Getting a grip on decarbonization with effective internal carbon pricing

Regulators and other stakeholders are increasing pressure on organizations to monitor, improve, and share information on their greenhouse gas (GHG) emissions. They want increased transparency around targets, timelines, and plans and are increasingly demanding actual results from decarbonization efforts.

The number of emission trading schemes (ETS) and carbon taxes is rising worldwide. In 2024, 75 carbon pricing initiatives were in place, covering 24% of global GHG emissions. Other countries are discussing implementing their own carbon pricing schemes.

As the world moves toward pricing carbon, organizations must respond by better managing and steering their carbon footprint. They need to start pricing carbon internally, using techniques such as internal carbon pricing (ICP), which contributes to better trade-offs in decision-making and considers the likely future price of externalities (as costs will be gradually internalized in products). Without ICP, procurement and other departments will never be incentivized to purchase and create more sustainable products.

While many companies use ICP, most only deploy it in the margins of their operations. They are not leveraging its potential to become the core of their decarbonization approach, which could satisfy sustainability targets and deliver significant value to the organization. This is partially because providing effective programs in practice is not easy, thanks to the sheer complexity of organizations and their supply chains and an absence of reliable data (both from upstream and downstream emissions). Consequently, many organizations that have launched ICP programs have only applied them to selected Scope 1 (and 2) emissions and set carbon prices at conservative levels, with the actual weight of carbon pricing in decision-making not rigorously set.

Now is the time for organizations to implement and step up their ICP programs to steer and mitigate their carbon emissions in line with their decarbonization strategies. This requires a much more holistic focus, putting in place a comprehensive, data-driven approach built on internal and external sources, starting small and growing to cover all material emissions across Scope 1, 2, and 3. It should enable granular and flexible emissions management by categories such as business unit, geography, type of emissions, or type of decisions, using parameters such as weight in decision-making or current and future carbon dioxide (CO2) price. This will give CEOs a much firmer grip on their decarbonization strategy, enabling them to guide it more confidently and effectively navigate a world where carbon will have an increasingly higher price.

THE NEED TO BETTER MANAGE EMISSIONS

Multiple factors are pushing companies to manage and decrease their GHG emissions:

- Regulatory mechanisms: Many governments have already implemented carbon-pricing mechanisms, such as carbon taxes, cap-and-trade systems (e.g., EU ETS), or the EU’s Carbon Border Adjustment Mechanism (CBAM), to incentivize companies to reduce their GHG emissions. The direction of travel is clear, with new regulations, such as the EU Corporate Sustainability Reporting Directive (CSRD) and the International Sustainability Standards Board (ISSB) S1 and S2 standards, requiring companies to disclose their current GHG emissions, including Scopes 1, 2, and 3. Also influencing this direction are set targets and obligations to report on progress.

- Market-driven mechanisms: Businesses also face pressure from consumers, investors (e.g., ESG [environmental, social, and governance] funds or general investment funds with ESG criteria such as BlackRock), and business partners/customers that have committed to reducing their total emissions and mandate that their supply chains, therefore, better manage their own emissions.

- Legal challenges: Multiple large companies have been sued for damaging the environment through fossil fuel production or not keeping to their publicly declared promises around GHG emissions. For example, in 2021, a court in The Hague, the Netherlands, ruled that Shell must decrease its CO2 emissions by 45% by 2030 in line with Paris Agreement goals, covering both emissions from its operations and those from the use of fossil fuels it produces.

- Voluntary initiatives: Many companies have voluntarily committed to reducing their GHG emissions by setting internal targets or joining programs such as the Science Based Targets initiative (SBTi) or RE100. ICP is critical to monitoring and meeting these targets and engaging the entire business in reducing emissions.

HOW DOES AN INTERNAL CARBON PRICE WORK?

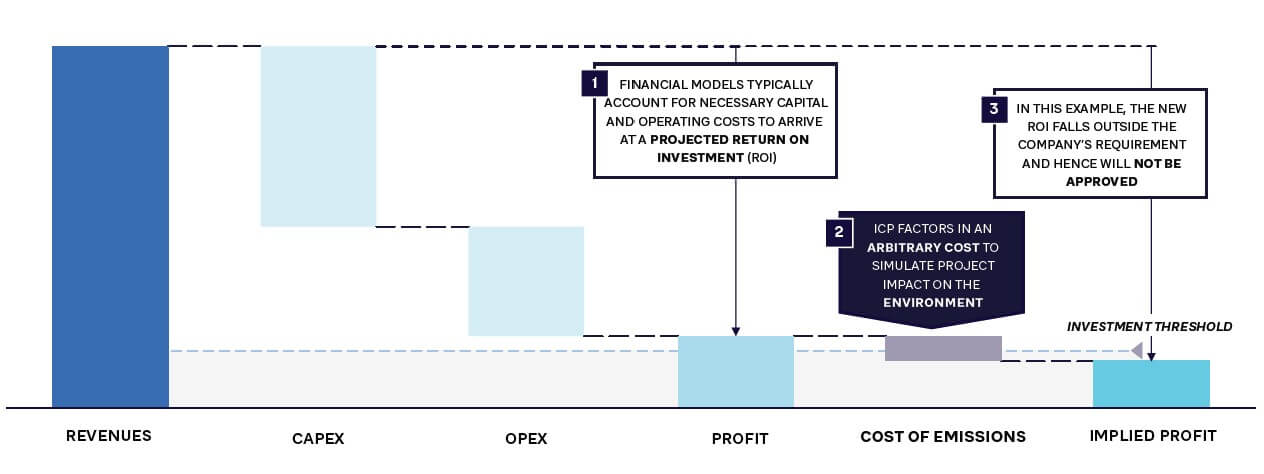

Figure 1 shows how an internal carbon price factors in an additional metric (the financial cost of emissions) when making investment and procurement decisions and generating a projected net present value (NPV). This is then used as part of the calculation to understand whether a project or purchase fits within company ROI thresholds and make a go or no-go decision.

