48 min read • Healthcare & Life Sciences

Tomorrow’s life sciences

Insights. Impacts. Imperatives.

FOREWORD

Dear reader,

We are living in an era of rapid scientific progress. It spans across multiple disciplines and is changing not only the medicines available to patients, but also entire healthcare systems, inclusive of researchers, clinicians, payers, providers, regulatory agencies, and untold numbers of patients.

The revolution occurring in healthcare is forcing stakeholders across the industry and all who benefit from healthcare to face a variety of questions: What are the societal implications of these changes? How do they protect health and improve the individual’s chance of cure? And how do they affect the business environment for companies in life and health insurance and the life sciences industry?

We believe that the magnitude and impact of these discoveries and the current changes across healthcare are so significant that they cannot be adequately captured by an isolated view. That is why Arthur D. Little and Munich Re have combined their knowledge, as well as analytical skills, and consolidated them into this joint Life Science Report.

Here we provide a compact and clearly structured overview of the major trends in medicine and healthcare. This Life Science Report provides insights, reveals impacts, and sets forth imperatives for both the insurance and life sciences industries. The common goal: to bring innovations to patients faster and to push the boundaries of insurability.

The Life Science Report highlights some highly relevant global trends and innovations that are already shaping the healthcare of tomorrow. We hope that sharing our experiences and insights in this Report will evoke your interest for further discussion. We invite you to reach out to share your view with us and to shape the future of health together.

— Dr. Ulrica Sehlstedt, Managing Partner, Global Practice Leader Healthcare & Life Sciences, Arthur D. Little

— Anke Idstein, Chief Executive Life & Health Munich, Continental Europe (w/o Iberia, Italy, Malta) and Israel, Munich Re

EXECUTIVE SUMMARY

Aging populations, changing urban and work environments, technical innovations in data processing and analysis, and current advances in diagnosing and treating diseases will not only dramatically transform healthcare but also our way of living. This will have impacts, both positive and negative, on the life sciences and insurance industries, as it is their purpose to provide solutions that prevent and mitigate current and future risks.

The COVID-19 pandemic has demonstrated how developments in multiple areas of medicine and society, as well as ways of living and working, can accelerate dramatically under pressure. As such, medical technologies, digitization of the healthcare system, and telehealth have made significant progress in the last two years. Home care solutions for elderly or chronic disease patients are on the rise, incorporating digital and medical technologies.

This fosters an ongoing decentralization of the patient journey that can provide a higher quality of care, potentially improving quality-of-life and patient-centered outcomes. Decentralization and a rise in home care solutions are necessary and likely beneficial for the aging patient population worldwide. By 2060, twice as many people in the EU will be 65 years or older as those younger than 15 years, and the proportion of very old people will triple. We are seeing these aforementioned changes now. But novel developments in the area of life sciences are on the horizon and will need to be analyzed, understood, and evaluated for their impact.

For this Report, our team has defined five focus topics that reflect the latest developments in the healthcare space that impact players in life sciences as well as in insurance.

Digital health is our starting point and the title of our first chapter. It illustrates tangibly how data and digital technologies will change the patient journey and open the opportunity space for innovative digital health solutions that insurance and healthcare players can learn from. The second chapter looks at new and advanced treatments like immunotherapies, gene therapy, and cell-based therapeutics, and is followed by a chapter about new ways to analyze large-scale biologic data including genomics, as it is a major research field for the development of diagnostics and therapeutics.

Another highly relevant healthcare area that has gained pace and therefore its deserved attention in recent years, especially during the pandemic, is mental health. In an expert interview, world-renowned depression expert Prof. Dr. Dr. Florian Holsboer and Dr. Alban Senn, Chief Medical Officer at Munich Re, discuss current challenges and future solutions in this field. And finally, we explore what is next after COVID-19, what is the threat of the next pandemic, and how life sciences players and insurers could and should prepare to support a more resilient healthcare ecosystem.

1

DIGITAL HEALTH

Insights

Digital health thus far has been used in different contexts, primarily in reference to devices, technologies, and developments in the healthcare system that are related to digitization and electronic systems.

For the purpose of this Report, digital health is the incorporation of digital technology tools and methods into healthcare to interact and treat patients in a better or more efficient way than before and thus improve outcomes.

The digital health field has gained traction in recent years with the increasing maturity of technologies and capabilities around data gathering and analysis. Projections show that in 2025 the digital health services market may grow to a financial volume of nearly US $660 billion.[1] The field was further fueled by the effects of the COVID-19 pandemic on society as person-to-person contact was temporarily restricted and willingly avoided. While prior to COVID-19, healthcare professionals from the US, Europe, and Japan rated the use of telemedicine at 57% across all medical fields, this increased to 73% in 2021.[2]

Digital health is rapidly integrating into the medical field and will transform it. In a 2019 survey with respondents primarily in the US and Europe, 68% of healthcare professionals stated that their company had a digital strategy or was working on one. In 2021 this number increased to 81%, emphasizing the speed at which the digital transformation has picked up recently.[3]

By nature, the healthcare and life sciences industry is data-driven, with business success based on scientifically proven numbers and figures. With digital tools, such as electronic health records (EHRs), remote patient monitoring, or virtual clinical trials management, data volume and complexity increase constantly. Through connected EHRs, medical professionals can access the full medical history of patients including information on test results, treatment record, allergies, demographics, and so on. Digital tools simplify coordination among different providers, such as involved physicians or hospitals and insurance providers — as long as future regulation allows insurers to use information from EHRs. This improved coordination can reduce redundancies in therapy and diagnostics and increase time efficiency by providing all necessary information to every professional in every therapeutic configuration. Patients can receive their intervention earlier, medication and treatment errors are reduced, and the standard of care increases through greater continuity.

In combination with other digital tools and technologies, EHRs can also be integrated into a larger digital network of services, such as for disease monitoring. Together, these tools can provide on-demand test results, subsequently set up necessary appointments, or send reminders for regular checkups, vaccinations, or screenings.

All these digital health tools, services, and devices can help facilitate the patient-centered journey through the healthcare system to support innovation and find solutions for the most pressing healthcare problems. For patients, ubiquity and linkage of digital health signifies an increased incorporation of various technologies across their medical experience, rather than an isolated usage of a single selected digital application for a certain point in time.

