manufacturing processes to enhance their efficiency and productivity, mainly within sectors with high raw material and/or electricity costs, such as heavy industries, automotive, and metal/chemical production. With higher raw material prices, manufacturing companies need to focus on cost optimization in their production lines (e.g., by reducing machine time, increasing standardization, and improving resource efficiency).

-

Protect. Companies invest independently to protect their assets, leading to a wide range of solutions with varying degrees of effectiveness, such as predictive weather tools and the use of advanced materials. Nature-based solutions, where ROI is challenging to quantify, are less likely to be supported by traditional financial strategies.

-

Sell. Industries directly engaged in adapting to climate impacts thrive and introduce new goods and services. For example, the construction industry specializes in resilient building technology, the water management industry focuses on water conservation/recycling, while agriculture develops drought-resistant crops and precision farming techniques.

Wild Green West: Integrating mobility into the energy ecosystem

By 2040, the individual mobility industry, driven by private investment and minimal regulation, has continued to innovate, achieving enhanced performance, fuel efficiency, and the development of new vehicles for alternative fuels. Zero-emission vehicles, primarily electric, then hydrogen, make up most of the market, comprising 50%-75% of sales. However, in regions where natural disasters and energy supply disruptions are increasingly common, fuel choices face heightened scrutiny. Alternative fuels present different trade-offs in terms of fuel access, fire risks, and vehicle-to-grid (V2G) power capabilities.

As weather emergencies become more frequent, access to fuel is crucial for maintaining daily mobility. Electric charging stations are expected to proliferate, forming dense networks in developed countries. However, events like Hurricane Sandy in 2012, which rendered 15% of electric charging infrastructure in affected areas of the Northeastern US inoperable due to outages and flooding, are becoming more frequent.

Electric vehicles (EVs) offer unique benefits in emergencies, such as powering local grids or hospital generators for a short period of time. During the 2019 California wildfires in the US, Pacific Gas & Electric (PG&E) used Tesla Powerwall batteries, on which the maximal-charging “Storm Watch” mode had been activated, to supply temporary power to affected communities.[1] Similarly, V2G charging helps deliver electricity in the event of weather-induced blackouts. The city of San Diego, California, is experimenting with a pilot program to enable bidirectional charging with school buses.[2] PG&E CEO Patricia Poppe has supported V2G charging to prevent blackouts, bolstering efforts by General Motors to add this capability on most of its vehicles, which it provided early on Ford’s F-150 Lightning.[3]

Volatile weather events, including floods, extreme temperatures, and wildfires, present trade-offs for alternative fuel vehicles. Extreme temperatures can cause batteries to degrade more quickly and require energy for temperature regulation, reducing driving range and efficiency. And while EVs tend to be less fire-prone than their conventional or hybrid counterparts (the US National Transportation Safety Board reports that EVs have been involved in approximately 25 fires per 100,000 sold in the US compared to 1,530 gasoline-powered and 3,475 hybrid vehicles[4]), fires in EVs are more challenging to extinguish. High-voltage lithium-ion batteries are at risk of thermal runaway, leading to intense, prolonged fires with pollutants and reignition risks. Hydrogen cars are more resilient to fires, as hydrogen is lighter than air and burns at a lower radiant than gasoline, reducing sustained fires and secondary fire risks. However, hydrogen cars present a (low) risk of explosion at critical concentrations of air and hydrogen. Moreover, hydrogen flames tend to be harder to detect, complicating emergency response efforts.

As a result of these trade-offs, the most resilient fleets by 2040 will employ a mixed-vehicle strategy. Large public and private fleets were early to adopt this approach. For example, Los Angeles and San Francisco committed to greening their fleets with a mix of alternative fuel vehicles, including electric, hybrid, natural gas, and hydrogen. By 2040, the mix has become electric or hydrogen-only, due to California’s zero-emission mandate. The US Army invested in hydrogen fuel cell technology, such as the Chevrolet Colorado ZH2, while the Navy has deployed EVs for on-base transportation and logistics. Amazon ordered 100,000 delivery vans from Rivian back in 2022 as well as testing Daimler Truck’s Mercedes-Benz hydrogen fuel-cell trucks in Germany.