It is important to understand that the ICP’s impact on project approvals can be both negative and positive. It can rule out investments that add significantly to organizational GHG emissions; equally, factoring in the cost of avoiding emissions can enable sustainability projects to go forward, even if they would not have been approved using traditional profitability calculations that did not consider carbon prices.

In terms of legislative requirements, the use of ICP is currently voluntary. New legislation such as the European Sustainability Reporting Standards (ESRS), IFRS S2, and US Securities and Exchange Commission (SEC) Climate-Related Disclosures merely asks:

- If an ICP is used at all?

- If in place, what is the price/t CO2?

In addition, the ESRS and IFRS S2 (but not SEC climate-related disclosures) ask how the ICP is used in decision-making.

THE CURRENT CHALLENGES TO ICP USE

Extending ICP and making it the cornerstone of a more rigorous and effective decarbonization strategy faces two current challenges: the need for reliable data and prioritization among competing concerns.

NEED FOR RELIABLE DATA

Calculating realistic carbon prices for projects requires an accurate understanding of the emissions that an organization generates. This includes emissions created by the organization (Scope 1), emissions from purchased energy (Scope 2), and, increasingly, Scope 3 data from upstream and downstream emissions. Collecting this data and ensuring it is accurate and trustworthy, particularly from outside the organization, can be difficult. It requires a holistic approach and, importantly, relies on buy-in from different business units and external suppliers.

To overcome the lack of reliable data, companies should begin by adopting an estimation method (e.g., spend-based, average data, or hybrid models), which provides an initial understanding of relevant GHG emissions. The weight given to ICP within decision-making should be proportionate to data quality. Suppose companies decide to give ICP greater weight. In that case, they need to gradually move to collecting primary emissions data, including through supplier engagement, and start with areas with a large impact and lower emission data point requirements, such as investments.

PRIORITIZATION AMONG MULTIPLE COMPETING CONCERNS

Companies face many serious issues, including high energy prices, inflation, and unstable supply chains. Given that ICPs are not mandatory, the temptation could be to avoid spending additional time and effort to develop one today. In fact, now is the optimum moment to start — as examples show, it takes time to build an optimal ICP that is fully aligned with the company’s strategy. Businesses can then use it to increase their resilience against future changes in regulations and mandatory carbon prices.

GETTING STARTED WITH ICP

Fully embedding ICP now gives companies greater control over carbon-reduction strategies, demonstrates transparency, increases efficiency, and delivers first-mover advantage, providing a framework for achieving future sustainability targets, as the success of leaders shows.

Successfully implementing ICP requires organizations to focus on the following five areas.

1. INVOLVE ALL KEY CORPORATE FUNCTIONS

Setting an internal carbon price and then using it effectively requires a holistic approach that stretches across key functions, especially:

- Executive leadership: Setting the strategic direction for the ICP initiative and providing necessary resources and commitment

- ESG/sustainability: Contributing expertise on climate change and carbon management, identifying opportunities for emission reductions, and ensuring that the ICP aligns with the overall sustainability strategy

- Finance: Taking a lead role in designing the ICP mechanism, integrating it into the company’s financial systems, and tracking its financial impacts

- Operations: Implementing the ICP within the company’s day-to-day activities, including projects to reduce carbon emissions, monitoring progress, and ensuring compliance

- Procurement: Modifying processes and incorporating the ICP into supplier contracts, ensuring partners are aware of the company’s carbon-pricing policy

- HR: Communicating the ICP to employees and providing support in developing training programs and incentives

- Legal and compliance: Ensuring the ICP adheres to relevant laws and industry standards, managing any implementation risks

- Communications/marketing: Promoting the ICP both internally and externally, highlighting the company’s commitment to sustainability

Getting buy-in from the entire business is vital to drive acceptance and support for the ICP.

2. CHOOSE A MODEL/BENCHMARK

ICP can be applied through a range of models. The most common are:

- Shadow price: This approach calculates the impact of mandatory carbon prices on future business operations and acts as a tool to identify potential climate risks. This approach aims to influence decision-making. About 80% of companies that report using ICP have chosen this approach, including Panasonic and Teijin.

- Internal fee: This approach takes carbon pricing a step further and involves the company charging itself a fee for every ton of carbon emissions it produces (“internal carbon tax”). Based on how it is implemented, it can provide a clear incentive for business units to reduce emissions through payment to the “corporate,” thus generating revenues that can then be assigned to sustainability projects. It is more suitable for companies in low-carbon-intensity sectors, such as technology, financial, and professional services. Companies employing this methodology include Klarna and Swiss Re.

Early in the ICP process, senior leadership should decide strategically on the models and approaches to adopt to support their strategy. This will vary depending on factors such as the industry they are in, the level of current emissions, and how these will be reduced.

