22 min read • Organization & transformation, Strategy

Turning Turmoil to Advantage: How CEOs Are Navigating Change to Drive Growth

CEOs are pushing for growth during global turbulence, focusing on 10 key areas for success

FOREWORD

Organizations, consumers, and citizens are reeling from the ongoing blows of the global pandemic, the geopolitical volatility, the industrial and digital revolutions, and the increasingly visible shocks caused by climate change. We undoubtedly live in times of volatility and uncertainty — with little sign that the rhythm of disruption will calm down.

Continuing with a strategy solely focused on business as usual is a recipe for failure. And in such a context, managing performance today while preparing for the future is complicated. Nevertheless, that is what is needed to avoid all risks and capture the many opportunities hidden behind these disruptions.

But how are companies and the CEOs that lead them reacting to these disruptions? What decisions are they taking and what do they feel about the current and future business environment?

To find out, Arthur D. Little (ADL) has explored in depth how CEOs in different industries and different geographies are coping with this extraordinary combination of challenges. After hundreds of conversations and months of research, the “2023 CEO Insights” study aims to answer five key questions:

-

How do CEOs perceive the current market situation and outlook?

-

What is their take on the right strategy? Is there room for growth?

-

What are the new requirements and calls for action on organization and leadership?

-

What are the challenges for human resources?

-

What is the relevance of environmental, social, and corporate governance (ESG) in this context?

Many of the findings were unexpected, surprising, and even counterintuitive. Despite current challenges and many dark macroeconomic previsions for 2023, most CEOs we spoke to are optimistic for the future, with nearly two-thirds (63%) expecting a stable or positive global economic outlook over the next three to five years.

Essentially, rather than being beaten down by the range and depth of current challenges, these leading CEOs see them as opportunities to be seized. They are willing to invest and innovate to drive growth. Compared to the major 2008/2009 crisis, we can clearly see that a new level of resilience among companies and CEOs has been forged, as illustrated during the pandemic.

This study shows a global executive community taking the bull by the horns and working with passion, coolness, and creativity to manage performance today while building the future.

I am personally convinced that the winners will be this new generation of ambidextrous CEOs and companies!

— Ignacio García Alves, Chairman & Chief Executive Officer, Arthur D. Little

EXECUTIVE SUMMARY

“Adversity equals opportunity” is how today’s CEOs view current, challenging times

Rather than causing them to retreat into their shells and focus on cost-cutting strategies, ADL’s “2023 CEO Insights” study shows that, globally, CEOs of the largest organizations are instead targeting growth through investment and innovation.

They are truly ambidextrous in managing both operational excellence and new innovations. Overall, their mindsets are positive, and they feel their organizations are resilient and well-positioned to cope thanks to changes implemented in response to the pandemic. This is leading them to look beyond their core business to a more balanced portfolio of strategic levers to drive growth. They are using technology as a key lever for innovation and future success.

Adding to this heartening, if potentially surprising, picture, they are focusing on sustainability as a competitive differentiator, moving beyond compliance to understand and benefit from the opportunities it brings. Uncertainty is all around us — but fearless global CEOs are taking advantage of it to shape a more positive future for their businesses and wider society.

1

ANALYSIS: 5 KEY TRENDS FROM TODAY’S CEOs

Analyzing ADL’s “2023 CEO Insights” study leads to five clear conclusions, which apply generally across both geographies and different vertical sectors.

1. CEOs: positive attitude & focused on building a new future

The current crisis has triggered a tsunami of challenges across many industries. Businesses have seen a large-scale drop in customer demand, while input costs, especially for energy, have skyrocketed. Combined with serious strains and breakdowns in supply chains, this has led many commentators to predict the end of globalization as we know it.

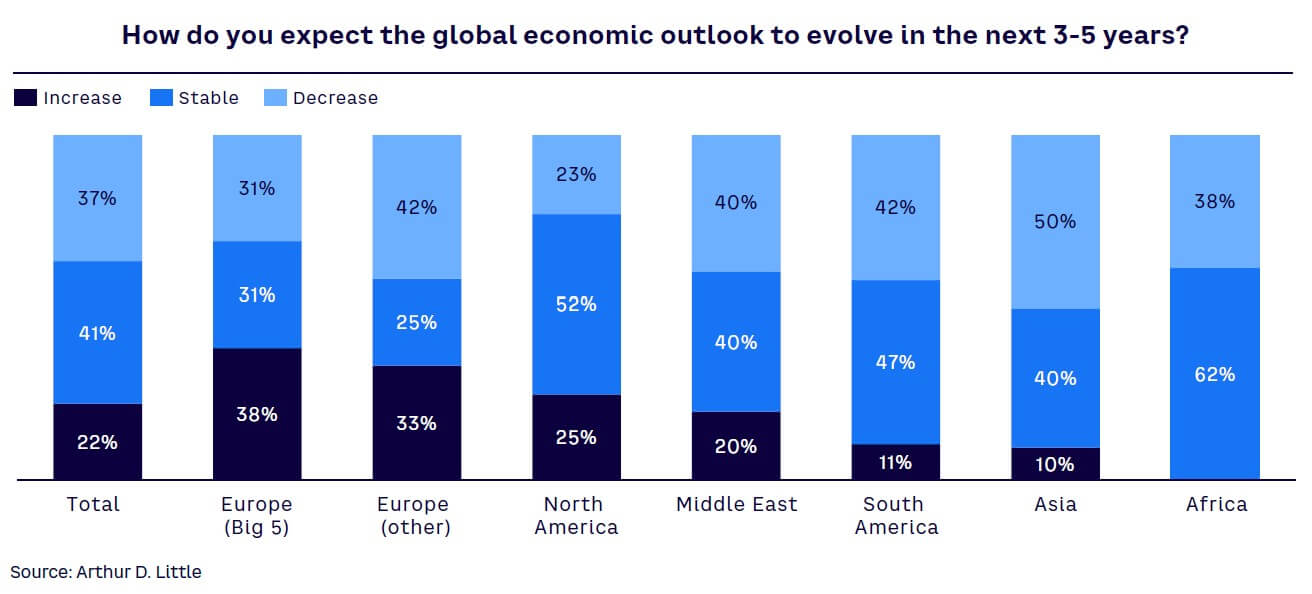

Yet most CEOs are pushing back and embracing a positive, resilient approach. In our sample, we see a trend toward a positive/stable, medium-term (three to five years) overall economic outlook (see Figure 1).

Clearly, optimism varies between regions. The fact that nearly four in 10 CEOs based in the Big Five economies of Europe (Germany, France, UK, Italy, Spain) are expecting global growth is perhaps surprising given the challenges that region in particular faces but may be explainable by a focus on opportunities outside the continent itself. CEOs in the US are more cautious, with over half predicting no growth over the same time period. Just 10% of Asian CEOs expect a positive economic outlook over this time frame.

A commitment to growth

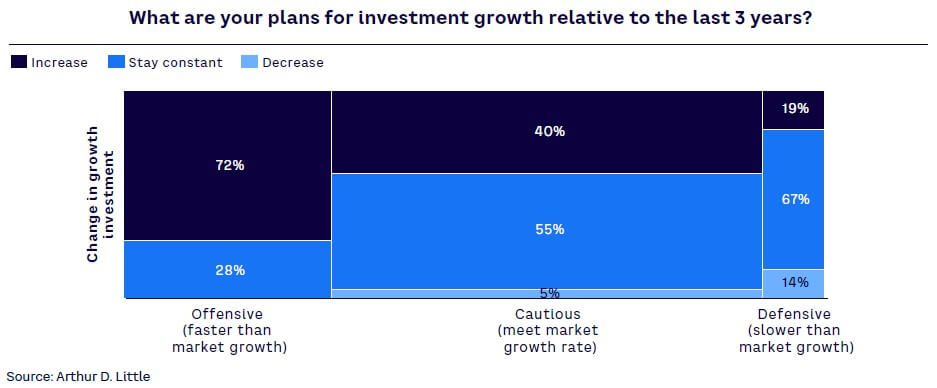

While CEOs are currently very actively engaged in cost savings and troubleshooting, the majority report that they are planning for growth, or at least stability, and are gearing up for the post-crisis world (see Figure 2). Thirty percent plan to grow faster than the market; nearly three-quarters of whom will increase their investment in growth. Showing the widespread commitment to expansion, 40% of those who are planning cautious growth are increasing their growth investment, with 55% keeping it constant. Even one in five CEOs planning a defensive approach expect to invest more relative to the last three years. This sends a strong signal that the future belongs to those who act with courage now to shape their way forward.

In our view, it is very encouraging to see this level of trust and energy, not only to fight the negative effects of the current crisis but also to mobilize creativity and resources to tap into future opportunities.

Resilience forged during the pandemic

These results demonstrate an overall increase in resilience. Essentially, the shock therapy of the COVID pandemic may well have provided a crash course in how to deal with unprecedented challenges, contributing to building more strength and confidence so that CEOs feel well placed to deal with current issues.

“In our industry, we have faced market volatility after the pandemic and due to that we made changes in our working process and strategies leading us to get involved in much better and advanced usage of tools and technologies.” — CEO, healthcare

An openness to government engagement

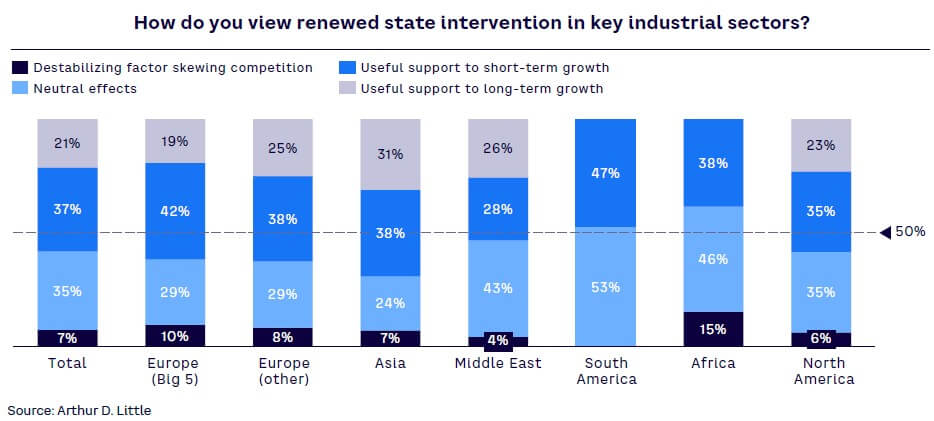

One area that is seeing change is attitudes to government intervention in markets. The pandemic saw an unprecedented growth of state involvement in many sectors, which combines with increasing regulation around areas such as decarbonization and sustainability. Geopolitical rivalry is driving protectionism, with benefits for incumbents in larger geographies. Overall, 58% of CEOs globally said government intervention provided a useful support for short- or long-term growth, with just 7% viewing it negatively (see Figure 3). Concerns are strongest in Africa (15%) and Europe (10%), but the vast majority of CEOs view it positively or with a neutral view.