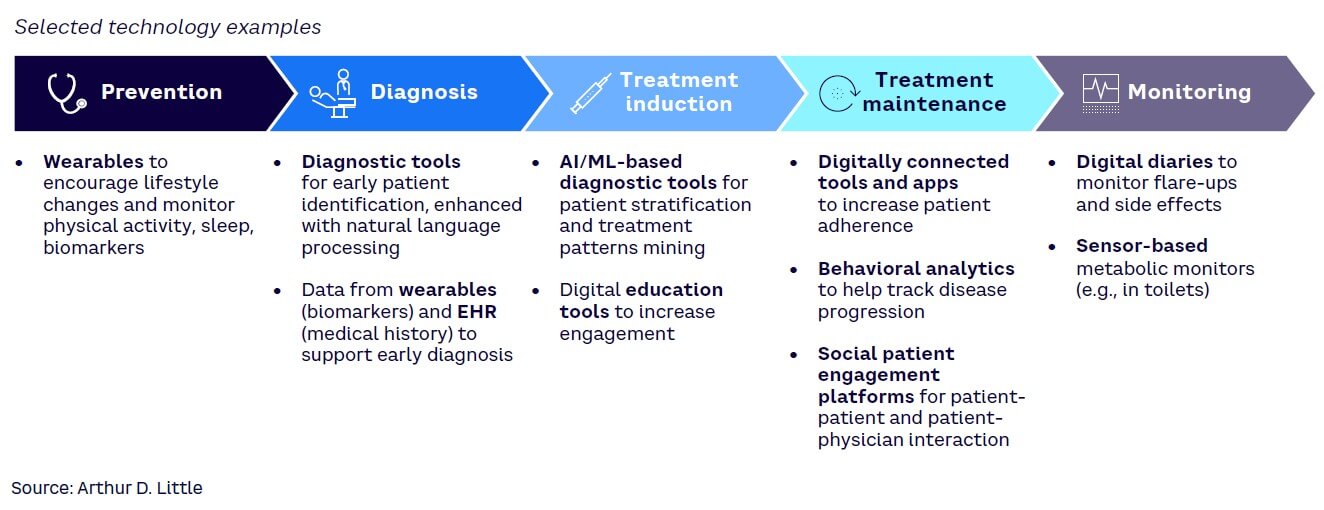

A patient’s journey can largely be divided into five steps: prevention, diagnosis, treatment induction, treatment maintenance, and monitoring. Each aspect can be closely tied with various digital services, tools, and devices (see Figure 1).

Incorporating technology across the various steps of the patient journey generates vast amounts of connected data, which subsequently can be interpreted using current and ever-improving capabilities. Such volumes of data and the possibility to integrate different data sources in the analysis present powerful tools, as they can be used by different stakeholders to further enhance the five steps of the patient journey.

This will, however, require a clear ecosystem approach with some form of a digital hub that allows for safe and compliant collection, processing, analysis, and data sharing across key ecosystem stakeholders (doctors, patients, payers, hospitals, research institutes, drug developers, etc.) as well as enabling the adoption of new technologies (e.g., artificial intelligence [AI]/machine learning [ML]).

Technology alone, however, is not sufficient to drive the digital health transformation. Digital health solutions have the potential to contribute to measurable improvements in longevity or morbidity but improving a hard endpoint such as survival simply by adding a single technology to the patient journey seems overly optimistic.

Essentially, a digital solution such as a health app is often targeted to a specific disease in a specific stage (e.g., severe forms) for a selected patient group (e.g., certain age groups). This is a similar approach to pharmaceuticals, which are usually tested and introduced in selected patient populations.

However, in contrast to pharmaceuticals that usually aim at reducing mortality or morbidity (e.g., reducing hospitalizations), a growing number of health apps aim for the improvement of health status, patient engagement, adherence, and quality of life, which are so-called soft endpoints for studies. It is so far unknown whether they become ineffective over time or if their adherence by users is long lasting.[4] But these aspects are crucial for becoming a valuable tool for comprehensive disease treatments and being cost-effective in the long term. Several studies have already shown a beneficial impact in the field of mental health[5] (e.g., improving symptoms of anxiety or even preventing depression)[6] and are now in practical use.

In addition, clear regulations regarding data privacy and use are essential. The more homogenous these regulations are across geographies, the more rapidly players will enter the market to provide solutions.

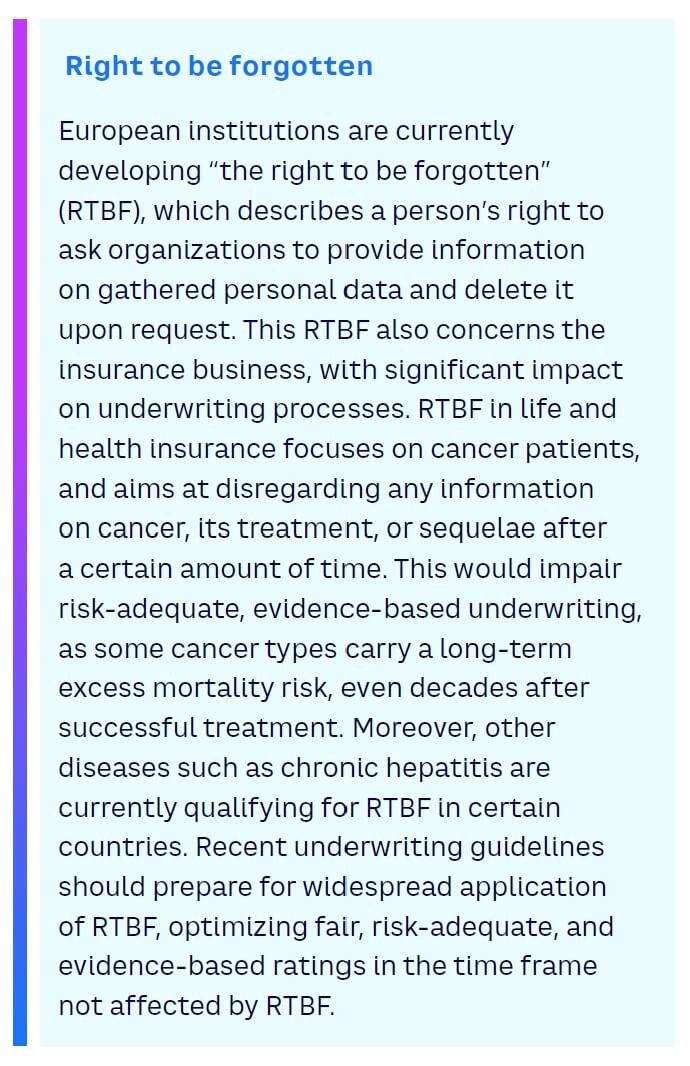

That being said, it is expected that significant differences will remain among key markets, especially the North American and European markets. The American market in particular is more open to the use of personal health data, even as there are clear regulations, such as the Health Insurance Portability and Accountability Act (HIPAA), which set limitations. While companies will continually push for increased sharing and use of data across all geographies, regulatory agencies will be forced to balance those requests with patients’ legitimate privacy and ethical concerns (for more information, see sidebars “Right to be forgotten” and “What is data ethics?”).