For example, in 2019, insurer Swiss Re committed to net zero emissions across the company and introduced an internal carbon price for operations, initially set at $8/tCO2e. This increased to $100/tCO2e in 2021, with a plan to gradually raise it to $200/tCO2e in 2030. As of 2023, Swiss Re’s operational GHG emissions amounted to around 28,000 tons of CO2e, and the 2023 internal carbon tax price was increased to $123/tCO2e. Through this, Swiss Re has generated an estimated US $3.4 million to cover the costs of the carbon removal certificates, which it plans to use to compensate for its emissions while incentivizing business units to take concrete action on emissions reduction. The program is accompanied by other measures, including increasing energy efficiency, switching to 100% renewable electricity, and reducing business air travel.

3. SET THE CARBON PRICE

ICP is being used across sectors with vastly different carbon prices. Therefore, one of the most important tasks for each company is to set its own ICP carbon price. Five key factors should be considered:

- The social cost of carbon: This is based on externalities caused by emitting an additional ton of CO2e into the atmosphere. According to the UN Global Compact, the recommended carbon price should have been at least $100/tCO2e by 2020, the US Environmental Protection Agency (EPA) suggested $190/tCO2e in 2022, and the International Monetary Fund (IMF) sees an international carbon price floor as the only viable scenario that would limit CO2 emissions sufficiently and suggests at least $85/tCO2e by 2030.

- Expected regulatory changes: Assess existing and anticipated carbon-pricing policies and regulations, including carbon taxes, cap-and-trade systems, and other market-based mechanisms. A sufficiently high ICP can help align with future mandatory/regulatory carbon price increases.

- Organizational incentives: To fully leverage the potential of ICP, the chosen carbon price needs to be high enough to influence decision-making. Furthermore, the entire ICP structure needs to be set up to encourage innovation and efficiency.

- Industry benchmarks and market trends: Consider carbon prices adopted by competitors, industry leaders, and other organizations with similar operations and emissions profiles. Figure 2 shows examples of internal carbon prices set by specific companies — these examples are based on CDP data and information from company websites. Monitor global carbon market trends, including the prices of carbon credits and allowances and the direction of carbon-pricing policies.

- Cost of abatement: Estimate the cost of implementing emission-reduction measures. The internal carbon price should be set at a level that incentivizes investments in these measures and technologies.

The internal carbon price should evolve over time, aligning with external developments and internal capabilities’ growth. Japanese chemical, pharmaceutical, and information technology company Teijin launched an ICP focused on Scope 1 and 2 emissions in capital investment in 2021, with a carbon price set at €50/tCO2. In 2023, it expanded to add M&A projects, renewable energy sourcing, and supply chain emissions (Scope 3, Category 1) while doubling the carbon price to €100/tCO2 (see Figure 3).

4. START SMALL AND BUILD

Depending on the organization and its structure, ICPs can be complex to implement, particularly given the often-large range of operations across geographies, legislations, and products; complex and lengthy supply chains; and the volume and quality of data required for all material emission sources. However, rather than risking project failure through overlong implementation time frames, organizations should focus their approach, starting small, piloting, and building from there. For example, they can begin by applying the ICP to major capital investments and move on to major purchases, gradually decreasing the emissions thresholds for inclusion. Starting with the areas that create the largest emissions delivers the greatest scope for improvement.

Companies should not stop with carbon price–adjusted CAPEX decisions. If the impact of carbon emissions did not adjust the relevant future cash flow, EBITDA, or KPIs, a negative effect on their KPIs and bonuses could make executives reluctant to invest. Therefore, a clear and transparent framework for how carbon pricing will impact financial metrics and compensation needs to be developed. For example, Microsoft’s internal carbon fee model impacts operational decisions and is reflected in the financial performance of different business units.

ICP rollouts can be phased. Once the initial framework is in place, ensure everyone is comfortable using it, starting with a low price and low decision-making weight for carbon. This pilots the ICP, making everyone aware of it and providing the ability to check data quality and other processes. After the system has bedded in, move on to monitoring its impact on key areas before increasing the carbon price and its weight in decision-making to the desired level (see Figure 4).

Panasonic provides a strong example of this gradual approach. The company emits approximately 110 million tCO2e/year across its value chain. It implemented an ICP system on a trial basis starting in fiscal 2024, focusing on investment decisions in its Living Appliances and Solutions business, with the carbon price set at ¥20,000/tCO2 (around US $143). From fiscal year 2025, the pilot ICP system will be rolled out more widely, adapting to the characteristics of each business unit. In addition to Scope 1 and 2 emissions, for which its goal is net zero by 2030, Panasonic is using its ICP to target Scope 3 emissions to achieve complete net zero by 2050.

5. MONITOR, STEER, AND ADAPT

ICP models must be designed and tailored to support individual company strategy and objectives. By establishing a comprehensive monitoring view (see Figure 5), companies can then amend key parameters (e.g., the price of carbon in the business units or geographies where it is applied and its weight in decision-making) to steer their strategy in line with wider business goals. For example, they can apply higher costs on some business units or geographies or tighten or loosen particular parameters based on other economic or corporate priorities.

Swedish fintech company Klarna illustrates this ability to adapt. It has set a target of achieving net zero by 2040, with ICP central to its strategy. In 2020, it set a carbon price of $100/tCO2 for its Scope 1, Scope 2, and Scope 3 travel emissions, with remaining Scope 3 emissions priced at $10/tCO2, intending to create accountability and incentivize emissions reduction. In 2024, it increased the price for Scope 1 and 2 to $200/tCO2e. This has generated $7 million since 2021, with Klarna investing much of this money in around 20 climate technology start-ups. Klarna also allows its customers to donate to these start-ups through its app, adding new offerings to its portfolio.