Furthermore, our global consulting projects show that senior executives are becoming personally involved in the paradigmatic shift currently happening in many of our core industries. For example, mobility and energy are driving decarbonization, telco companies are delivering higher-quality connectivity, while financial and healthcare organizations are fully embracing digitalization. It is encouraging to see that most CEOs of the largest companies are focusing on forward-looking activities rather than remaining in defensive mode.

2. Strategic thrust: Leading ambidextrous agenda

When facing a downturn, conventional business wisdom is to cut costs, focus on the core business, and aim to ride out the recession. However, depending on the industry and customer segments, buying behavior often transforms, opening up new opportunities for those that innovate. The switch to digital during pandemic lockdowns is the perfect example of this change.

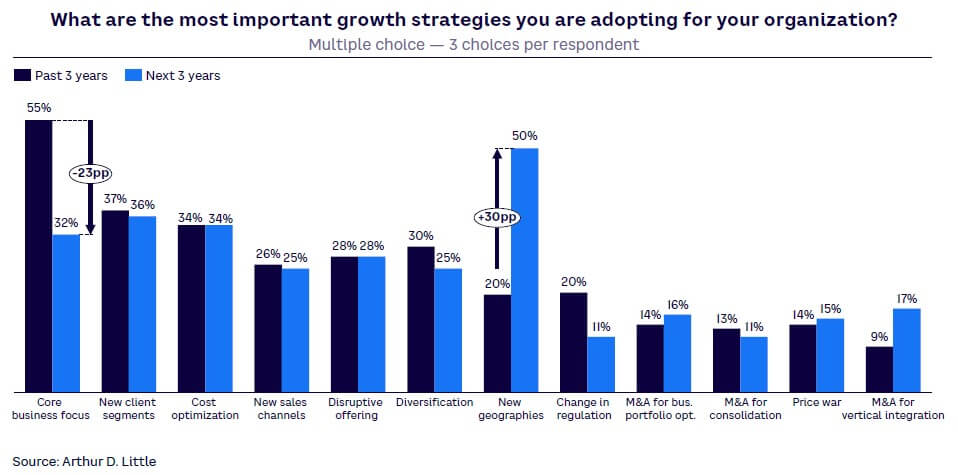

Therefore, we were positively surprised to see that a strong percentage of our sample is now putting the emphasis on innovation as a lever to get ahead and grow, alongside optimizing existing operations (see Figure 4). CEOs are becoming truly ambidextrous.

CEOs are clearly looking to improve efficiency and effectiveness. But they are treating this goal as a constant (e.g., cost optimization remains an unchanged priority) and are focusing more on creating new opportunities. For example, 30% more are planning to enter fresh geographies, while also triggering the development of new products, and are ready to explore different business models. Innovation is key; there is a 23% drop in focus on the core business as a driver of growth, compared to the last three years.

We see good examples of an industry’s moves to improve both efficiency and innovation in the travel and transportation industry. The COVID crisis pushed airlines and airports into large-scale efficiency programs to achieve major cost reductions, impacting thousands of jobs. However, at the same time, these companies are forming new partnerships to offer new services to passengers, such as combined intermodal mobility offerings (e.g., bringing together aircraft, rail, and mobility on-demand services).

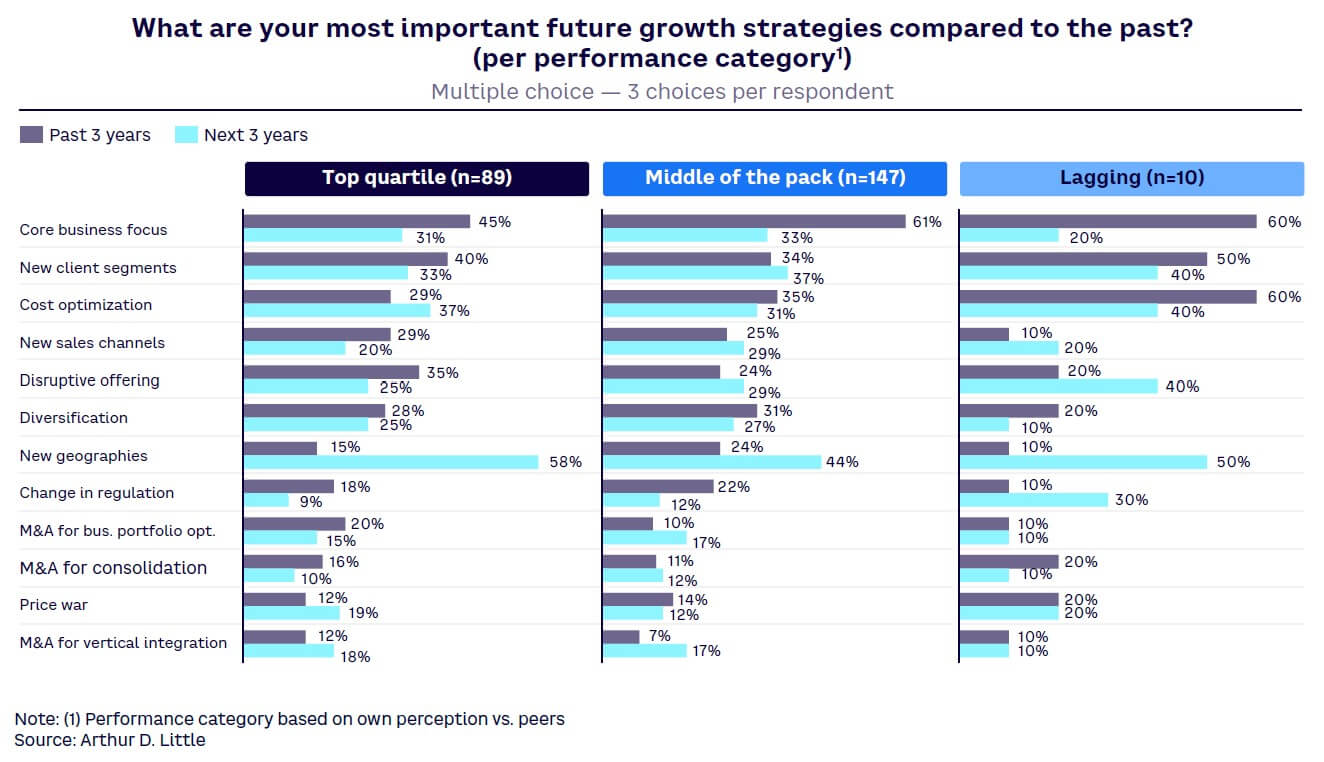

Growth plans — Leaders vs. laggards

Taking a deeper look into growth strategies shows a widening gap between leaders and laggards (see Figure 5). Successful CEOs have built ambitious ambidextrous strategies that combine growth and optimization and are now focused on relentlessly executing on their plans.

By contrast, lagging CEOs have focused only on optimization and are now making major strategic changes as they struggle to catch up. These include:

-

Moving away from a focus on their core business (60% over past three years vs. 20% in the future).

-

Embracing more disruptive offerings (20% past vs. 40% future).

This demonstrates that laggards recognize they need to catch up and can only do this by taking risks.

“Dealing with market uncertainty is such a difficult task, but we are ready to beat that as we are expanding into fast-growing markets and investing in high-tech products which will help us.” — CEO, healthcare

What are the drivers of future growth?

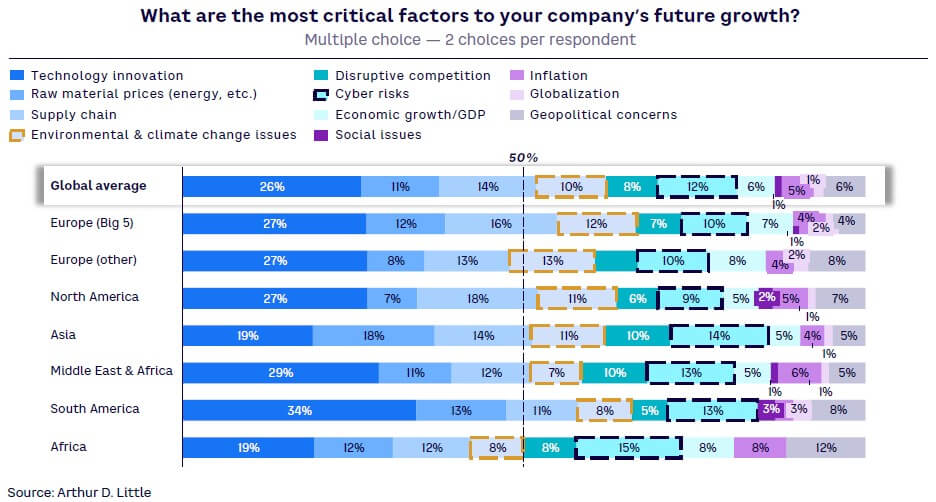

Despite the current energy crisis, all CEOs are focusing on innovation when it comes to drivers of future growth (see Figure 6). Globally, over a quarter (26%) listed technology innovation as the most critical factor to growth, well ahead of raw material/energy prices (11%). Factors such as supply chain, and cyber risks both outranked raw material prices globally.

However, there are clear regional differences:

-

Environmental and climate change issues are a key focus in Europe, North America, and Asia, but receive less attention in other regions.

-

Cyber risk is viewed as a key, urgent factor by 15% of CEOs in Africa, 14% in Asia, and 13% in Middle East and Africa (MEA)/South America, ahead of their peers in Europe and North America.