Impact

The incorporation of digital health into the patient journey and the subsequent possibility of data extraction and analysis will impact various stakeholders in the pharmaceutical field, including:

- Patients. Patients will benefit from the remote delivery of care through virtual platforms (e.g., telemedicine or mHealth) as well as the added transparency and availability of information. And, with the increased ability to self-manage and monitor their disease together with healthcare providers, they will also feel more empowered.

- Healthcare providers. Ultimately, data will have to be augmented with the right clinical decision support tools across the whole patient journey, enabling providers to become more efficient and reducing some of the barriers between providers and patients. This will not only be an opportunity to concentrate more on the patient, but also to have a more informed and engaged patient dialogue supported by much improved visualization of the data and the disease status.

- Life sciences companies. The large sets of data that are being generated by technology use (as a result of a growing need for real-time data/evidence) can affect treatment algorithms and preferences among physicians and regulatory bodies. Consequently, drug developers need to monitor data prior to and after the launch of their drugs. During the clinical development, digital solutions (e.g., data analytics in clinical trial design, decentralized clinical trials with remote patient monitoring, digital biomarkers) are leveraged for a faster time-to-market with enriched clinical data.

- Medtech companies. The integration, interchangeability, and monitoring of data as part of medtech solutions will be critical and must be based on a better understanding of how digital health and medtech solutions will interact and ultimately improve outcomes.

- Regulators. As the field matures, an increasing number of digital health solutions will be put forth for regulatory approval. At the same time, integration and acceptance of technological tools in clinical development will require regulators to review the large volumes of data those tools generated. In addition, safety and data privacy and security must be addressed from a regulatory perspective.

- Insurers. A major part of the insurance business is based on an accurate risk assessment. The use of AI- or ML-supported models based on relevant insured data could improve risk prediction in underwriting by finding novel or more relevant parameters beyond traditional and population-oriented evidence-based methods from traditional medical knowledge. These new models rely on structured and standardized data, which must be formed and delivered by insurers to fully harness the potential of this technology.

First models currently are being developed to either simplify and accelerate the underwriting process with ML methods, asking only for the minimum necessary information to achieve an adequate risk assessment, or to improve risk prediction by using novel AI-supported models within large data pools extended also by third-party data. It remains to be seen whether, with limited applicant information going into the underwriting process, a superior risk prediction is possible beyond conventional actuarial and insurance medicine methods.

Whether these new approaches in underwriting can replace existing methods will be clarified over the coming years. Beyond improving prediction, this technology could streamline and accelerate decision processes in underwriting or claims handling and thereby reducing current sales barriers as well as administrative costs.

Together, the integration of digital technologies in prevention, diagnosis, and treatment increases the convenience and quality of life for patients. With the vast amounts of data that can, should, and must be interpreted by different stakeholders, medications and treatments can reach the patient earlier and more effectively (with the right medications at the right time in the right dose) to ultimately improve outcomes.

Imperatives for healthcare & life sciences players

Digital technologies are sweeping the healthcare and life sciences field, which requires their adoption into the player’s existing services, platforms, and processes. This can be achieved largely through a five-step approach:

- Looking inside. Adapting to the new digital environment is key. To do so, organizations must assess their current standing and find out which digital skills, tools, and processes are already present and integrated.

- Assessing potential. Analyzing the potential improvements and benefits of digital health and the pain points that will be addressed by these solutions is an important step in identifying the right vision for a specific organization or player.

- Looking outside. Players must understand which digital trends will shape the market in the future and establish a proactive rather than reactive position to respond to coming disruptions.

- Analyzing the gap. With the understanding of internal capabilities and prediction of the future landscape, players must identify the current gaps and assess the potential solutions. Then, they can outline and prioritize a fitting strategy based on the stakeholder’s goals.

- Bridging the gap. Challenging old structures, creating new frameworks, updating processes, and establishing new ways of thinking are imperatives in preparing for the digital advances and accessing their full potential.

For some pharmaceutical companies, these steps may identify key gaps that are difficult to fill in-house and may require a search for an M&A target or partnership. Such collaborations are an increasing trend in the pharmaceutical arena, as illustrated by recent partnerships between Pfizer and Iterative Scopes, between Thermo Fisher Scientific with Medidata Acorn AI, and between Gilead and AWS. Essentially, players across healthcare and life sciences will have to develop strategies to adopt and incorporate the technological transformation with an integrated ecosystem and collaboration approach in order to move into the digital future. This will require a much stronger collaboration between healthcare and life sciences players, spanning from traditional pharma to medtech, as well as integrating healthcare providers.

Imperatives for insurance

Current and future technological developments will change health systems massively. Some changes have already had an impact while others still need some time. However, insurers should closely follow digital health trends and consider performing the following tasks to be prepared:

- Consult experts on digital health in the industry and within the healthcare system about whether current and future digital health solutions could have a profound impact on disease prevention or therapeutic improvements and, finally, mortality and morbidity.

- Implement a data strategy to structure and standardize portfolio data and process data to enable in-depth data analysis for improving key elements of the business model.

- Foster data literacy in the company, providing the skills and knowledge employees need to support the exchange and foster co-creation between domain experts and data analysts with the objective to further harness the power of data.

2

ADVANCED THERAPEUTICS & NEW PARADIGMS IN TREATMENTS

Insights

Over the past decade, a new paradigm in treating severe diseases has become reality. Patients can now be treated with personalized, highly specific, and very effective drugs based on their individual disease characteristics and even their genetic patterns. These innovative therapies encompass various approaches such as immunotherapies, gene therapies, and cell therapies. Immunotherapies harness the patient’s own immune system to fight tumors, and targeted molecular therapeutics aim at specific molecules involved in the growth and spread of cancer cells.

Therapeutic advances, be they data- or technology-driven, have significantly reduced mortality by transforming once-fatal diseases into chronic conditions and by providing options for one-time cures, particularly for many cancers. Heavy investments in the field — like the $1.3 billion venture capital spending on gene therapy companies alone in 2021[7] or the leading cancer drug being immunotherapy with sales of $17 billion in the same year — indicate the rapid developments and high economic interests in advanced therapeutics.

Immunotherapies and targeted molecular therapeutics have improved survival and morbidity in many cancer patients. For example, in advanced stages of melanoma, immunotherapies have significantly increased the life span of patients: 20 years ago, the life expectancy averaged six months whereas today, more than 50% of patients are alive after five years.[8] In 2011, only 2% of cancer patients were eligible for so-called immune checkpoint inhibitors, a number which has risen considerably to an estimated 50% today.[9] These therapies thus far have focused on metastasized cancers but are now moving into non-metastasized tumors. Such advanced treatments have pushed or are pushing some of their indications from a high-mortality, short life expectancy disease to moderate-mortality, chronic disease, raising multiple implications for both the life sciences and insurance industries.