INSIGHTS FOR THE EXECUTIVE

Achieving decarbonization is a journey — and organizations need to ensure that they are moving forward and accelerating their efforts if they are to reach objectives such as becoming net zero by 2050, as well as prepare for ever-tightening regulation. Establishing an internal carbon price and monitoring mechanism delivers robust support to investment and procurement decision-making, steering the organization now and in the future. To ensure success in this complex program, CEOs should:

- Set overall strategic direction around carbon reduction: If decreasing emissions is important, or the growing price of carbon or current or future regulations would significantly impact your company, make ICP the cornerstone of your decarbonization approach.

- Set overall aspirations for ICP: What are the key aims and objectives? Are they to influence decision-making or also to raise money to launch decarbonization projects? This will drive the models and approaches used.

- Start now to give visibility for the future: This is particularly true when planning major long-term investments, such as new factories or facilities, with significant carbon risks and lengthy project timelines.

- Get buy-in from across the business and create cross-functional teams to deliver a cohesive implementation.

- If you opt for an ICF approach, define and communicate early how you will use the funds collected to create additional benefits, including investments in climate technologies.

- Start small and build: First, put the framework in place, then extend it to other key areas, gradually increasing data quality, prices, and weighting to make it an intrinsic part of all investment and procurement decision-making. Develop a clear and transparent framework for how carbon pricing will impact financial metrics and compensation. By the end, you will need a flexible steering tool to help you manage the company into the future based on strategy.

- Finally, additional externalities should be considered in decision-making: For example, water is increasingly becoming a critical issue in many areas, so representative freshwater use and water pollution costs should be factored into relevant decision-making. Social externalities can also be considered and monetized. Companies with mature sustainability strategies consider the costs of over 20 externalities in their decision-making.

Getting a grip on decarbonization with effective internal carbon pricing

DATE

Regulators and other stakeholders are increasing pressure on organizations to monitor, improve, and share information on their greenhouse gas (GHG) emissions. They want increased transparency around targets, timelines, and plans and are increasingly demanding actual results from decarbonization efforts.

The number of emission trading schemes (ETS) and carbon taxes is rising worldwide. In 2024, 75 carbon pricing initiatives were in place, covering 24% of global GHG emissions. Other countries are discussing implementing their own carbon pricing schemes.

As the world moves toward pricing carbon, organizations must respond by better managing and steering their carbon footprint. They need to start pricing carbon internally, using techniques such as internal carbon pricing (ICP), which contributes to better trade-offs in decision-making and considers the likely future price of externalities (as costs will be gradually internalized in products). Without ICP, procurement and other departments will never be incentivized to purchase and create more sustainable products.

While many companies use ICP, most only deploy it in the margins of their operations. They are not leveraging its potential to become the core of their decarbonization approach, which could satisfy sustainability targets and deliver significant value to the organization. This is partially because providing effective programs in practice is not easy, thanks to the sheer complexity of organizations and their supply chains and an absence of reliable data (both from upstream and downstream emissions). Consequently, many organizations that have launched ICP programs have only applied them to selected Scope 1 (and 2) emissions and set carbon prices at conservative levels, with the actual weight of carbon pricing in decision-making not rigorously set.

Now is the time for organizations to implement and step up their ICP programs to steer and mitigate their carbon emissions in line with their decarbonization strategies. This requires a much more holistic focus, putting in place a comprehensive, data-driven approach built on internal and external sources, starting small and growing to cover all material emissions across Scope 1, 2, and 3. It should enable granular and flexible emissions management by categories such as business unit, geography, type of emissions, or type of decisions, using parameters such as weight in decision-making or current and future carbon dioxide (CO2) price. This will give CEOs a much firmer grip on their decarbonization strategy, enabling them to guide it more confidently and effectively navigate a world where carbon will have an increasingly higher price.

THE NEED TO BETTER MANAGE EMISSIONS

Multiple factors are pushing companies to manage and decrease their GHG emissions:

- Regulatory mechanisms: Many governments have already implemented carbon-pricing mechanisms, such as carbon taxes, cap-and-trade systems (e.g., EU ETS), or the EU’s Carbon Border Adjustment Mechanism (CBAM), to incentivize companies to reduce their GHG emissions. The direction of travel is clear, with new regulations, such as the EU Corporate Sustainability Reporting Directive (CSRD) and the International Sustainability Standards Board (ISSB) S1 and S2 standards, requiring companies to disclose their current GHG emissions, including Scopes 1, 2, and 3. Also influencing this direction are set targets and obligations to report on progress.

- Market-driven mechanisms: Businesses also face pressure from consumers, investors (e.g., ESG [environmental, social, and governance] funds or general investment funds with ESG criteria such as BlackRock), and business partners/customers that have committed to reducing their total emissions and mandate that their supply chains, therefore, better manage their own emissions.

- Legal challenges: Multiple large companies have been sued for damaging the environment through fossil fuel production or not keeping to their publicly declared promises around GHG emissions. For example, in 2021, a court in The Hague, the Netherlands, ruled that Shell must decrease its CO2 emissions by 45% by 2030 in line with Paris Agreement goals, covering both emissions from its operations and those from the use of fossil fuels it produces.