Again, this positive focus on innovation could be a product of the pandemic, which saw enormous transformation of operations driven by the likes of digital growth, working from home (WFH), and supply chain disruption. With these improvements in place, CEOs are empowered (and enthusiastic) to explore innovation as a growth lever.

“Despite challenging business conditions and changes in the operating environment, we were still able to achieve dramatic growth. Our global efforts to reduce costs achieved our goals three years ahead of schedule. Now we are prepared to handle any future uncertainties.” — CEO, healthcare

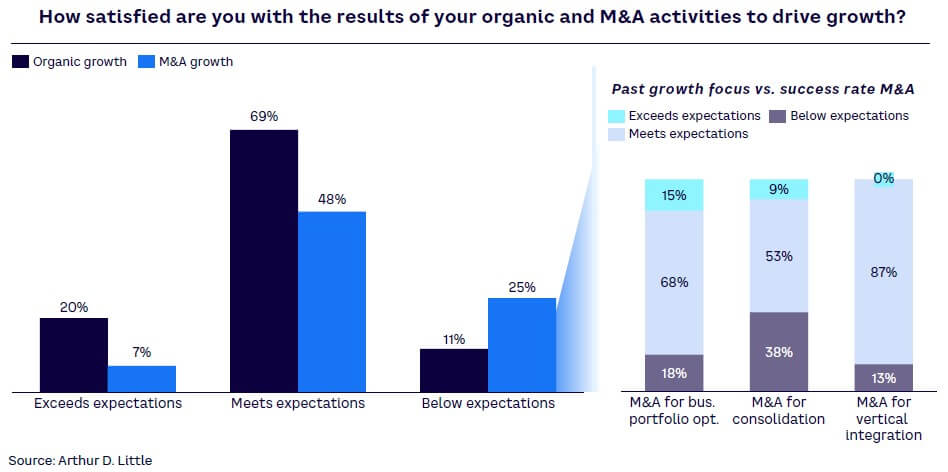

Turmoil brings M&A opportunities

Historically, CEOs have been most satisfied with internal initiatives to drive success (see Figure 7). Of those surveyed, 89% said their organic growth activities met or exceeded their expectations. In our experience, these initiatives are driven by a key focus on customer-centricity, led from the top. At the same time, 25% felt that M&A activity contributions fell below expectations, with success rates for M&A for consolidation even worse, with 38% of CEOs unhappy at the results of this activity.

The major reason for this previous poor contribution from M&A has been extremely high multiples, meaning acquisitions were expensive and often difficult to integrate. Current market turmoil has dramatically lowered prices, providing the perfect opportunity to add programmatic M&A to the CEO agenda, alongside internal initiatives. As well as taking advantage of lower multiples, success requires choosing ambidextrous targets that fit wider corporate strategies and ensuring that the right integration capabilities are in place to deliver real value and growth.

3. Shaping the organization: Building on experience, not wholesale change

The intensive rhythm of disruption required to adapt fundamental ways of working shifts the CEO organizational agenda from a focus on structure to a focus on capabilities. While CEOs are building agile, ambidextrous organizations, the classic question of centralized versus decentralized is much less important. Essentially, CEOs understand that developing fit-for-purpose capabilities that drive optimization and efficiency as well as innovation and growth are now mission-critical.

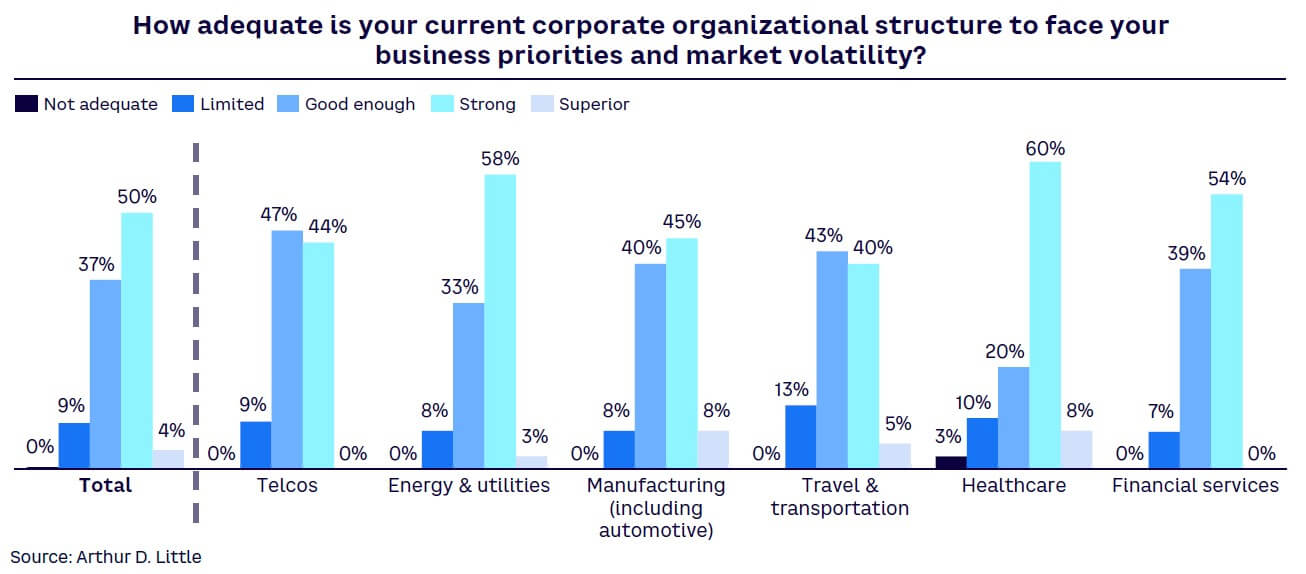

In fact, 91% of CEOs (see Figure 8) felt their current organization setup and structure was sufficiently robust to enable their business priorities. Half felt that their organization was “strong,” although just 4% felt it was superior. This pattern was true across most industries, although healthcare saw a polarization, with 3% believing their structures were inadequate and 68% believing they were strong or superior. This could reflect the wide range of organizations in the sector, some of which transformed during the pandemic, while others are struggling to cope with the long-term impacts it brought.

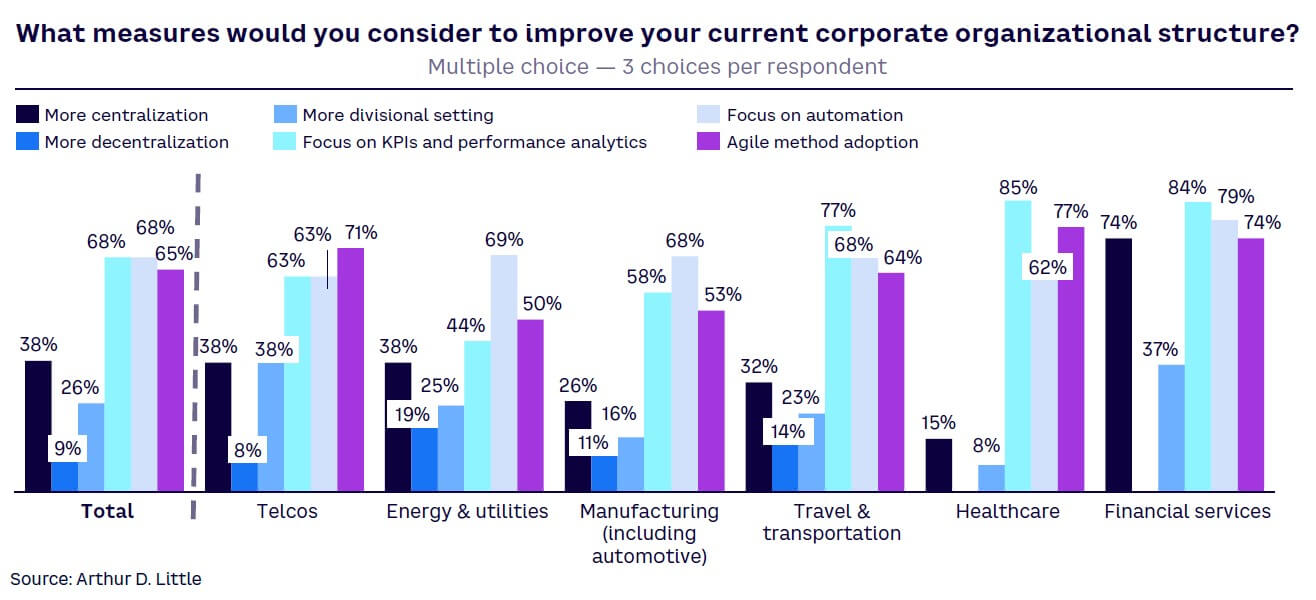

Overall, most organizational structures are now reflecting today’s multidimensional business reality. Attention is shifting to prepare for the strategic challenges ahead. The main organizational improvement focus is a fresh look at automation (68% of respondents), adoption of agile ways of working (65% of respondents) and building KPI/performance metrics that reflect both the performance versus growth dimension as well as hard versus soft skills (68% of respondents; see Figure 9). This is likely to lead to a different capability mix across various companies enabling them to explore and exploit, tailored to their specific strategies for the future.

“We have managed to go through a transition phase and successfully implement the strategies required. This makes us better prepared to face the unexpected, yet we need to further improve on this.” — CEO, financial services

The increasing challenge to find and attract talent

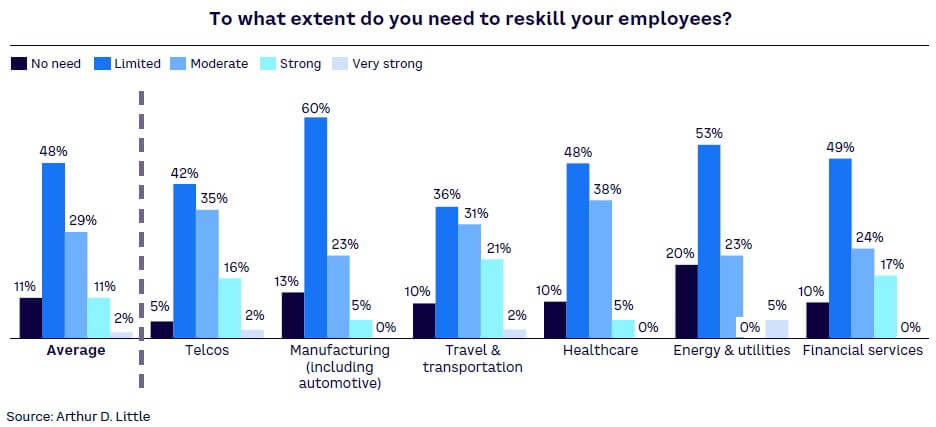

When it comes to recruitment, CEOs have long had concerns around demography (replacing retiring baby boomers) and adapting to the changing values of new generations. On the positive side, most are happy with the skills mix within their organization: just 13% see a strong/very strong impetus to drive reskilling (see Figure 10). However, this varies among industries — and in companies within them — as the example of the energy and utilities sector shows. Among energy players, 20% said there was no need for reskilling, yet at the other end of the spectrum, 5% of CEOs in the sector saw a very strong requirement to invest in this area.