To build systemic resilience to climate impacts, deep collaboration between EV manufacturers and local grid providers is essential. In 2016, Nissan and Italian utility company Enel launched the first large-scale V2G project in Denmark, integrating EVs into the national grid. The project installed 10 V2G units at the Danish utility company Frederiksberg Forsyning’s headquarters, allowing EV owners to connect their vehicles to the grid and sell excess energy during peak demand periods, stabilizing the grid while providing an additional revenue stream for EV owners. Meanwhile, V2G options in the US garner significant interest for commercial EVs.

To prepare for this (and other possible) futures, company leaders must maintain a broad perspective. This includes looking beyond short-term impacts and starting to prepare for the new world as structural changes begin to significantly reshape the business environment. It also implies looking beyond obvious trends and reassessing major areas of uncertainty and their implications. Decision makers will need to shape scenarios, make swift no-regret moves, and develop strategic insurance to mitigate unwanted scenarios. This requires embracing uncertainty and embedding it into decision-making: developing capabilities for scenario development and monitoring of trigger events, adjusting strategic and operational planning and related governance mechanisms, and shaping corporate culture so employees feel empowered to deal with uncertainty. Then, companies will be able to leverage digital technologies to improve intelligence and increase agility and responsiveness. (For more information on navigating this increasingly uncertain environment, see the ADL publications “Embracing Uncertainty, Driving Growth,” “Electrifying the Future,” “Truck Electrification — Profit Booster or White Elephant?,” “Driving Profitability in US Public EV Charging,” and “The Relevance of EV Battery Swapping in Emerging Markets.”)

Florent Nanse, Partner, Automotive Practice, ADL

Marc Wiseman, Senior Advisor, Automotive Practice, ADL

Notes

- Lambert, Fred. “Tesla Activated ‘Storm Watch’ for ‘Hundreds’ of Powerwall Owners over California Fires.” Electrek, 11 June 2019.

- “Current V2G Projects.” San Diego Gas & Electric (SDGE), accessed May 2024.

- Melendez, Lyanne. “PG&E CEO Proposes Using Electric Cars to Send Power Back to Grid to Prevent Blackouts.” ABC7 San Francisco, 8 August 2023.

- Weil, Gina. “Data Shows EVs Are Less of a Fire Risk than Conventional Cars.” Fairfax County, Virginia, Office of Environmental and Energy Coordination, 12 February 2024.

“Some problems seem simple and turn out to be complicated, others seem complicated and turn out to be simple.” — Cédric Villani, President of the Fondation de l’Écologie Politique