- Voluntary initiatives: Many companies have voluntarily committed to reducing their GHG emissions by setting internal targets or joining programs such as the Science Based Targets initiative (SBTi) or RE100. ICP is critical to monitoring and meeting these targets and engaging the entire business in reducing emissions.

HOW DOES AN INTERNAL CARBON PRICE WORK?

Figure 1 shows how an internal carbon price factors in an additional metric (the financial cost of emissions) when making investment and procurement decisions and generating a projected net present value (NPV). This is then used as part of the calculation to understand whether a project or purchase fits within company ROI thresholds and make a go or no-go decision.

It is important to understand that the ICP’s impact on project approvals can be both negative and positive. It can rule out investments that add significantly to organizational GHG emissions; equally, factoring in the cost of avoiding emissions can enable sustainability projects to go forward, even if they would not have been approved using traditional profitability calculations that did not consider carbon prices.

In terms of legislative requirements, the use of ICP is currently voluntary. New legislation such as the European Sustainability Reporting Standards (ESRS), IFRS S2, and US Securities and Exchange Commission (SEC) Climate-Related Disclosures merely asks:

- If an ICP is used at all?

- If in place, what is the price/t CO2?

In addition, the ESRS and IFRS S2 (but not SEC climate-related disclosures) ask how the ICP is used in decision-making.

THE CURRENT CHALLENGES TO ICP USE

Extending ICP and making it the cornerstone of a more rigorous and effective decarbonization strategy faces two current challenges: the need for reliable data and prioritization among competing concerns.

NEED FOR RELIABLE DATA

Calculating realistic carbon prices for projects requires an accurate understanding of the emissions that an organization generates. This includes emissions created by the organization (Scope 1), emissions from purchased energy (Scope 2), and, increasingly, Scope 3 data from upstream and downstream emissions. Collecting this data and ensuring it is accurate and trustworthy, particularly from outside the organization, can be difficult. It requires a holistic approach and, importantly, relies on buy-in from different business units and external suppliers.

To overcome the lack of reliable data, companies should begin by adopting an estimation method (e.g., spend-based, average data, or hybrid models), which provides an initial understanding of relevant GHG emissions. The weight given to ICP within decision-making should be proportionate to data quality. Suppose companies decide to give ICP greater weight. In that case, they need to gradually move to collecting primary emissions data, including through supplier engagement, and start with areas with a large impact and lower emission data point requirements, such as investments.

PRIORITIZATION AMONG MULTIPLE COMPETING CONCERNS

Companies face many serious issues, including high energy prices, inflation, and unstable supply chains. Given that ICPs are not mandatory, the temptation could be to avoid spending additional time and effort to develop one today. In fact, now is the optimum moment to start — as examples show, it takes time to build an optimal ICP that is fully aligned with the company’s strategy. Businesses can then use it to increase their resilience against future changes in regulations and mandatory carbon prices.

GETTING STARTED WITH ICP

Fully embedding ICP now gives companies greater control over carbon-reduction strategies, demonstrates transparency, increases efficiency, and delivers first-mover advantage, providing a framework for achieving future sustainability targets, as the success of leaders shows.

Successfully implementing ICP requires organizations to focus on the following five areas.

1. INVOLVE ALL KEY CORPORATE FUNCTIONS

Setting an internal carbon price and then using it effectively requires a holistic approach that stretches across key functions, especially:

- Executive leadership: Setting the strategic direction for the ICP initiative and providing necessary resources and commitment

- ESG/sustainability: Contributing expertise on climate change and carbon management, identifying opportunities for emission reductions, and ensuring that the ICP aligns with the overall sustainability strategy

- Finance: Taking a lead role in designing the ICP mechanism, integrating it into the company’s financial systems, and tracking its financial impacts

- Operations: Implementing the ICP within the company’s day-to-day activities, including projects to reduce carbon emissions, monitoring progress, and ensuring compliance

- Procurement: Modifying processes and incorporating the ICP into supplier contracts, ensuring partners are aware of the company’s carbon-pricing policy

- HR: Communicating the ICP to employees and providing support in developing training programs and incentives

- Legal and compliance: Ensuring the ICP adheres to relevant laws and industry standards, managing any implementation risks

- Communications/marketing: Promoting the ICP both internally and externally, highlighting the company’s commitment to sustainability

Getting buy-in from the entire business is vital to drive acceptance and support for the ICP.

2. CHOOSE A MODEL/BENCHMARK

ICP can be applied through a range of models. The most common are:

- Shadow price: This approach calculates the impact of mandatory carbon prices on future business operations and acts as a tool to identify potential climate risks. This approach aims to influence decision-making. About 80% of companies that report using ICP have chosen this approach, including Panasonic and Teijin.

- Internal fee: This approach takes carbon pricing a step further and involves the company charging itself a fee for every ton of carbon emissions it produces (“internal carbon tax”). Based on how it is implemented, it can provide a clear incentive for business units to reduce emissions through payment to the “corporate,” thus generating revenues that can then be assigned to sustainability projects. It is more suitable for companies in low-carbon-intensity sectors, such as technology, financial, and professional services. Companies employing this methodology include Klarna and Swiss Re.

Early in the ICP process, senior leadership should decide strategically on the models and approaches to adopt to support their strategy. This will vary depending on factors such as the industry they are in, the level of current emissions, and how these will be reduced.