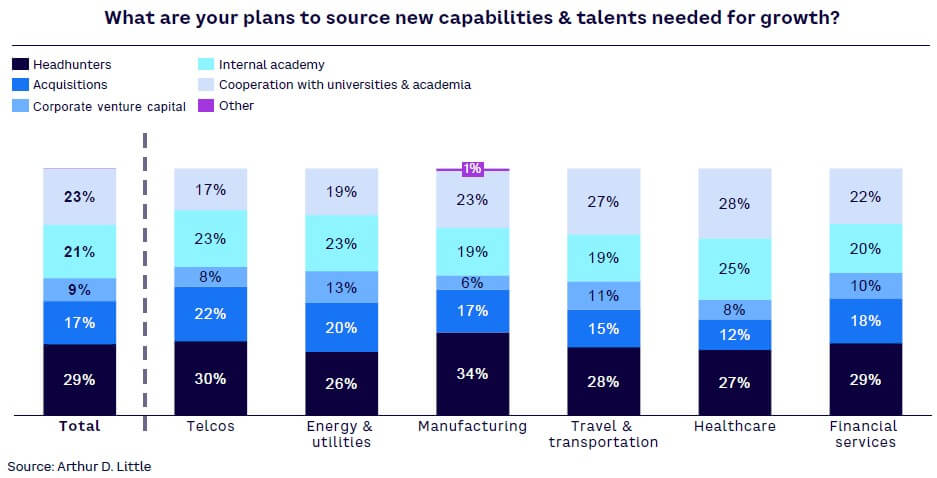

There is concern across industries regarding access to talent (see Figure 11). CEOs struggle to organically attract new capabilities and talents and are focused on acquiring them either via headhunters, corporate venture capital, or direct acquisition. Less than a quarter (21%) of key employees are developed internally, with headhunters the favored option for 29% of companies. A greater focus on diversity, equity, and inclusion (DEI) is likely to help attract and retain talent over the long term.

4. Moving beyond digitalization to embrace technologies

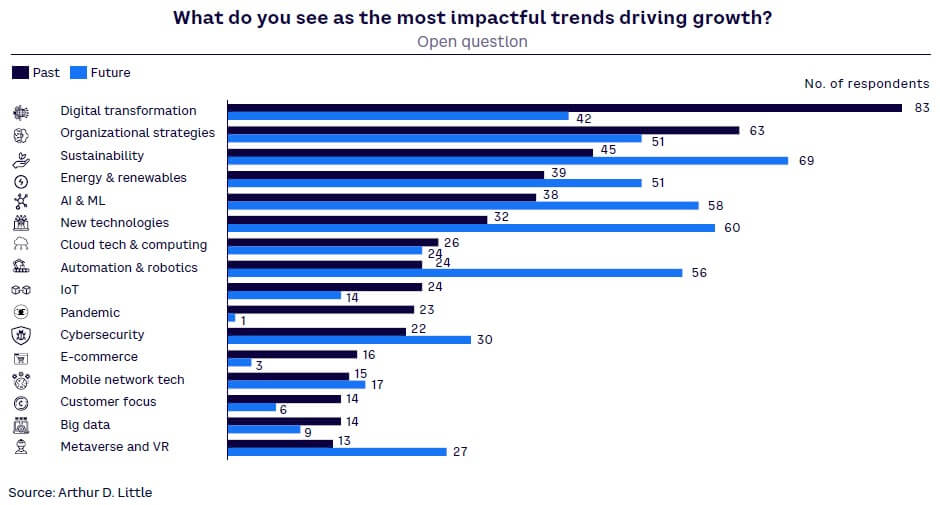

As we have seen, CEOs are focusing on technology innovation to drive growth (refer back to Figure 5). Drilling down into where they see technology delivering benefits shows a step change between the past and future (see Figure 12). While the focus previously has been on digital transformation, looking forward this will virtually halve in importance — to just 42% in the future, as traditional technology trends such as digitalization have become commonplace within organizations.

Essentially, ambidextrous CEOs are now moving beyond using technology, such as digitalization, to drive efficiency and optimization and are now looking at large-scale adoption of new technology to provide a differentiator. They want new technology to underpin their growth agendas and help in acquiring and retaining new customers.

To achieve this going forward, CEOs expect artificial intelligence (AI)/machine learning (ML), automation and robotics, and sustainability to significantly increase in importance. They are moving beyond pilot projects to scale technologies and embed them in the mainstream business. This brings higher expectations for delivery from their teams but potentially higher returns as well.

CEOs are contemplating the future with open minds: 60% want to explore new technologies, and 27% believe the Metaverse and virtual reality (VR) will impact their business. They are monitoring and piloting these technologies now, preparing to exploit opportunities once they mature.

ADL experience supports this trend. AI applications have achieved mass market penetration and are making a significant difference in our societies. For example, they are underpinning new modes and means of transportation, better access to mobility systems, new and bidirectional energy management systems, and automation and automomy enabled by new telecom-connectivity systems. All of this will lead to progressive and radical changes to our economies and societies, and CEOs are focused and active in understanding and acting on the implications of technology breakthroughs.

5. ESG factors become core

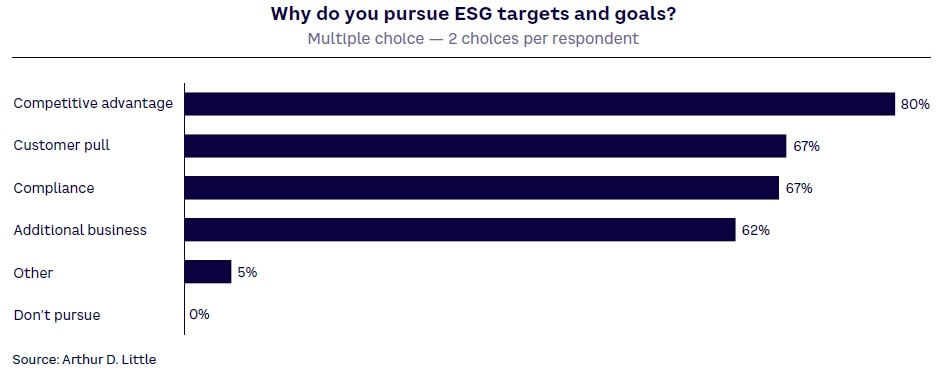

ESG is becoming a full part of the CEO agenda, and increasingly it is seen as an opportunity rather than a threat (see Figure 13). While two-thirds of CEOs admit they pursue ESG targets and goals for compliance reasons, 80% see it as a source of competitive advantage, with 67% referencing consumer pull as a further reason for pursuing greener, more sustainable strategies.

ESG is also rising in strategic importance, with 41% of CEOs making it a higher priority than other initiatives (see Figure 14). Only 1% rank it as a lower priority. Unsurprisingly there is a clear difference between sectors: 60% of carbon-intensive manufacturing companies see it as a higher priority, compared to just 28% of healthcare companies. Increasing the focus on sustainability and committing to targets such as those within the UN’s Sustainable Development Goals (SDGs) delivers wider benefits in both responding to customer needs and attracting today’s purpose-driven generations of employees.

Successful CEOs are moving beyond talk to taking action on sustainability. Based on ADL work and research, we see five key actions to embed sustainability within a company’s operations and governance:

-

Adopt an ecosystem approach, positioning themselves through collaboration with nontraditional partners.

-

Integrate sustainability indicators, reporting, and tools at the core of the business, and incentivize senior management based on these indicators.

-

Redefine their culture and build new capabilities and internal governance.

-

Focus on sustainability technologies and look more widely for innovation beyond traditional value chains.

-

Develop and adopt new business models built on sustainability.

2

HOW SECTORS COMPARE

We have already seen how CEO thinking and actions vary between geographic regions. Unsurprisingly, attitudes show differences across sectors as well, with current and future trends impacting them in distinct ways.

Some sectors are undergoing more radical transformation than others, especially those driven by convergence, which is enabling new opportunities but adding complexity. In the travel and transportation sector, for example, all players are gearing up to address a major shift in the classical paradigm of mobility management. This new mobility will be electric (with a lower carbon footprint), fully integrated and intermodal, and more autonomous, but also more demand and efficiency oriented. Around this paradigm a variety of new services will emerge to be addressed by traditional and new players, all of them working in stronger partnerships and ecosystems. In addition to transportation companies, these ecosystems will involve players such as energy suppliers, automotive manufacturers, telco companies providing connectivity, and even government agencies. CEOs understand that these trends go far beyond the current global crisis and are acting and planning accordingly.

These differences between sectors are particularly highlighted in three areas: (1) optimism for the future, (2) views on the importance of growth/investment strategies, and (3) the levers CEOs expect to drive the growth.