At the same time, gene and cell therapies have seen a renaissance in recent years. These therapeutic advances aim at restoring dysfunctional genes in patients by replacing or editing the genetic code. They offer a lasting cure, with less morbidity and potentially less mortality in the midterm future. Curative cases in oncology are already available: patient-derived, genetically modified Chimeric Antigen Receptor T-cell therapies (CAR-T) have been found to cure patients, with those treated 10 years ago still alive today.

Gene therapies based on technologies such as CRISPR-Cas (“gene scissors”) can directly edit a patient’s genome to provide a one-time cure. These technologies may also become a core treatment pillar beyond oncology and especially for rare genetic diseases, from which almost 10% of all Europeans suffer. In 80% of these rare diseases, a genetic origin is likely.[10]

We estimate that within the next 10 years, a significant number of genetic diseases could become curable, considering that 13% of the drugs indicated as being developed for rare diseases are precision therapies based on specific molecular targets.[11] More than 300 clinical trials are currently investigating gene therapies for different diseases.

Impacts

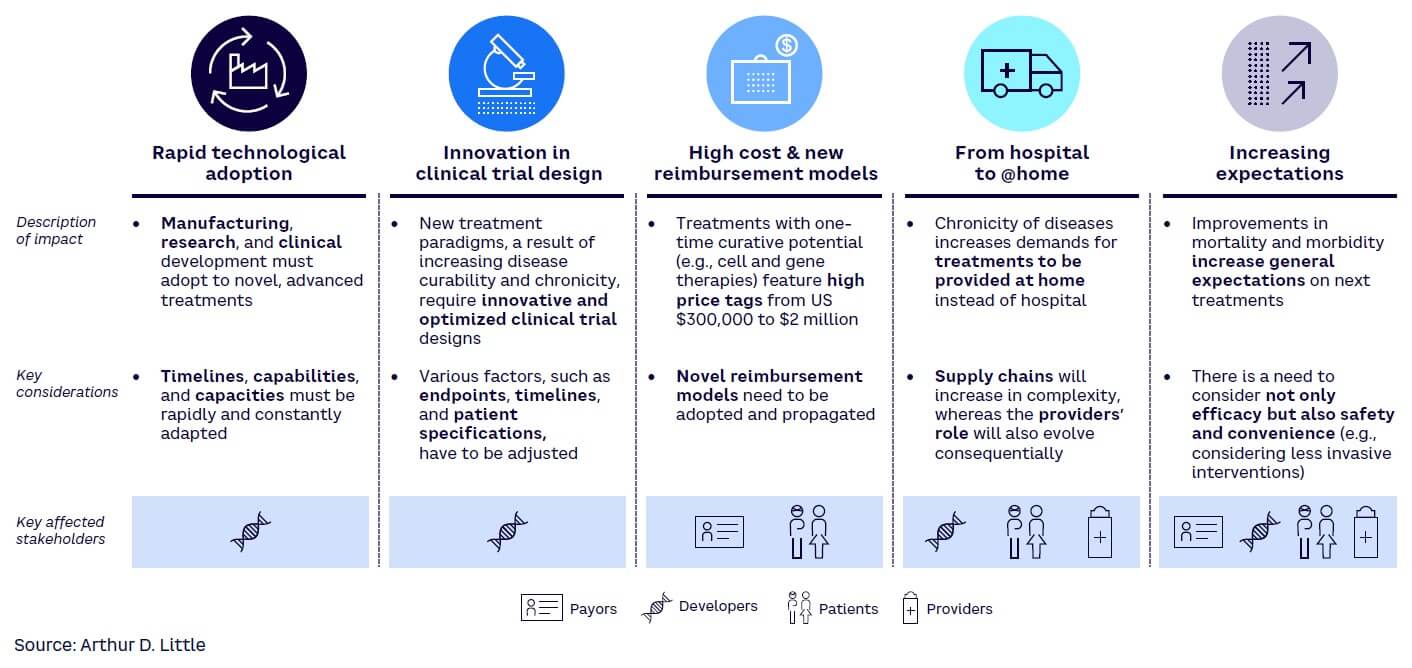

Advanced therapeutics aim to make once-fatal diseases chronic or cure them altogether. Consequentially, they are changing and will continue to change the treatment paradigms as we currently know them. This has multiple key implications on various healthcare and life sciences players (see Figure 2 for a selection of key impacts).

Advanced therapeutics will change how drugs are developed and provided. For the developers, which include not only drug and medtech developers but also manufacturers (e.g., contract manufacturing organizations) and research experts (e.g., contract research organization), this presents not only new assets and growth opportunities but also complexities with short timelines.

Patients as well as providers and payers will face the dilemma of having higher-priced drugs but with the increased benefits and ultimately lower long-term costs based on the possibility of being treated at home or even cured. Payers and providers will also face increasing drug prices and the need to balance the economics with societal benefits, especially in the case of curative gene therapy, which has extremely high costs initially but likely long-term economic benefits. Currently, this is stretching all healthcare systems and will require alternative financing and payment models.

For health insurers, the initial costs of novel therapies are high. For one type of lung cancer, for example, the costs of current immune checkpoint inhibitors can reach up to $100,000 per year compared to $9,000 for the previous standard therapy.[12] Especially in cases of therapeutic response such as when the tumor is effectively reduced, the costs of ongoing therapies increase in a linear manner. This will likely elicit discussions with medical societies and healthcare providers to give clear guidance on therapy duration and introduction of cost policies. As with all novel therapies, patents will expire and biosimilars will provide less costly alternatives.

In fact, the immune checkpoint inhibitors mentioned above will lose their patent protection from 2026 onward. Lower costs for these drugs will shift cost-effectiveness into a more financially sustainable direction for healthcare providers and health insurers. Value-based pricing could be a method to estimate the added benefit for the individual patient and to mitigate “overspending” on treatments that have only minimal added benefit.

Still, assessing cost-effectiveness is highly specific to the respective markets and heavily influenced by public healthcare policies. Life and health insurance are also affected by this new treatment paradigm. Considering cancer and life insurance, insurers currently offer substantial, but risk-adequate, premium loadings for regionally metastasized cancers and decline the majority of applicants with distant metastasized tumors due to their high mortality and disabling morbidity. If cancer patients have fewer long-term side effects, a longer life expectancy, and less morbidity due to these advanced therapeutics, insurability could be extended, even for metastasized disease.

With this progress in mortality and quality of life, cancer survivors could potentially return more frequently into an active work life after initial disability. Since cancer is one of the key claims drivers in life and health insurance in many markets worldwide, there is a need for effective measures to ensure that reactivation of occupational disability from this cause is considered.