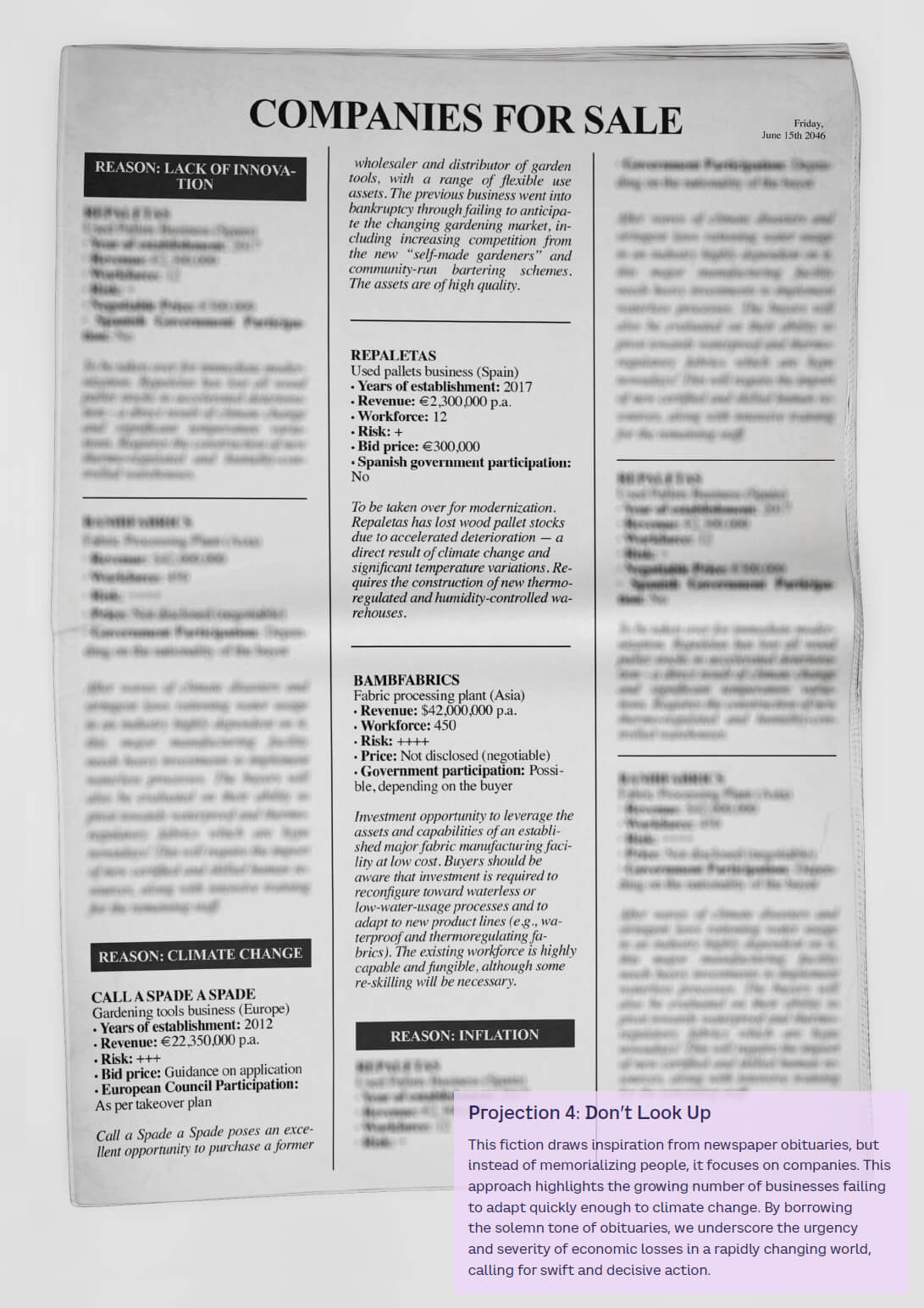

Projection 4 - Don't Look Up

How did we get here?

Not all consumers are feeling the impact of climate change, meaning those who are not constrained to adapt simply do not. Insurance has not caught up with reality, and public funding for adaptation in developing countries remains limited, while private funding (including private equity) remains largely limited to projects that deliver short-term profits.

The international economy

Central banks struggle to curb inflation as the price of raw materials rises. The international division of labor remains in place, apart from a handful of critical materials (e.g., semiconductors) subject to state intervention. Local solutions are deployed in climate-vulnerable regions with access to capital (e.g., the Middle East), but do not spread elsewhere.

Society

Societies remain teetering on the brink of widespread change. Policies that promote both solidarity and climate adaptation have not been developed; hence, resistance to adaptation remains widespread, especially among groups most at risk, including farmers, hospitality workers, those in vulnerable industries or locations, and disenfranchised urban populations. Greater inequality gaps form between those who can afford price increases and those (still in the minority) who must radically change their lifestyles, such as living without a car, thus limiting their mobility. The disappearance of entire communities, towns, and landscapes due to fires, hurricanes, and rising sea levels creates large-scale trauma and challenging migration flows, both within and across countries.

Winners & losers

Asset-light companies in the digital space and companies whose manufacturing facilities are in low-risk areas reap benefits from being able to continuously produce goods, without interruptions from climate change effects. Companies that have already regionalized their production for regulatory reasons (e.g., life sciences) or due to transportation constraints (e.g., manufacturers of large car parts and construction materials) are more resilient. Manufacturers of commodity consumer goods (e.g., textiles and plastics) and smaller agricultural producers are immediately threatened.

Cultural shift

The public remains torn between adaptation to climate change and more pressing concerns, such as fighting rising costs due to inflation. Limited efforts by regulators and some industry leaders are insufficient to move the needle, feeding a sense of hopelessness and frustration.

Impact on the source/make/protect/sell model

-

Source. Smaller agricultural producers not protected by insurance that lack the funds to invest in protection or optimization improvements face the prospect of major consolidation. Shortages and delays become a given — most companies focus on managing disruptions, as they cannot afford to limit them.

-

Make. Raw material substitution is often needed, requiring machines that can function with a broader range of inputs. Only those manufacturers whose industrial processes are very vulnerable to increased climate events introduce new/innovative changes, albeit on a small scale.