Future economic outlook

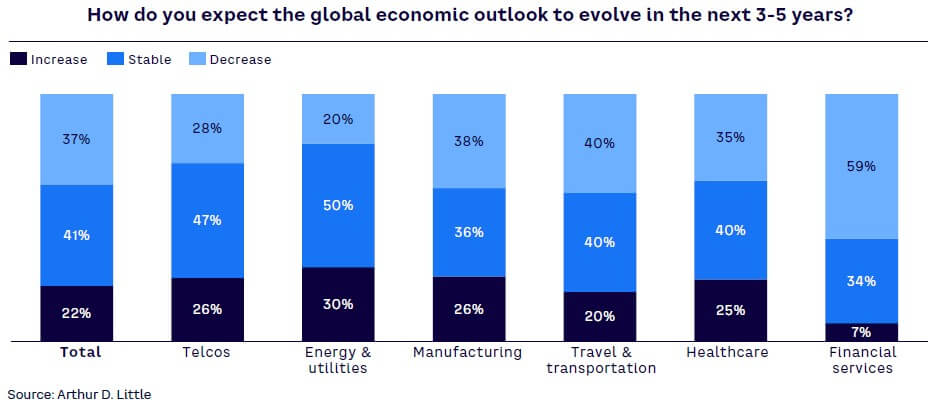

Current turbulence means some sectors are winning while others languish (see Figure 15). For example, 80% of CEOs of energy & utilities companies believe the global economic outlook will either improve or remain stable over the next three to five years. This could reflect the positive side of higher energy prices, particularly among producers. The telco sector is also positive, demonstrating its position as a critical part of everyone’s work and daily lives. In contrast, industries that are not able to benefit from the crisis, such as financial services, are extremely pessimistic, with 59% in that sector expecting a decline in the global economy.

“Every firm can be impacted by an uncertain and unpredictable environment. We were not completely prepared during the pandemic and had a challenging experience. Now, we are preparing for the future by increasing our operational reach and updating technology inside our company.” — CEO, travel & transportation

“Through the methodical implementation of our strategy program and a creative and innovative commercial approach, we have now repositioned the company for growth.” — CEO, telco

The relative importance of growth — and where investments are being made

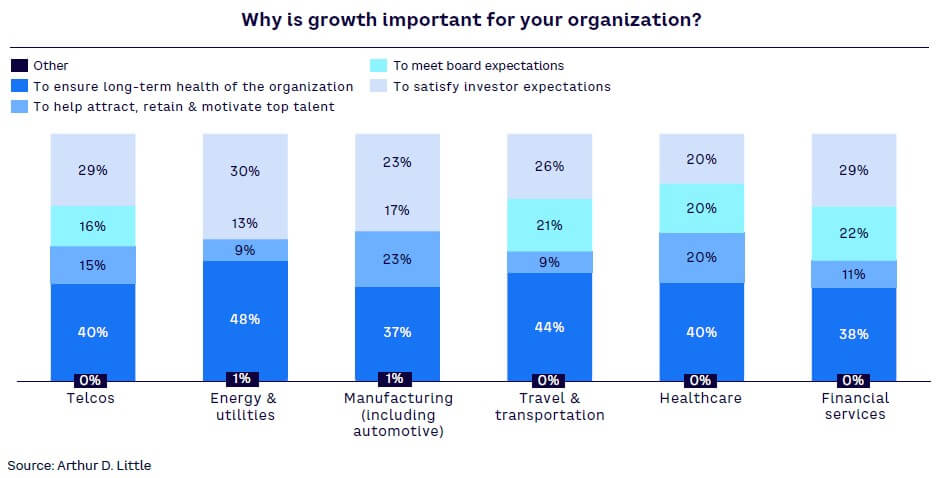

CEOs in all sectors view growth as vital for their organization. However, there’s diversity in the reasons they want to grow (see Figure 16). Nearly a quarter of manufacturing companies (23%) believe it will help them attract, retain, and motivate top talent — higher than in all other sectors. Growth is seen as most critical to securing the long-term health of the organization, particularly in energy and utilities (cited by 48% of CEOs), demonstrating the large-scale transformation happening in the sector as the world decarbonizes. Financial services is driven most by investor and board expectations (51%), reflecting the more traditional nature of the industry.

“Despite challenging business conditions, we were still able to achieve dramatic growth. Our global efforts to reduce costs meant we achieved our goals three years ahead of schedule. Now we are prepared to handle all the uncertainties that may arise.” — CEO, healthcare

“High volatility and geopolitical tensions continually affect the energy market. We are increasing our production multifold by utilizing different tactics and new updated technologies while keeping resource sustainability in mind.” — CEO, energy & utilities

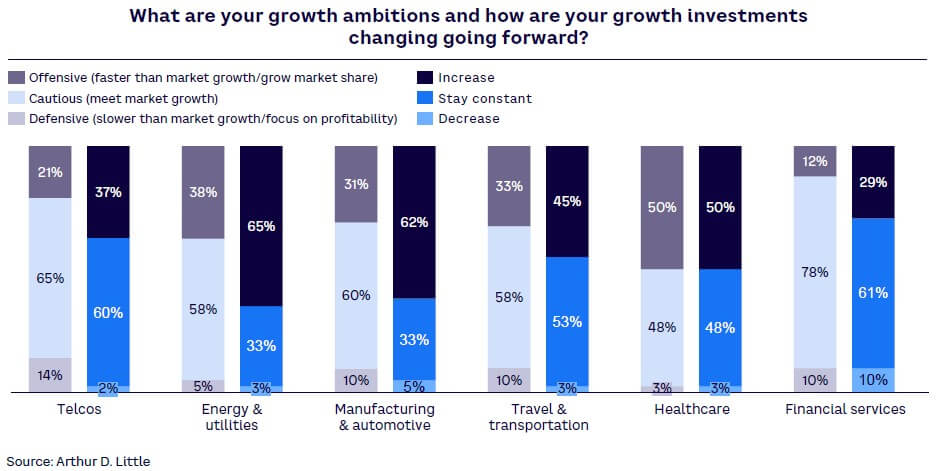

In the minds of CEOs, future opportunities are not evenly spread among sectors, with a greater number of companies in certain sectors (healthcare, energy and utilities, travel and transportation) aiming to achieve above-average growth rates (see Figure 17). In contrast, just 12% of financial services CEOs are adopting offensive growth strategies, the lowest number in the study.

These different approaches drive investment budgets. Less than a third (29%) of financial services companies will increase their growth investments, with 10% decreasing them. Nearly two-thirds (65%) of energy and utilities CEOs will boost spending in this area, alongside 62% of those in manufacturing. In both these cases, radical transformation required for sustainability are key drivers for CEOs.

Levers for growth

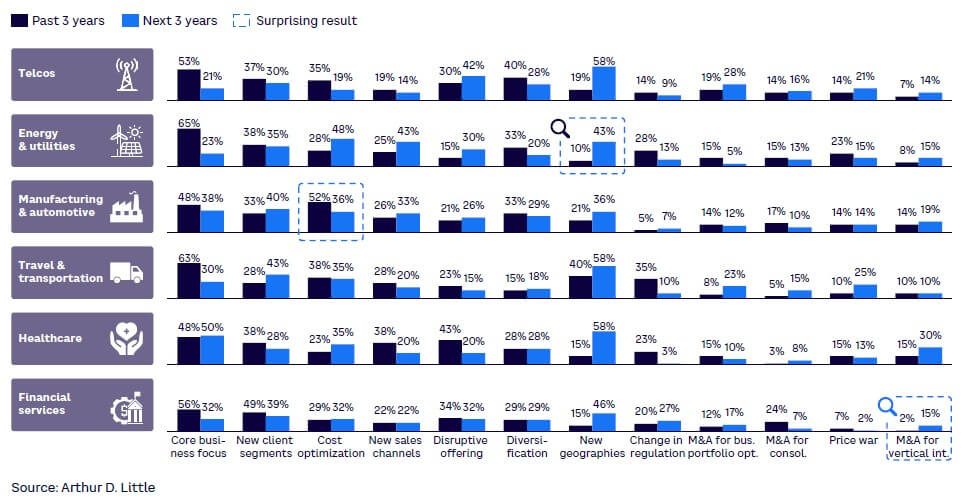

While CEOs in every sector are consistently reducing their focus on their core business, where they are looking for growth varies widely (see Figure 18). Telcos and energy and utilities CEOs are dramatically increasing their efforts around disruptive innovation and expansion into new geographies. Energy CEOs are aiming to be truly ambidextrous, also accelerating their emphasis on cost optimization and seeing the largest drop in focus (42%) on their (previously) core business.

Perhaps surprisingly for a sector noted for a constant focus on process improvement, manufacturing is moving away from cost optimization, instead embracing new sales channels and new geographies. Reflecting the sector’s static, rather pessimistic view of current opportunities, financial services CEOs are planning a seven-fold increase in M&A investments to drive vertical integration as they battle new competitors.

“A diversified investment portfolio will work to our advantage. We are planning more investments in technology and fast-growth sectors.” — CEO, financial services

“Concentrate on twin transformations to withstand economic shocks. One would be looking for raw material substitutes and the other would be an investment in technology.” — CEO, manufacturing

CONCLUSION: FORTUNE FAVORS THE BRAVE

It is easy to become disheartened in current times. Short-term challenges, such as inflation, and longer-term issues, such as climate change, have swiftly followed the global pandemic, which continues to cause death and disruption.

However, ADL research demonstrates that, globally, CEOs of our largest companies are embracing the positive and seeing the opportunities that arise from turmoil. They have a growth focus and are confident that a combination of pandemic-hardened organizational structures and innovation will allow them to thrive, rather than just survive. Across sectors and geographies they are combining this focus on growth with cost optimization, building agile, ambidextrous organizations that can innovate while increasing productivity.

Based on the five broad trends that emerged from our 2023 survey and that we have discussed above, we have defined 10 CEO imperatives to help companies remain competitive, both now and in the future.

Trend #1: Build a new future for the company

-

Pursue a growth-oriented strategy. The vast majority of companies are maintaining or increasing their investment in growth. Going forward, this means a fundamental revisit of strategic plans and priorities to reflect this desire for growth. Companies now need to develop strategies to identify new markets, customer segments, and new products to actively shape the business portfolio of the future while keeping an eye on profitability. The survey shows that CEOs believe that the current economic climate presents unique opportunities for expansion and diversification that can only be captured through a growth-oriented strategy.

-

Engage proactively with government stakeholders. CEOs realize that governments are restructuring and revisiting regulation to respond to societal crises. Companies that engage constructively with policy makers will be able to secure their futures. Companies must actively shape policy and regulation, particularly around decarbonization and sustainability, to become the winners of the future.

Trend #2: Lead an ambidextrous agenda

-

Balance resource allocation between optimization and growth/renewal priorities. CEOs have stated a desire to maintain a good balance between optimization and growth/innovation priorities, building an ambidextrous strategic agenda for the company. We believe that this balance must be enabled with the right level of capital and workforce deployment. Keeping this in mind, companies should ensure adequate budget and, more importantly, leadership bandwidth allocation to strike the right balance between innovation and optimization initiatives.