For example, in 2019, insurer Swiss Re committed to net zero emissions across the company and introduced an internal carbon price for operations, initially set at $8/tCO2e. This increased to $100/tCO2e in 2021, with a plan to gradually raise it to $200/tCO2e in 2030. As of 2023, Swiss Re’s operational GHG emissions amounted to around 28,000 tons of CO2e, and the 2023 internal carbon tax price was increased to $123/tCO2e. Through this, Swiss Re has generated an estimated US $3.4 million to cover the costs of the carbon removal certificates, which it plans to use to compensate for its emissions while incentivizing business units to take concrete action on emissions reduction. The program is accompanied by other measures, including increasing energy efficiency, switching to 100% renewable electricity, and reducing business air travel.

3. SET THE CARBON PRICE

ICP is being used across sectors with vastly different carbon prices. Therefore, one of the most important tasks for each company is to set its own ICP carbon price. Five key factors should be considered:

- The social cost of carbon: This is based on externalities caused by emitting an additional ton of CO2e into the atmosphere. According to the UN Global Compact, the recommended carbon price should have been at least $100/tCO2e by 2020, the US Environmental Protection Agency (EPA) suggested $190/tCO2e in 2022, and the International Monetary Fund (IMF) sees an international carbon price floor as the only viable scenario that would limit CO2 emissions sufficiently and suggests at least $85/tCO2e by 2030.

- Expected regulatory changes: Assess existing and anticipated carbon-pricing policies and regulations, including carbon taxes, cap-and-trade systems, and other market-based mechanisms. A sufficiently high ICP can help align with future mandatory/regulatory carbon price increases.

- Organizational incentives: To fully leverage the potential of ICP, the chosen carbon price needs to be high enough to influence decision-making. Furthermore, the entire ICP structure needs to be set up to encourage innovation and efficiency.

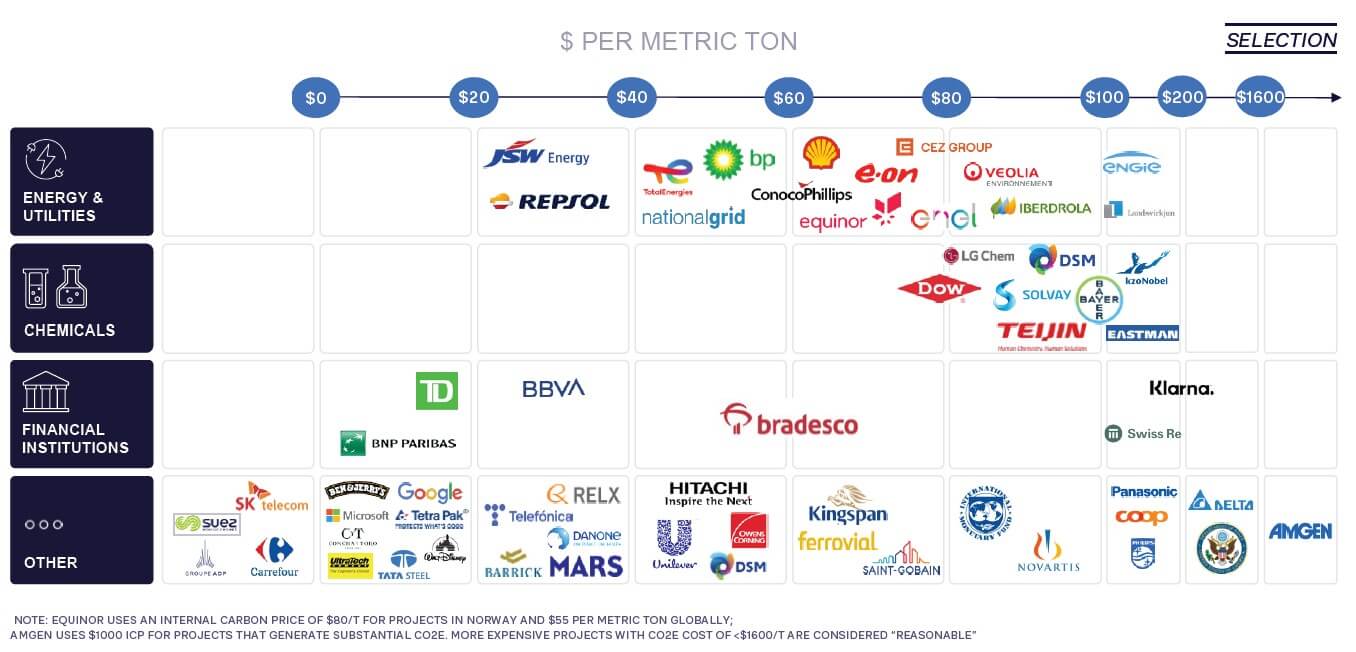

- Industry benchmarks and market trends: Consider carbon prices adopted by competitors, industry leaders, and other organizations with similar operations and emissions profiles. Figure 2 shows examples of internal carbon prices set by specific companies — these examples are based on CDP data and information from company websites. Monitor global carbon market trends, including the prices of carbon credits and allowances and the direction of carbon-pricing policies.

- Cost of abatement: Estimate the cost of implementing emission-reduction measures. The internal carbon price should be set at a level that incentivizes investments in these measures and technologies.

The internal carbon price should evolve over time, aligning with external developments and internal capabilities’ growth. Japanese chemical, pharmaceutical, and information technology company Teijin launched an ICP focused on Scope 1 and 2 emissions in capital investment in 2021, with a carbon price set at €50/tCO2. In 2023, it expanded to add M&A projects, renewable energy sourcing, and supply chain emissions (Scope 3, Category 1) while doubling the carbon price to €100/tCO2 (see Figure 3).