-

Protect. Unable to finance large-scale asset-protection projects, companies focus on limiting/controlling damage from the impacts of climate change. Preventative maintenance is also an area of focus to avoid infrastructure and machinery breaking under climate pressures. Greater focus is placed on selecting the right site when purchasing or building a new facility, according to multiple criteria. Data centers, in growing demand due to ongoing digitalization, take the prime spots. There is also increased demand for connectivity, with satellite links encouraged over terrestrial connections (fiber, cable) due to lower vulnerability.

-

Sell. Remaining affordable is the primary concern of many industries producing mid-market products, especially in automotive. A lack of financing mechanisms causes lower readiness in key sectors, such as pharma R&D around the creation of vaccines/drugs addressing climate-borne illnesses.

Don’t Look Up: Cooling for continuity

By 2040, manufacturing plants face regular production interruptions due to fluctuating energy supply, scarcer fresh water, and challenging labor conditions caused by frequent heat waves. Customer apathy and lack of investment in adaptation have slowed down systemic and large-scale changes, leaving manufacturers to cope and adjust under duress. As a result, production costs have risen significantly. Most costs have been passed on to the customer as “climate change inflation,” making middle-of-the-range products like cars increasingly unaffordable for the median consumer, even in industrialized countries, and threatening entire markets. Concerns include:

- Access to a stable, reliable energy source is critical. In regions like India or Texas, disruptions to the electricity grid, already significant in 2024, are deeply problematic in 2040 due to damage from extreme weather and greater demands on the grid. These disruptions compel businesses to interrupt manufacturing operations for several days each year. For example, in France, in 2024, supply to industrial sites was interrupted for 10-15 days in January when residential consumption was at its highest. Manufacturers are forewarned and financially compensated by utility providers. By 2040, such arrangements have multiplied.

- Local power generation helps compensate for variations in the grid supply. Renewables such as wind and solar power, often implemented on-site, are largely insufficient for the needs of a manufacturing facility and intermittent by nature. Gas engine generators become more widespread. Small modular nuclear reactors, with capacities of up to 300 MWe, are considered for the largest, most demanding industries, such as chemicals. Additionally, there may be sporadic development of local energy communities to counterbalance the risk profiles of national grids, but the Don’t Look Up world lacks the planning, investment, and coordination required (see the Adaptation Surge projection).

- Water is an equally critical resource. Climate change has led to increased water scarcity and irregularities in water supply due to changing precipitation patterns and insufficient investment in water-harvesting infrastructure. This raises major concerns for critical processes, such as cooling in nuclear, metallurgical, and chemical plants. While desalination plants are an option in some coastal hubs, the release of brine restricts their installation in several areas. Maximizing efficiency in the use of available freshwater appears to be a safer bet. Water recycling technologies, such as membrane-aerated biofilm reactors, rainwater harvesting, greywater recycling, or closed-circuit reverse osmosis, which treat wastewater for reuse in manufacturing processes, are examples of innovations in this space.

- The increased frequency and severity of heat waves worldwide, including those that are extremely humid, significantly impact working conditions. Resulting changes in ways of working, such as shortening or moving shifts to cooler times, may lead to organizational issues, productivity losses, and increased labor costs. The automation and robotization of manufacturing tasks, usually implemented to streamline processes and improve productivity, also protect workers from hightemperature environments. However, automation has its limits, and not all tasks can be performed by robots. Additionally, most automated machinery relies on electronics that cannot withstand excessively hot environments (>25°C-30°C, or 77°F-86°F).

- Investments in thermal comfort systems, hitherto considered too expensive, are likely to develop. Thermal comfort implementations can be partial to control costs. For example, air-conditioning is installed in only the most heat-sensitive workshops, or factories are fitted with air-conditioned cabins like the Cabin Cool concept designed by Air Innovation, which directly cools air for machine-handling vehicle operators. Arguably, the most economical of thermal comfort solutions works symbiotically with heatconscious design: improving airflow, managing exposure to the sun, and increasing the use of electric machines (e.g., electric presses) wherever relevant.

- In 2040, reliable supplies of power and water will become leading criteria for the location of new manufacturing sites, putting pressure on industrial hubs to secure these services for their tenants. In existing plants, companies are well advised to include adaptation in their comprehensive industrial strategy plans to ensure they can take on these challenges consistently and affordably when they arise — thus building lasting competitive advantage.