-

Develop programmatic M&A as a strategic lever while doubling down on existing customers. CEOs have expressed dissatisfaction with existing M&A programs. This is driven mostly by expansive fiscal policies inflating asset prices and valuations that have set up most acquisitions for failure, with the buyer overpaying significantly. The new inflationary environment has tempered valuations and, with dropping P/E multiples, we believe that acquisition targets have become strategically affordable as a result. While continuing to focus heavily on existing customers, CEOs can put past M&A disappointments behind them to build programmatic M&A initiatives supported by thoughtful integration capabilities.

Trend #3: Shape the organization

-

Fill capability gaps. CEOs believe that now is not the time to indulge in time-consuming changes of organizational structure but instead to strengthen the existing organization. As a result, companies should proactively seek out and develop the right talents, whether internally, through acquisition, or via headhunters. At the same time, companies should focus on encouraging more organizational diversity by widening the range of experiences and backgrounds of prospective employees to match changing business and customer needs.

-

Build organizational agility. An ambidextrous strategic agenda will need an ambidextrous organization. Companies should strive to break down silos, encourage cross-functional teaming and collaboration, and encourage more risk taking and innovation. At the same time, revisiting KPIs/key responsibility areas (KRAs), and objectives and key results (OKRs) to encourage and incentivize innovation will help create the right motivation for employees to think outside the box.

Trend #4: Leverage technology

-

Build a comprehensive technology transformation agenda beyond process digitization. COVID-19 drove companies to embrace process digitization, driving cost reduction and enabling WFH. CEOs recognize that technology is a key driver for growth, innovation, and cost optimization. Going forward, companies need to embrace newer technologies such as AI, robotics, and the Metaverse to increase revenues, enable innovation, and sustain/ensure market differentiation.

-

Invest in scaling technology usage from pilot projects and sandboxes. CEOs realize that advanced technologies need to be embedded in business models to drive full value realization. Going forward, companies should scale investment in new technologies, moving away from pilot projects and sandboxes. As investments in technology scale, companies could consider measuring return on investment in technology (RoIT) and incorporating this in company and employee dashboards.

Trend #5: Move ESG into the core

-

Move from intent to action on ESG. CEOs are beginning to view ESG as a positive and not just a compliance cost. Companies must put sustainability at the core of their business model and engage with customers, suppliers, and regulators. At the same time, CEOs should create and drive multiple strategic initiatives that underpin the achievement of ESG goals and create a culture of positive ESG actions in the company.

-

Craft and execute bold ESG bets. Progressive CEOs believe that ESG could be a source of future business model differentiation and drive the increased acquisition and retention of customers. As a result, companies could craft bold ESG bets such as divesting carbon-intensive operations, investments in new technologies (such as carbon capture and storage), and create an end-to-end green business model. Raising green finance to fund these bets will become increasingly important.

It will take a bold CEO to embrace and drive all of these recommended imperatives, navigate the current turmoil, capitalize on new opportunities, and build the companies of the future. However, our research finds that, increasingly, CEOs leading the largest organizations across the globe have the skills, optimism, and growth plans to thrive in the uncertain future.

Note

[1] Milanese, Stefano, et al. “Overcoming the Challenges to Sustainability.” Arthur D. Little Report, July 2022.

DOWNLOAD THE FULL REPORT

22 min read • Organization & transformation, Strategy

Turning Turmoil to Advantage: How CEOs Are Navigating Change to Drive Growth

CEOs are pushing for growth during global turbulence, focusing on 10 key areas for success

DATE

FOREWORD

Organizations, consumers, and citizens are reeling from the ongoing blows of the global pandemic, the geopolitical volatility, the industrial and digital revolutions, and the increasingly visible shocks caused by climate change. We undoubtedly live in times of volatility and uncertainty — with little sign that the rhythm of disruption will calm down.

Continuing with a strategy solely focused on business as usual is a recipe for failure. And in such a context, managing performance today while preparing for the future is complicated. Nevertheless, that is what is needed to avoid all risks and capture the many opportunities hidden behind these disruptions.

But how are companies and the CEOs that lead them reacting to these disruptions? What decisions are they taking and what do they feel about the current and future business environment?

To find out, Arthur D. Little (ADL) has explored in depth how CEOs in different industries and different geographies are coping with this extraordinary combination of challenges. After hundreds of conversations and months of research, the “2023 CEO Insights” study aims to answer five key questions:

-

How do CEOs perceive the current market situation and outlook?

-

What is their take on the right strategy? Is there room for growth?

-

What are the new requirements and calls for action on organization and leadership?

-

What are the challenges for human resources?

-

What is the relevance of environmental, social, and corporate governance (ESG) in this context?

Many of the findings were unexpected, surprising, and even counterintuitive. Despite current challenges and many dark macroeconomic previsions for 2023, most CEOs we spoke to are optimistic for the future, with nearly two-thirds (63%) expecting a stable or positive global economic outlook over the next three to five years.

Essentially, rather than being beaten down by the range and depth of current challenges, these leading CEOs see them as opportunities to be seized. They are willing to invest and innovate to drive growth. Compared to the major 2008/2009 crisis, we can clearly see that a new level of resilience among companies and CEOs has been forged, as illustrated during the pandemic.

This study shows a global executive community taking the bull by the horns and working with passion, coolness, and creativity to manage performance today while building the future.

I am personally convinced that the winners will be this new generation of ambidextrous CEOs and companies!

— Ignacio García Alves, Chairman & Chief Executive Officer, Arthur D. Little

EXECUTIVE SUMMARY

“Adversity equals opportunity” is how today’s CEOs view current, challenging times

Rather than causing them to retreat into their shells and focus on cost-cutting strategies, ADL’s “2023 CEO Insights” study shows that, globally, CEOs of the largest organizations are instead targeting growth through investment and innovation.

They are truly ambidextrous in managing both operational excellence and new innovations. Overall, their mindsets are positive, and they feel their organizations are resilient and well-positioned to cope thanks to changes implemented in response to the pandemic. This is leading them to look beyond their core business to a more balanced portfolio of strategic levers to drive growth. They are using technology as a key lever for innovation and future success.

Adding to this heartening, if potentially surprising, picture, they are focusing on sustainability as a competitive differentiator, moving beyond compliance to understand and benefit from the opportunities it brings. Uncertainty is all around us — but fearless global CEOs are taking advantage of it to shape a more positive future for their businesses and wider society.

1

ANALYSIS: 5 KEY TRENDS FROM TODAY’S CEOs

Analyzing ADL’s “2023 CEO Insights” study leads to five clear conclusions, which apply generally across both geographies and different vertical sectors.

1. CEOs: positive attitude & focused on building a new future

The current crisis has triggered a tsunami of challenges across many industries. Businesses have seen a large-scale drop in customer demand, while input costs, especially for energy, have skyrocketed. Combined with serious strains and breakdowns in supply chains, this has led many commentators to predict the end of globalization as we know it.

Yet most CEOs are pushing back and embracing a positive, resilient approach. In our sample, we see a trend toward a positive/stable, medium-term (three to five years) overall economic outlook (see Figure 1).

Clearly, optimism varies between regions. The fact that nearly four in 10 CEOs based in the Big Five economies of Europe (Germany, France, UK, Italy, Spain) are expecting global growth is perhaps surprising given the challenges that region in particular faces but may be explainable by a focus on opportunities outside the continent itself. CEOs in the US are more cautious, with over half predicting no growth over the same time period. Just 10% of Asian CEOs expect a positive economic outlook over this time frame.

A commitment to growth

While CEOs are currently very actively engaged in cost savings and troubleshooting, the majority report that they are planning for growth, or at least stability, and are gearing up for the post-crisis world (see Figure 2). Thirty percent plan to grow faster than the market; nearly three-quarters of whom will increase their investment in growth. Showing the widespread commitment to expansion, 40% of those who are planning cautious growth are increasing their growth investment, with 55% keeping it constant. Even one in five CEOs planning a defensive approach expect to invest more relative to the last three years. This sends a strong signal that the future belongs to those who act with courage now to shape their way forward.

In our view, it is very encouraging to see this level of trust and energy, not only to fight the negative effects of the current crisis but also to mobilize creativity and resources to tap into future opportunities.

Resilience forged during the pandemic

These results demonstrate an overall increase in resilience. Essentially, the shock therapy of the COVID pandemic may well have provided a crash course in how to deal with unprecedented challenges, contributing to building more strength and confidence so that CEOs feel well placed to deal with current issues.

“In our industry, we have faced market volatility after the pandemic and due to that we made changes in our working process and strategies leading us to get involved in much better and advanced usage of tools and technologies.” — CEO, healthcare

An openness to government engagement

One area that is seeing change is attitudes to government intervention in markets. The pandemic saw an unprecedented growth of state involvement in many sectors, which combines with increasing regulation around areas such as decarbonization and sustainability. Geopolitical rivalry is driving protectionism, with benefits for incumbents in larger geographies. Overall, 58% of CEOs globally said government intervention provided a useful support for short- or long-term growth, with just 7% viewing it negatively (see Figure 3). Concerns are strongest in Africa (15%) and Europe (10%), but the vast majority of CEOs view it positively or with a neutral view.

Furthermore, our global consulting projects show that senior executives are becoming personally involved in the paradigmatic shift currently happening in many of our core industries. For example, mobility and energy are driving decarbonization, telco companies are delivering higher-quality connectivity, while financial and healthcare organizations are fully embracing digitalization. It is encouraging to see that most CEOs of the largest companies are focusing on forward-looking activities rather than remaining in defensive mode.

2. Strategic thrust: Leading ambidextrous agenda

When facing a downturn, conventional business wisdom is to cut costs, focus on the core business, and aim to ride out the recession. However, depending on the industry and customer segments, buying behavior often transforms, opening up new opportunities for those that innovate. The switch to digital during pandemic lockdowns is the perfect example of this change.

Therefore, we were positively surprised to see that a strong percentage of our sample is now putting the emphasis on innovation as a lever to get ahead and grow, alongside optimizing existing operations (see Figure 4). CEOs are becoming truly ambidextrous.