4. START SMALL AND BUILD

Depending on the organization and its structure, ICPs can be complex to implement, particularly given the often-large range of operations across geographies, legislations, and products; complex and lengthy supply chains; and the volume and quality of data required for all material emission sources. However, rather than risking project failure through overlong implementation time frames, organizations should focus their approach, starting small, piloting, and building from there. For example, they can begin by applying the ICP to major capital investments and move on to major purchases, gradually decreasing the emissions thresholds for inclusion. Starting with the areas that create the largest emissions delivers the greatest scope for improvement.

Companies should not stop with carbon price–adjusted CAPEX decisions. If the impact of carbon emissions did not adjust the relevant future cash flow, EBITDA, or KPIs, a negative effect on their KPIs and bonuses could make executives reluctant to invest. Therefore, a clear and transparent framework for how carbon pricing will impact financial metrics and compensation needs to be developed. For example, Microsoft’s internal carbon fee model impacts operational decisions and is reflected in the financial performance of different business units.

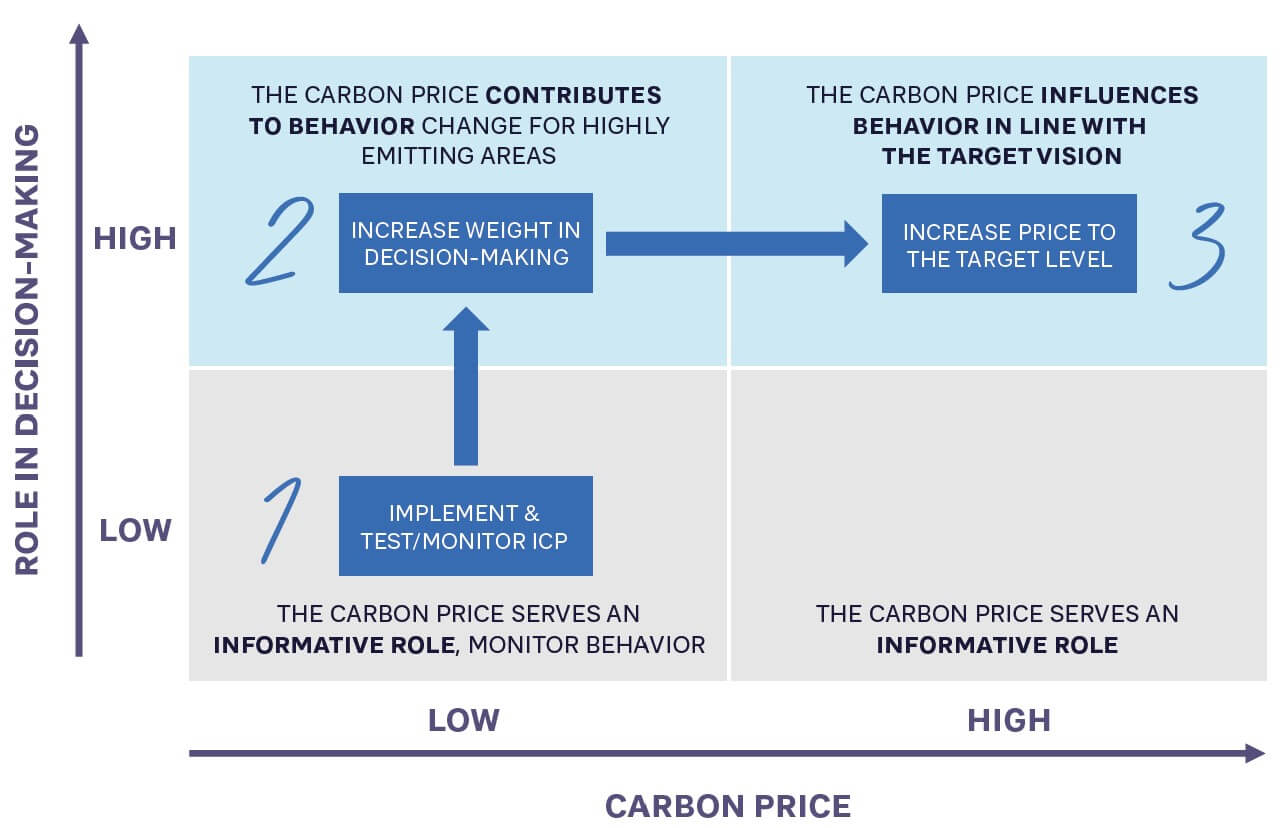

ICP rollouts can be phased. Once the initial framework is in place, ensure everyone is comfortable using it, starting with a low price and low decision-making weight for carbon. This pilots the ICP, making everyone aware of it and providing the ability to check data quality and other processes. After the system has bedded in, move on to monitoring its impact on key areas before increasing the carbon price and its weight in decision-making to the desired level (see Figure 4).

Panasonic provides a strong example of this gradual approach. The company emits approximately 110 million tCO2e/year across its value chain. It implemented an ICP system on a trial basis starting in fiscal 2024, focusing on investment decisions in its Living Appliances and Solutions business, with the carbon price set at ¥20,000/tCO2 (around US $143). From fiscal year 2025, the pilot ICP system will be rolled out more widely, adapting to the characteristics of each business unit. In addition to Scope 1 and 2 emissions, for which its goal is net zero by 2030, Panasonic is using its ICP to target Scope 3 emissions to achieve complete net zero by 2050.