Furthermore, a substantial impact on critical illness (CI) products is very likely, as cancers comprise the largest disease group covered by this insurance product. If several cancers or at least stages of certain cancers lose their negative effect on prognosis and disability, CI definitions will have to be adapted. Even regionally metastasized cancers could lose their debilitating effect after treatment and would not trigger a claim. On the underwriting side, some cancer types would receive favorable loadings or could become insurable for CI products.

Similar to cancer, insurance applicants with severe genetic disease are offered, if any, high premium loadings due to the disabling nature and up-to-now limited therapeutic options. Curative gene therapy that abolishes disease morbidity could extend insurability to these persons, offering novel products to new customers.

Imperatives for healthcare & life sciences players

Advanced therapeutics will shape how our healthcare systems are set up in the future and will require new approaches to deal with the associated challenges, such as drug development, costs, manufacturing, supply chain, and expectation management. The consequential shift in treatment paradigms brings unprecedented opportunities and complexities for which all stakeholders need to prepare, assess, and transform their organizations and business models.

As all stakeholders are affected by the new treatment paradigms, the specifics of the different steps may vary. But since the advances in therapeutics will affect all players, preemptive steps are necessary to be best prepared. Of particular importance is the development and implementation of highly coordinated supply chains that link patients, doctors, analytics organizations, drug developers, and manufacturers to bring advanced therapeutics to the bedside where and when they are needed. This will require the support of an integrated healthcare ecosystem comprised of private and public payers to provide the necessary reimbursement to fund both current treatments and the development and implementation of the next generation of therapeutics.

In addition, participating ecosystem players must not only ensure the effectiveness and added value of the treatments, but also that healthcare providers have the right capabilities and infrastructure to deliver these new advanced therapies at scale.

Imperatives for insurance

Advanced therapeutics may only have indirect consequences for insurers, but these can be of high relevance as they can impact different parts of the insurance value chain. In response, insurers should:

- Identify how the current insurance portfolio is affected by advances in the fields of cancer treatment, as this is the most relevant disease group for many insurance products in the life and health sector. Treatment costs may be expensive today but will decrease going forward.

- Consider advanced therapeutics in product development as new treatments may require updates in product definition or even completely new product solutions.

- Update medical risk assessment guidelines accordingly in defined intervals with risk-adequate loadings that reflect improved survival and the diminished disability of cancer survivors or patients with genetic diseases treated with advanced therapeutics.

- Consult with internal and external experts to determine if and under which circumstances persons with rare genetic diseases should become part of the portfolio, potentially expanding insurability to a group of thus far uninsurable persons.

3

POWER OF GENES & OMICS

Insights

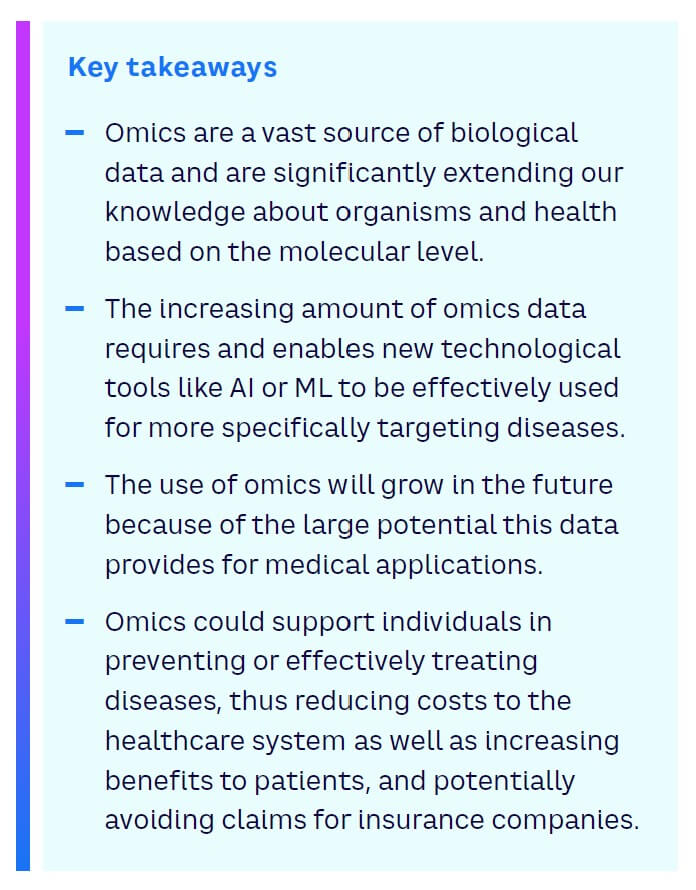

The secrets of the human genome are increasingly being demystified — and thus its impact on our health is becoming more prominent. Findings from so-called genomics are helping to develop new and much more personalized treatments or therapies, as well as allowing the identification of personal risks at a very early stage. The success of messenger RNA (mRNA)-based COVID-19 vaccines now provides a classic example of how genomic data from the virus was used to rapidly develop a pharmaceutical product.