CEOs are clearly looking to improve efficiency and effectiveness. But they are treating this goal as a constant (e.g., cost optimization remains an unchanged priority) and are focusing more on creating new opportunities. For example, 30% more are planning to enter fresh geographies, while also triggering the development of new products, and are ready to explore different business models. Innovation is key; there is a 23% drop in focus on the core business as a driver of growth, compared to the last three years.

We see good examples of an industry’s moves to improve both efficiency and innovation in the travel and transportation industry. The COVID crisis pushed airlines and airports into large-scale efficiency programs to achieve major cost reductions, impacting thousands of jobs. However, at the same time, these companies are forming new partnerships to offer new services to passengers, such as combined intermodal mobility offerings (e.g., bringing together aircraft, rail, and mobility on-demand services).

Growth plans — Leaders vs. laggards

Taking a deeper look into growth strategies shows a widening gap between leaders and laggards (see Figure 5). Successful CEOs have built ambitious ambidextrous strategies that combine growth and optimization and are now focused on relentlessly executing on their plans.

By contrast, lagging CEOs have focused only on optimization and are now making major strategic changes as they struggle to catch up. These include:

-

Moving away from a focus on their core business (60% over past three years vs. 20% in the future).

-

Embracing more disruptive offerings (20% past vs. 40% future).

This demonstrates that laggards recognize they need to catch up and can only do this by taking risks.

“Dealing with market uncertainty is such a difficult task, but we are ready to beat that as we are expanding into fast-growing markets and investing in high-tech products which will help us.” — CEO, healthcare

What are the drivers of future growth?

Despite the current energy crisis, all CEOs are focusing on innovation when it comes to drivers of future growth (see Figure 6). Globally, over a quarter (26%) listed technology innovation as the most critical factor to growth, well ahead of raw material/energy prices (11%). Factors such as supply chain, and cyber risks both outranked raw material prices globally.

However, there are clear regional differences:

-

Environmental and climate change issues are a key focus in Europe, North America, and Asia, but receive less attention in other regions.

-

Cyber risk is viewed as a key, urgent factor by 15% of CEOs in Africa, 14% in Asia, and 13% in Middle East and Africa (MEA)/South America, ahead of their peers in Europe and North America.

Again, this positive focus on innovation could be a product of the pandemic, which saw enormous transformation of operations driven by the likes of digital growth, working from home (WFH), and supply chain disruption. With these improvements in place, CEOs are empowered (and enthusiastic) to explore innovation as a growth lever.

“Despite challenging business conditions and changes in the operating environment, we were still able to achieve dramatic growth. Our global efforts to reduce costs achieved our goals three years ahead of schedule. Now we are prepared to handle any future uncertainties.” — CEO, healthcare

Turmoil brings M&A opportunities

Historically, CEOs have been most satisfied with internal initiatives to drive success (see Figure 7). Of those surveyed, 89% said their organic growth activities met or exceeded their expectations. In our experience, these initiatives are driven by a key focus on customer-centricity, led from the top. At the same time, 25% felt that M&A activity contributions fell below expectations, with success rates for M&A for consolidation even worse, with 38% of CEOs unhappy at the results of this activity.

The major reason for this previous poor contribution from M&A has been extremely high multiples, meaning acquisitions were expensive and often difficult to integrate. Current market turmoil has dramatically lowered prices, providing the perfect opportunity to add programmatic M&A to the CEO agenda, alongside internal initiatives. As well as taking advantage of lower multiples, success requires choosing ambidextrous targets that fit wider corporate strategies and ensuring that the right integration capabilities are in place to deliver real value and growth.

3. Shaping the organization: Building on experience, not wholesale change

The intensive rhythm of disruption required to adapt fundamental ways of working shifts the CEO organizational agenda from a focus on structure to a focus on capabilities. While CEOs are building agile, ambidextrous organizations, the classic question of centralized versus decentralized is much less important. Essentially, CEOs understand that developing fit-for-purpose capabilities that drive optimization and efficiency as well as innovation and growth are now mission-critical.

In fact, 91% of CEOs (see Figure 8) felt their current organization setup and structure was sufficiently robust to enable their business priorities. Half felt that their organization was “strong,” although just 4% felt it was superior. This pattern was true across most industries, although healthcare saw a polarization, with 3% believing their structures were inadequate and 68% believing they were strong or superior. This could reflect the wide range of organizations in the sector, some of which transformed during the pandemic, while others are struggling to cope with the long-term impacts it brought.

Overall, most organizational structures are now reflecting today’s multidimensional business reality. Attention is shifting to prepare for the strategic challenges ahead. The main organizational improvement focus is a fresh look at automation (68% of respondents), adoption of agile ways of working (65% of respondents) and building KPI/performance metrics that reflect both the performance versus growth dimension as well as hard versus soft skills (68% of respondents; see Figure 9). This is likely to lead to a different capability mix across various companies enabling them to explore and exploit, tailored to their specific strategies for the future.

“We have managed to go through a transition phase and successfully implement the strategies required. This makes us better prepared to face the unexpected, yet we need to further improve on this.” — CEO, financial services

The increasing challenge to find and attract talent

When it comes to recruitment, CEOs have long had concerns around demography (replacing retiring baby boomers) and adapting to the changing values of new generations. On the positive side, most are happy with the skills mix within their organization: just 13% see a strong/very strong impetus to drive reskilling (see Figure 10). However, this varies among industries — and in companies within them — as the example of the energy and utilities sector shows. Among energy players, 20% said there was no need for reskilling, yet at the other end of the spectrum, 5% of CEOs in the sector saw a very strong requirement to invest in this area.

There is concern across industries regarding access to talent (see Figure 11). CEOs struggle to organically attract new capabilities and talents and are focused on acquiring them either via headhunters, corporate venture capital, or direct acquisition. Less than a quarter (21%) of key employees are developed internally, with headhunters the favored option for 29% of companies. A greater focus on diversity, equity, and inclusion (DEI) is likely to help attract and retain talent over the long term.

4. Moving beyond digitalization to embrace technologies

As we have seen, CEOs are focusing on technology innovation to drive growth (refer back to Figure 5). Drilling down into where they see technology delivering benefits shows a step change between the past and future (see Figure 12). While the focus previously has been on digital transformation, looking forward this will virtually halve in importance — to just 42% in the future, as traditional technology trends such as digitalization have become commonplace within organizations.

Essentially, ambidextrous CEOs are now moving beyond using technology, such as digitalization, to drive efficiency and optimization and are now looking at large-scale adoption of new technology to provide a differentiator. They want new technology to underpin their growth agendas and help in acquiring and retaining new customers.

To achieve this going forward, CEOs expect artificial intelligence (AI)/machine learning (ML), automation and robotics, and sustainability to significantly increase in importance. They are moving beyond pilot projects to scale technologies and embed them in the mainstream business. This brings higher expectations for delivery from their teams but potentially higher returns as well.

CEOs are contemplating the future with open minds: 60% want to explore new technologies, and 27% believe the Metaverse and virtual reality (VR) will impact their business. They are monitoring and piloting these technologies now, preparing to exploit opportunities once they mature.

ADL experience supports this trend. AI applications have achieved mass market penetration and are making a significant difference in our societies. For example, they are underpinning new modes and means of transportation, better access to mobility systems, new and bidirectional energy management systems, and automation and automomy enabled by new telecom-connectivity systems. All of this will lead to progressive and radical changes to our economies and societies, and CEOs are focused and active in understanding and acting on the implications of technology breakthroughs.

5. ESG factors become core

ESG is becoming a full part of the CEO agenda, and increasingly it is seen as an opportunity rather than a threat (see Figure 13). While two-thirds of CEOs admit they pursue ESG targets and goals for compliance reasons, 80% see it as a source of competitive advantage, with 67% referencing consumer pull as a further reason for pursuing greener, more sustainable strategies.

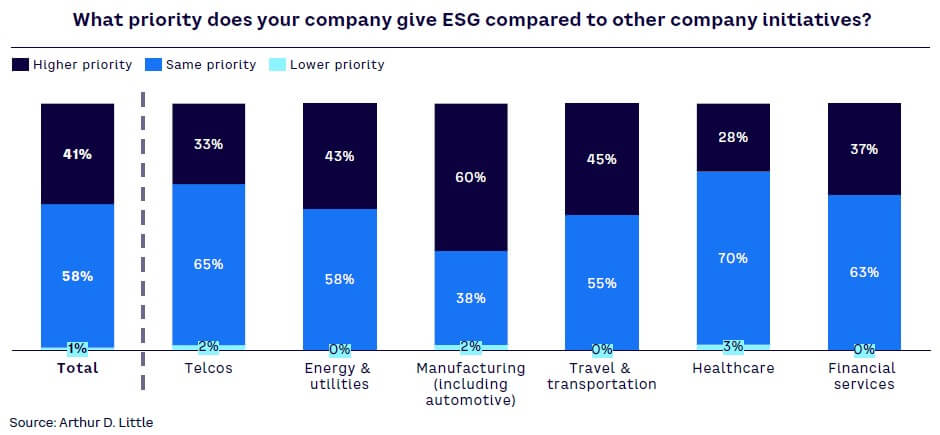

ESG is also rising in strategic importance, with 41% of CEOs making it a higher priority than other initiatives (see Figure 14). Only 1% rank it as a lower priority. Unsurprisingly there is a clear difference between sectors: 60% of carbon-intensive manufacturing companies see it as a higher priority, compared to just 28% of healthcare companies. Increasing the focus on sustainability and committing to targets such as those within the UN’s Sustainable Development Goals (SDGs) delivers wider benefits in both responding to customer needs and attracting today’s purpose-driven generations of employees.

Successful CEOs are moving beyond talk to taking action on sustainability. Based on ADL work and research, we see five key actions to embed sustainability within a company’s operations and governance:

-

Adopt an ecosystem approach, positioning themselves through collaboration with nontraditional partners.

-

Integrate sustainability indicators, reporting, and tools at the core of the business, and incentivize senior management based on these indicators.

-

Redefine their culture and build new capabilities and internal governance.

-

Focus on sustainability technologies and look more widely for innovation beyond traditional value chains.

-

Develop and adopt new business models built on sustainability.