Arnaud Jouron, Managing Partner and Global Practice Leader, Performance Practice, ADL

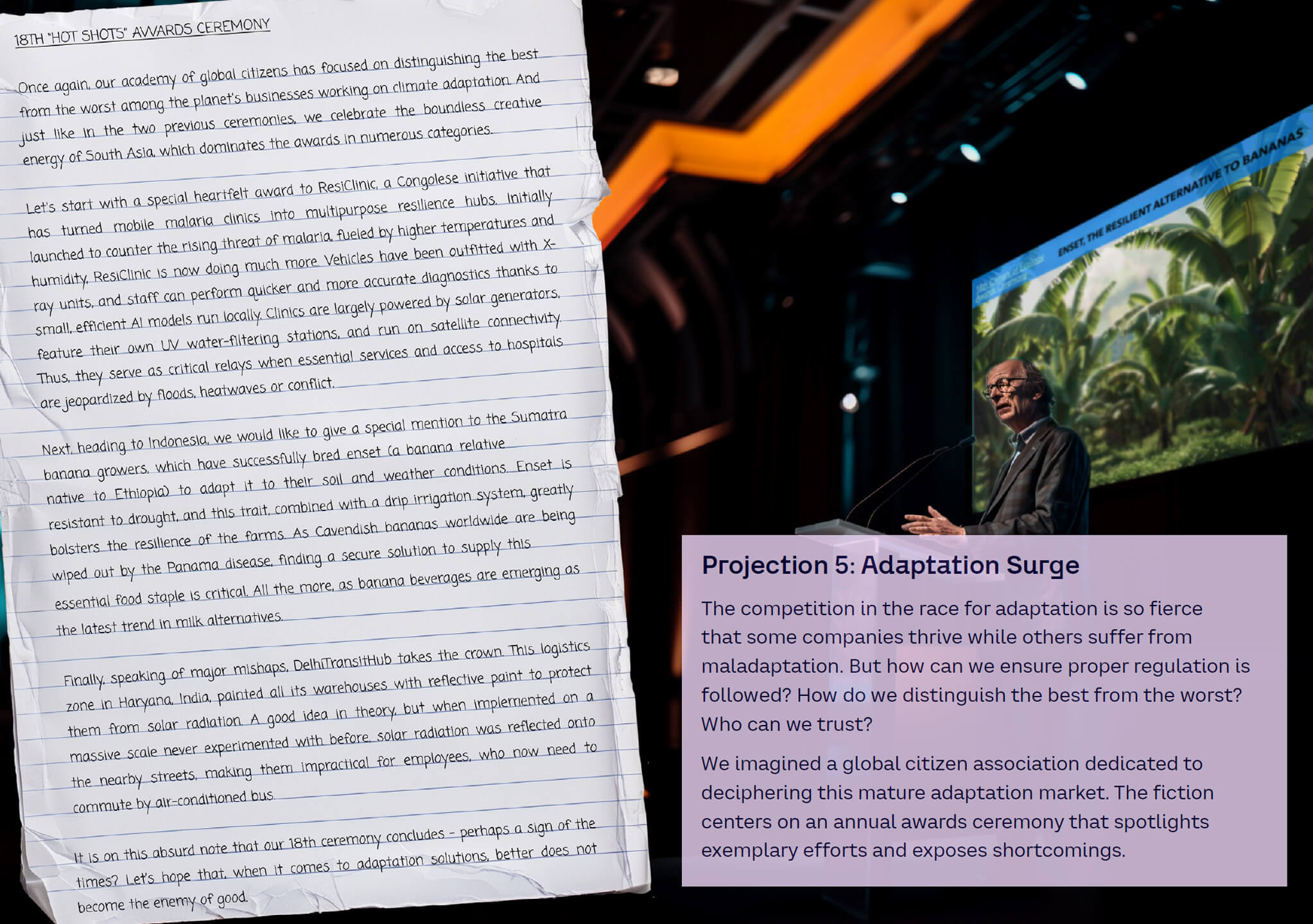

Projection 5 - Adaptation Surge

How did we get here?

In response to recent climate catastrophes, governments worldwide enacted strict adaptation regulations, including prohibiting construction in vulnerable coastal areas, while consumers increasingly demanded action on adaptation measures. Some public sector funding was made available to support adaptation projects, but this is insufficient on its own, requiring additional finance from the private sector.

The international economy