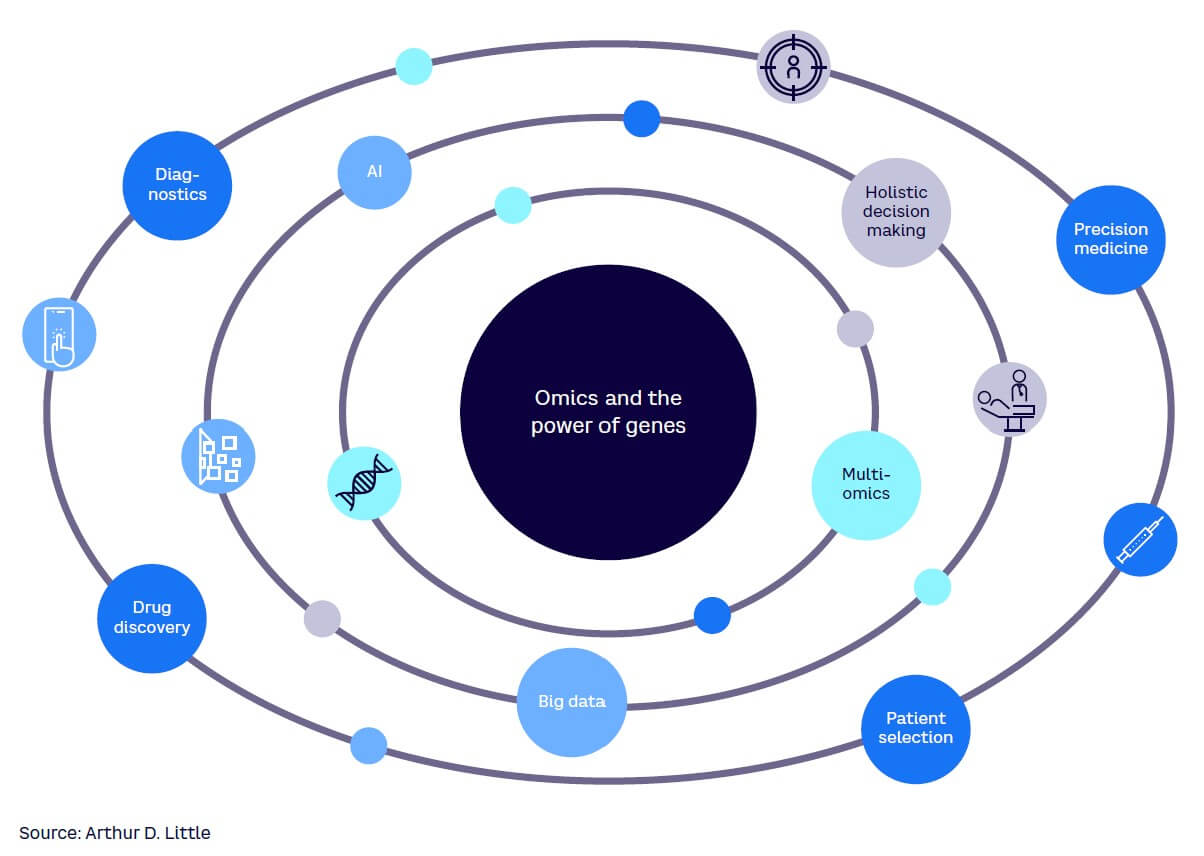

Beyond genes, large-scale biologic information can be gathered from other pools of molecules to generate transcriptomics (the study of RNA produced from the genome), proteomics (the study of proteins in an organism), and metabolomics (the study of molecules and products processed by cells, tissues, or organisms), among others. The science delves into various aspects of biomolecules such as structure, function, and modifications and how they respond to different stimuli. Together, the different omics[13] vastly expand the breadth and depth of our understanding around human physiology and pathology, including insights into disease development and treatment effects.

The availability of the data will enable further advances in the fundamental understanding of the most complex biological systems, including the central nervous and immune system, while also pushing the medical science to ever-increasing personalization of medicine.

Additionally, the application of predictive testing is rising with the massive drop in costs of detecting genetic abnormalities. In fact, depending on the country, whole genome sequencing services are now offered for less than $500, and an increasing number of providers offer testing in and outside of clinical settings.

Already today, selected data from omics is widely used, for example in certain types of cancer to screen for drug responsiveness and likelihood of adverse effects. In breast cancer, for example, decisions on treatment regimens can be determined by the gene expression profile of cancer cells (among others, through the presence of the so-called human epidermal growth factor receptor 2). And, recently, a genomic approach showed that by analyzing DNA from tumor cells in the blood, patients with colon cancer could receive a tailored therapy, reducing the need for chemotherapy by almost 50% and thus preventing associated side effects.[14] More recently, omics such as metabolomics have been extensively explored in the context of diagnosis and disease monitoring.

Data generated from omics is a major origin of big data in healthcare and provides a large source of information that has thus far barely been used. Due to the complexity and amount of omics data, sophisticated analysis and computational power (such as quantum computing) are necessary. Incorporating technologies like AI and ML transforms the data into useful information. These technologies reduce costs and time of analysis and simplify identification of patterns and associations, which can improve medical decision making. For example, in a recent breakthrough, in silico quaternary protein structures and ligand-receptor interaction model are now being used to develop libraries of optimal drug structures for therapeutic interventions in individual tumors even before sequencing the causative cancer gene.

However, two main considerations currently hamper the widespread and in-depth use of omics data in real-life settings. First, the incorporation into clinical practice is slow because healthcare systems are still at the beginning of their digital transformation. Much more work is needed to provide healthcare professionals with the necessary infrastructure and technologies, and to develop the specific skills required to work with omics data.

Second, medical consensus is lacking on many aspects of information generated from omics data alone. As many diseases are also strongly influenced by environmental factors, the greatest benefits arise when omics data is integrated into a holistic diagnostic and treatment approach. The realization of its potential not only rests on changes to the health system but also the regulatory and legal frameworks of multiple countries that govern how personal medical data can be gathered and utilized. Privacy concerns must be balanced with the clear medical benefits to personal and communal health, and governments and regulators must provide guidance and clear guidelines under which the medical system can function.

A multi-omics strategy combined with other biomedical data such as patient history and clinical data could provide the greatest benefit within a holistic diagnostic and treatment approach.

Impacts

Omics have the potential to significantly change medicine and healthcare in the future, bringing wide-ranging impacts to healthcare and life sciences players (see Figure 3). Patients and care providers also benefit from omics through the growing personalization of medicine, improvement of treatment outcomes, and the reduction of inefficient and costly therapies. While the omics revolution is based on the generation of vast amounts of data, this data is still a component of an overall health ecosystem.

This ecosystem contains different players. Regulatory agencies provide the legal framework in which the entire system operates. Tech companies deploy the required tools to acquire and analyze data that can then be used by research institutes, universities, and pharmaceutical companies. Their target is to better understand diseases and develop new and more effective treatments. Finally, medical professionals provide care to individual patients. Within this ecosystem, demands on healthcare professionals and regulators are increasing with the need for additional knowledge and technological skills.

There is also an ethical responsibility for these professionals to provide patients with the best possible information while medical relevance and the impacts of many genomic findings remain under discussion. Professionals also need access to the technological resources and skill sets to work with and analyze omics data, which requires significant investments from health providers.

Innovators can utilize the enormous potential of omics data that opens new possibilities for the development of drugs, diagnostics, or technology. But they also have to account for the rising need to connect the digital and clinical space and to create solutions that allow cost-efficient and easy application of omics for other healthcare and life sciences players.