2

HOW SECTORS COMPARE

We have already seen how CEO thinking and actions vary between geographic regions. Unsurprisingly, attitudes show differences across sectors as well, with current and future trends impacting them in distinct ways.

Some sectors are undergoing more radical transformation than others, especially those driven by convergence, which is enabling new opportunities but adding complexity. In the travel and transportation sector, for example, all players are gearing up to address a major shift in the classical paradigm of mobility management. This new mobility will be electric (with a lower carbon footprint), fully integrated and intermodal, and more autonomous, but also more demand and efficiency oriented. Around this paradigm a variety of new services will emerge to be addressed by traditional and new players, all of them working in stronger partnerships and ecosystems. In addition to transportation companies, these ecosystems will involve players such as energy suppliers, automotive manufacturers, telco companies providing connectivity, and even government agencies. CEOs understand that these trends go far beyond the current global crisis and are acting and planning accordingly.

These differences between sectors are particularly highlighted in three areas: (1) optimism for the future, (2) views on the importance of growth/investment strategies, and (3) the levers CEOs expect to drive the growth.

Future economic outlook

Current turbulence means some sectors are winning while others languish (see Figure 15). For example, 80% of CEOs of energy & utilities companies believe the global economic outlook will either improve or remain stable over the next three to five years. This could reflect the positive side of higher energy prices, particularly among producers. The telco sector is also positive, demonstrating its position as a critical part of everyone’s work and daily lives. In contrast, industries that are not able to benefit from the crisis, such as financial services, are extremely pessimistic, with 59% in that sector expecting a decline in the global economy.

“Every firm can be impacted by an uncertain and unpredictable environment. We were not completely prepared during the pandemic and had a challenging experience. Now, we are preparing for the future by increasing our operational reach and updating technology inside our company.” — CEO, travel & transportation

“Through the methodical implementation of our strategy program and a creative and innovative commercial approach, we have now repositioned the company for growth.” — CEO, telco

The relative importance of growth — and where investments are being made

CEOs in all sectors view growth as vital for their organization. However, there’s diversity in the reasons they want to grow (see Figure 16). Nearly a quarter of manufacturing companies (23%) believe it will help them attract, retain, and motivate top talent — higher than in all other sectors. Growth is seen as most critical to securing the long-term health of the organization, particularly in energy and utilities (cited by 48% of CEOs), demonstrating the large-scale transformation happening in the sector as the world decarbonizes. Financial services is driven most by investor and board expectations (51%), reflecting the more traditional nature of the industry.

“Despite challenging business conditions, we were still able to achieve dramatic growth. Our global efforts to reduce costs meant we achieved our goals three years ahead of schedule. Now we are prepared to handle all the uncertainties that may arise.” — CEO, healthcare

“High volatility and geopolitical tensions continually affect the energy market. We are increasing our production multifold by utilizing different tactics and new updated technologies while keeping resource sustainability in mind.” — CEO, energy & utilities

In the minds of CEOs, future opportunities are not evenly spread among sectors, with a greater number of companies in certain sectors (healthcare, energy and utilities, travel and transportation) aiming to achieve above-average growth rates (see Figure 17). In contrast, just 12% of financial services CEOs are adopting offensive growth strategies, the lowest number in the study.

These different approaches drive investment budgets. Less than a third (29%) of financial services companies will increase their growth investments, with 10% decreasing them. Nearly two-thirds (65%) of energy and utilities CEOs will boost spending in this area, alongside 62% of those in manufacturing. In both these cases, radical transformation required for sustainability are key drivers for CEOs.

Levers for growth

While CEOs in every sector are consistently reducing their focus on their core business, where they are looking for growth varies widely (see Figure 18). Telcos and energy and utilities CEOs are dramatically increasing their efforts around disruptive innovation and expansion into new geographies. Energy CEOs are aiming to be truly ambidextrous, also accelerating their emphasis on cost optimization and seeing the largest drop in focus (42%) on their (previously) core business.

Perhaps surprisingly for a sector noted for a constant focus on process improvement, manufacturing is moving away from cost optimization, instead embracing new sales channels and new geographies. Reflecting the sector’s static, rather pessimistic view of current opportunities, financial services CEOs are planning a seven-fold increase in M&A investments to drive vertical integration as they battle new competitors.

“A diversified investment portfolio will work to our advantage. We are planning more investments in technology and fast-growth sectors.” — CEO, financial services

“Concentrate on twin transformations to withstand economic shocks. One would be looking for raw material substitutes and the other would be an investment in technology.” — CEO, manufacturing

CONCLUSION: FORTUNE FAVORS THE BRAVE

It is easy to become disheartened in current times. Short-term challenges, such as inflation, and longer-term issues, such as climate change, have swiftly followed the global pandemic, which continues to cause death and disruption.

However, ADL research demonstrates that, globally, CEOs of our largest companies are embracing the positive and seeing the opportunities that arise from turmoil. They have a growth focus and are confident that a combination of pandemic-hardened organizational structures and innovation will allow them to thrive, rather than just survive. Across sectors and geographies they are combining this focus on growth with cost optimization, building agile, ambidextrous organizations that can innovate while increasing productivity.

Based on the five broad trends that emerged from our 2023 survey and that we have discussed above, we have defined 10 CEO imperatives to help companies remain competitive, both now and in the future.

Trend #1: Build a new future for the company

-

Pursue a growth-oriented strategy. The vast majority of companies are maintaining or increasing their investment in growth. Going forward, this means a fundamental revisit of strategic plans and priorities to reflect this desire for growth. Companies now need to develop strategies to identify new markets, customer segments, and new products to actively shape the business portfolio of the future while keeping an eye on profitability. The survey shows that CEOs believe that the current economic climate presents unique opportunities for expansion and diversification that can only be captured through a growth-oriented strategy.

-

Engage proactively with government stakeholders. CEOs realize that governments are restructuring and revisiting regulation to respond to societal crises. Companies that engage constructively with policy makers will be able to secure their futures. Companies must actively shape policy and regulation, particularly around decarbonization and sustainability, to become the winners of the future.

Trend #2: Lead an ambidextrous agenda

-

Balance resource allocation between optimization and growth/renewal priorities. CEOs have stated a desire to maintain a good balance between optimization and growth/innovation priorities, building an ambidextrous strategic agenda for the company. We believe that this balance must be enabled with the right level of capital and workforce deployment. Keeping this in mind, companies should ensure adequate budget and, more importantly, leadership bandwidth allocation to strike the right balance between innovation and optimization initiatives.

-

Develop programmatic M&A as a strategic lever while doubling down on existing customers. CEOs have expressed dissatisfaction with existing M&A programs. This is driven mostly by expansive fiscal policies inflating asset prices and valuations that have set up most acquisitions for failure, with the buyer overpaying significantly. The new inflationary environment has tempered valuations and, with dropping P/E multiples, we believe that acquisition targets have become strategically affordable as a result. While continuing to focus heavily on existing customers, CEOs can put past M&A disappointments behind them to build programmatic M&A initiatives supported by thoughtful integration capabilities.

Trend #3: Shape the organization

-

Fill capability gaps. CEOs believe that now is not the time to indulge in time-consuming changes of organizational structure but instead to strengthen the existing organization. As a result, companies should proactively seek out and develop the right talents, whether internally, through acquisition, or via headhunters. At the same time, companies should focus on encouraging more organizational diversity by widening the range of experiences and backgrounds of prospective employees to match changing business and customer needs.

-

Build organizational agility. An ambidextrous strategic agenda will need an ambidextrous organization. Companies should strive to break down silos, encourage cross-functional teaming and collaboration, and encourage more risk taking and innovation. At the same time, revisiting KPIs/key responsibility areas (KRAs), and objectives and key results (OKRs) to encourage and incentivize innovation will help create the right motivation for employees to think outside the box.

Trend #4: Leverage technology

-

Build a comprehensive technology transformation agenda beyond process digitization. COVID-19 drove companies to embrace process digitization, driving cost reduction and enabling WFH. CEOs recognize that technology is a key driver for growth, innovation, and cost optimization. Going forward, companies need to embrace newer technologies such as AI, robotics, and the Metaverse to increase revenues, enable innovation, and sustain/ensure market differentiation.

-

Invest in scaling technology usage from pilot projects and sandboxes. CEOs realize that advanced technologies need to be embedded in business models to drive full value realization. Going forward, companies should scale investment in new technologies, moving away from pilot projects and sandboxes. As investments in technology scale, companies could consider measuring return on investment in technology (RoIT) and incorporating this in company and employee dashboards.

Trend #5: Move ESG into the core

-

Move from intent to action on ESG. CEOs are beginning to view ESG as a positive and not just a compliance cost. Companies must put sustainability at the core of their business model and engage with customers, suppliers, and regulators. At the same time, CEOs should create and drive multiple strategic initiatives that underpin the achievement of ESG goals and create a culture of positive ESG actions in the company.

-

Craft and execute bold ESG bets. Progressive CEOs believe that ESG could be a source of future business model differentiation and drive the increased acquisition and retention of customers. As a result, companies could craft bold ESG bets such as divesting carbon-intensive operations, investments in new technologies (such as carbon capture and storage), and create an end-to-end green business model. Raising green finance to fund these bets will become increasingly important.

It will take a bold CEO to embrace and drive all of these recommended imperatives, navigate the current turmoil, capitalize on new opportunities, and build the companies of the future. However, our research finds that, increasingly, CEOs leading the largest organizations across the globe have the skills, optimism, and growth plans to thrive in the uncertain future.

Note

[1] Milanese, Stefano, et al. “Overcoming the Challenges to Sustainability.” Arthur D. Little Report, July 2022.

DOWNLOAD THE FULL REPORT

RELATED INFORMATION

Navigating fixed asset reconfiguration in telcos

Telcos have long looked to asset reconfiguration as a lever to increase strategic focus and unlock value. While examples often focused on mobile, reconfiguration now reaches fixed assets and is…

Agile – Turning data overload into meaningful value

In today’s digital environment, companies and their customers are generating increasing amounts of data. Correctly interpreted and used, this overload can be a means of competitive differentiation.…

Turning customers into subscribers – How to successfully make the shift

What customers expect from manufacturing businesses is changing, moving away from outright purchase- to subscription-based models. This offers opportunities and risks for traditional players,…