5. MONITOR, STEER, AND ADAPT

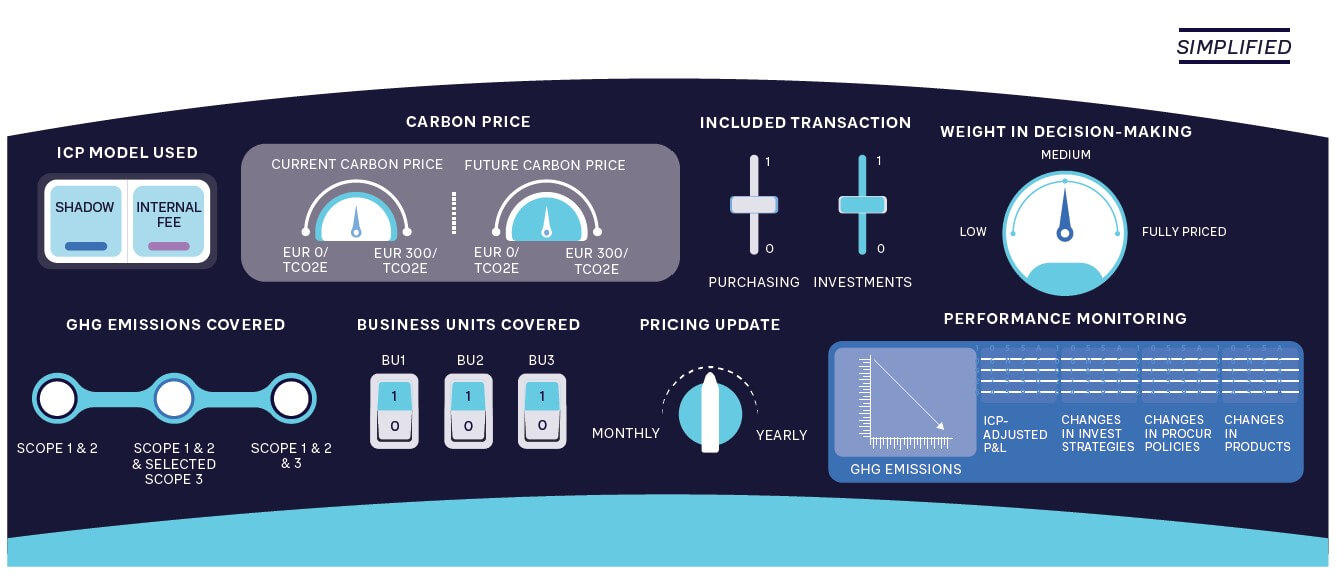

ICP models must be designed and tailored to support individual company strategy and objectives. By establishing a comprehensive monitoring view (see Figure 5), companies can then amend key parameters (e.g., the price of carbon in the business units or geographies where it is applied and its weight in decision-making) to steer their strategy in line with wider business goals. For example, they can apply higher costs on some business units or geographies or tighten or loosen particular parameters based on other economic or corporate priorities.

Swedish fintech company Klarna illustrates this ability to adapt. It has set a target of achieving net zero by 2040, with ICP central to its strategy. In 2020, it set a carbon price of $100/tCO2 for its Scope 1, Scope 2, and Scope 3 travel emissions, with remaining Scope 3 emissions priced at $10/tCO2, intending to create accountability and incentivize emissions reduction. In 2024, it increased the price for Scope 1 and 2 to $200/tCO2e. This has generated $7 million since 2021, with Klarna investing much of this money in around 20 climate technology start-ups. Klarna also allows its customers to donate to these start-ups through its app, adding new offerings to its portfolio.

INSIGHTS FOR THE EXECUTIVE

Achieving decarbonization is a journey — and organizations need to ensure that they are moving forward and accelerating their efforts if they are to reach objectives such as becoming net zero by 2050, as well as prepare for ever-tightening regulation. Establishing an internal carbon price and monitoring mechanism delivers robust support to investment and procurement decision-making, steering the organization now and in the future. To ensure success in this complex program, CEOs should:

- Set overall strategic direction around carbon reduction: If decreasing emissions is important, or the growing price of carbon or current or future regulations would significantly impact your company, make ICP the cornerstone of your decarbonization approach.

- Set overall aspirations for ICP: What are the key aims and objectives? Are they to influence decision-making or also to raise money to launch decarbonization projects? This will drive the models and approaches used.

- Start now to give visibility for the future: This is particularly true when planning major long-term investments, such as new factories or facilities, with significant carbon risks and lengthy project timelines.

- Get buy-in from across the business and create cross-functional teams to deliver a cohesive implementation.

- If you opt for an ICF approach, define and communicate early how you will use the funds collected to create additional benefits, including investments in climate technologies.

- Start small and build: First, put the framework in place, then extend it to other key areas, gradually increasing data quality, prices, and weighting to make it an intrinsic part of all investment and procurement decision-making. Develop a clear and transparent framework for how carbon pricing will impact financial metrics and compensation. By the end, you will need a flexible steering tool to help you manage the company into the future based on strategy.

- Finally, additional externalities should be considered in decision-making: For example, water is increasingly becoming a critical issue in many areas, so representative freshwater use and water pollution costs should be factored into relevant decision-making. Social externalities can also be considered and monetized. Companies with mature sustainability strategies consider the costs of over 20 externalities in their decision-making.