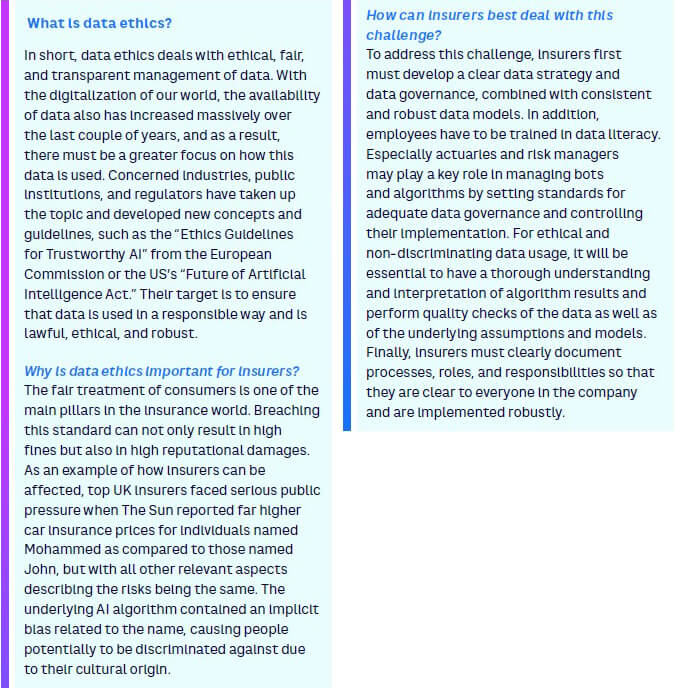

In this context, of particular importance is the need for ethical use of data and clear guidance from regulators and governments to codify the legal obligations of organizations that gather and use that data. Data policies regarding biometric information are exceptionally important in the insurance industry. It is well known that an information asymmetry, particularly for genetic information, between the applicant (with genetic information) and the insurer (without the genetic information) could lead to negative anti-selection. This could be the case if genetic risk assessments become more widespread and gain in predictive value. Then a larger number of applicants — and therefore a larger cumulative risk — could materialize in the insurance portfolio.

Additional information from other non-genetic omics could overcome this potential information asymmetry and provide superior risk prediction beyond or in addition to genetic testing, as legislation on non-genetic omics is not different from conventional laboratory parameters.

As an example, proteomics generated and analyzed from a blood sample can predict cardiopulmonary fitness or liver fat development to a high accuracy.[15] This non-genetic but highly sophisticated data could then be used instead of the current cumbersome medical examinations in underwriting, such as treadmill and stress tests, lung function tests, computer tomography, or echocardiograms to support risk-adequate loadings for applicants. Even in markets with broad access to genetic information for underwriting, non-genetic omics could improve risk detection and prediction, thus potentially omitting time-consuming in-person examinations, as described above. Other omics could then be complementary to or even replace genomics, depending on the predictive value and technical effort to yield the data.

Analysis of omics data could become a vital part of the underwriting process, but presumably only when high contract sums are assured, as the costs for specimen analysis and interpretation are currently high. As omics increasingly will be used in clinical routines as well, we expect significant price reductions soon, which will be favorable for cost-benefit evaluations of implementing omics into insurance risk processes.[16],[17]

Imperatives for healthcare & life sciences players

A key challenge for the healthcare and life sciences players centers on the question of how to integrate and utilize these insights and data into healthcare delivery to enable truly personalized medicine.

It is essential to create efficient operating models that underlie a personal health ecosystem comprised of primary care givers, data scientists, translational medicine researchers, and biopharmaceutical and medical device manufacturers. Continued monitoring of patients’ data will enable updates to their treatment regimens to deliver the most effective treatments but requires a full-scale omics view that accounts for changes in protein expression, mutations, and the transcriptome of the relevant component of a given pathway. Developing this system to effectively realize the full potential of omics and personalized medicine will require the following:

- Collect, structure, and analyze data. A vast amount of omics data is already available, and more is generated every day. To seize the opportunities lying within this data, healthcare and life sciences players must develop and implement strategies for accelerated data analysis.

- Build capabilities and data literacy. All components of the personal health ecosystem will require some degree of data knowledge, hardware and software systems capable of rapidly sharing data, sources of truth for education, trusted and secure data repositories, and clearly defined roles and responsibilities supported by health authorities for data use.

- Integrate data into development, manufacturing, and delivery. Data must be acquired from patients, transformed into actual treatments, and delivered to the patient. This requires care givers, data centers, and drug manufacturers to be operationally connected in a way that allows for rapid turnaround times, maintains the physical integrity of personalized medicine, and allows for repeated feedback loops of treatment development and improvement.

Imperatives for insurance

Omics will help in developing more precise diagnostics and enable personalized medical treatments. Its routine implementation in healthcare is expected within this decade. The transition in the insurance business could then follow shortly. In preparation, insurers should:

- Monitor health policy regulation in their markets to determine whether mass-data acquisition from biologic sources within an individual can be used for risk assessment.

- Use insurance medicine consultations to determine whether omics exist that have both accuracy and predictive value and are available, feasible, and cost-effective for implementation in the insurance application process.

- If omics are available, evaluate whether they can be harnessed not only in underwriting but also in the in-force insurance population to reduce cancer risk and thus potential claims.

4

MENTAL HEALTH

Insights & impacts

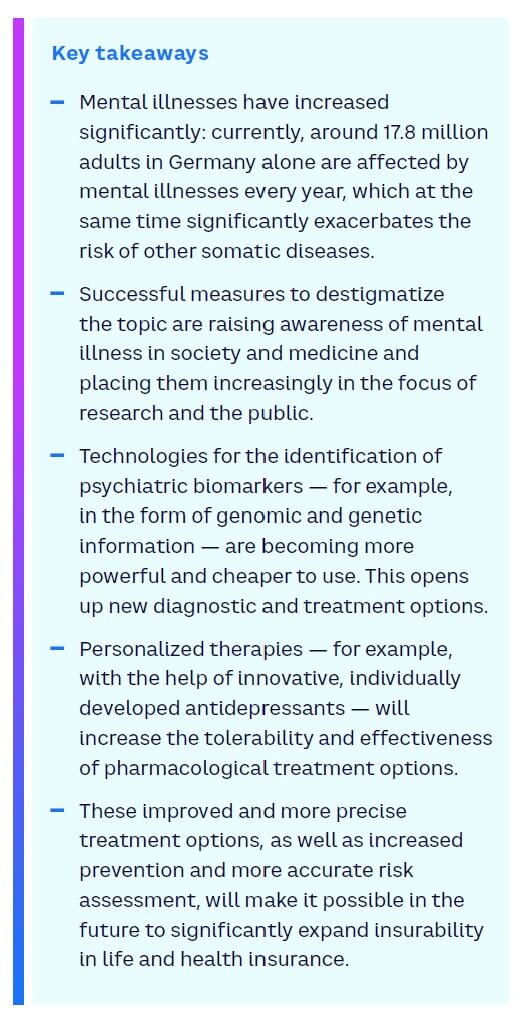

Mental health is a topic that concerns society as a whole and, more than ever, the insurance industry, medicine, pharmacology, and large parts of the healthcare system. Increasing case numbers and costs — as well as the associated extremely complex challenges in all the disciplines mentioned — are just a few of the many reasons for this development.

We discussed the current developments in mental health, the state of clinical research, and the resulting opportunities, especially for the insurance industry, with one of the world’s most renowned researchers in this field, Prof. Dr. Dr. Florian Holsboer, psychiatrist, chemist, and Emeritus Director of the Max Planck Institute for Psychiatry in Munich, and Dr. Alban Senn, Chief Medical Officer and Head of the Medical Research & Development team at Munich Re. In this chapter, we share a transcript from that interview.

Q: Professor Holsboer, the figures from insurers show that mental illnesses are increasingly the cause of occupational disability. Can you confirm this?

A: Prof. Dr. Dr. Florian Holsboer: The increase in documented cases of mental illness is a fact. However, we do not necessarily know whether more people have actually become mentally ill. The increase could as well be since our society today is a bit more open to mental illness diagnoses and that the individual is more likely to accept them.

In general, there are two uncertainties in the evaluation of the case numbers. First, we make psychiatric diagnoses solely based on interpretation of verbal communication. In other words, we depend on what patients and relatives tell us.

The second factor of uncertainty is stigmatization. The statement that someone is mentally ill still brings negative prejudices onto the scene. In order to not expose themselves to this, many people hesitate to make use of professional medical support. Treatment is delayed, and those affected are put on the path to incapacity for work, early retirement, or occupational disability.

Q: What consequences does this have with regard to the risk assessment of insurers?

A: Dr. Alban Senn: Our statistics show that mental illness is increasing as a cause of disability. This trend has been unbroken for 10 years, which is consistent with clinical observations. It is estimated that around 27.8% of the German adult population suffer from a mental illness at least temporarily every year. That amounts to 17.8 million people.

This raises two questions for us: How many of these people fall ill so severely that we cannot insure them and — more importantly — how do we identify those whose prognosis is so good that we can offer them insurance? That is the challenge we face.

Q: So, insurability thus evolves with medical progress. Which forms of therapy do you think are particularly promising?

A: Prof. Dr. Dr. Florian Holsboer: The antidepressants available today are too unspecific. The drugs work on too few patients, they take too long to work, and they have too many side effects. One explanation for this is the individual manifestation of mental illnesses. Two patients can be the same age, have the same sex, show identical symptoms, and get the same diagnosis — but in the background there may be very different disease mechanisms.

With the help of innovative antidepressants, we will be able to specifically address and cure this disease mechanism in the future. This is not utopia. Thanks to the successes in genome research, we should soon be able to offer laboratory tests that provide information on which patients a highly specific drug will be effective or not.

Q: Laboratory tests are surely an important future consideration. Another one is digital apps for prevention. How do you assess these? Could they be used to achieve measurable effects in insurance medicine?

A: Dr. Alban Senn: First of all, I welcome everything that supports and helps patients with their psychological challenges. It is easy to imagine that mental health apps can strengthen individual mindfulness and improve resilience to mental illness. If the digital apps also facilitate access to professional help, positive effects are quite possible. There are studies that suggest this. However, the abundance of app offerings is large, and the potential is not yet exhausted. At this point we, as the insurance industry, should become active; for example, by supporting customers and saying which of the digital offers are useful and effective. I am convinced that digital apps can develop valuable offerings, especially in the area of preventing mental diseases.

However, they will not be able to replace psychiatric pharmacotherapy, which means medication and conventional psychotherapy.

Q: How do you assess such digital tools from a scientific point of view? Could they lead to any measurable effects in insurance medicine?

A: Prof. Dr. Dr. Florian Holsboer: I share Alban’s assessment. Digital apps will never be able to replace the trusting relationship between a patient and his or her doctor, but they open new preventive opportunities.

Looking into the future, I see another, also technology-based, preventive option: biomarkers that can indicate the advent of a mental illness. This would give us the opportunity to intervene before the disease is even there.

Q: What are these biomarkers and how can they be identified?

A: Prof. Dr. Dr. Florian Holsboer: Biomarkers are genetic and genomic information, as well as certain biochemical and physiological data, from which we can derive valuable information on the individual risk of a person’s illness. In order to be able to collect and evaluate this information, medical research is developing innovative testing possibilities and better algorithms.

The keywords are “artificial intelligence” and “machine learning.” The progress in this field is currently enormous. This can be seen, for example, in genome sequencing: just a few years ago, the costs were tens of thousands of euros, and today it is a few hundred euros only.

This brings genome sequencing as a biomarker-based preventive examination close to practical applicability — at least in terms of costs.

Q: Could such screening also have positive effects for the insurance industry, for example, in underwriting?

A: Dr. Alban Senn: Yes, absolutely. The ability to predict individual risks and disease progression is part of the core of our work in risk assessment. The better and more objective the predictions, the easier it is to assess risks. In life insurance, however, we work with complex models, which ultimately result in mere probabilities.

These probabilities will probably never be 100% or 0%, but somewhere in between. Therefore, objective findings are essential building blocks for us. We know that even the best data cannot do justice to human complexity. This must be considered and therefore always have a comprehensive view on the applicant.

Q: Let’s look at the crystal ball: Will mental illnesses play an even greater role in 10 or 20 years? Or will current challenges be much better under control thanks to new forms of therapy and prevention?

A: Prof. Dr. Dr. Florian Holsboer: Successful measures against stigmatization and better treatments, especially through the introduction of personalized therapy, will increase patient confidence and social acceptance of the diseases.

The number of cases is therefore likely to increase further, but compensatory improvements will result in less progression to a chronic form and less early retirement at the same time. And what should not be forgotten is the following: patients who experience depression or become chronically depressed have a two to four times higher risk of dementia, cardiovascular disease, and diabetes. Successful psychiatric therapies will reduce these cases.

A: Dr. Alban Senn: I am also optimistic about the future and think that the life and health insurance business will benefit greatly from the outlined developments. In this respect, I hope that the destigmatization of mental diseases will lead to more early diagnoses, which can then be treated faster, more specifically, and ultimately more successfully than today. In this sense, I am looking forward to the upcoming developments.

Imperatives for healthcare & life sciences players

- Pharmacological research should focus on personalized therapeutic approaches. The mechanisms of mental illness are too individualized for non-specific drugs.

- Technology-based prevention options have great potential. Use it, for example, by developing new biomarkers or by offering even more effective mental health apps as a preventive measure.

- Focus on AI and ML in healthcare and especially for the further development of laboratory tests to support additional breakthroughs.

Imperatives for insurance

- Support measures to destigmatize mental illnesses. As a result, mental illnesses can be detected and treated at an earlier stage, so that incapacity for work, work occupational disability, and early retirement are more often avoided.

- Strengthen the resilience of insured persons and support them in individual prevention by promoting selected mental health apps with proven effectiveness and giving insured persons support in app selection.

- Benefit from medical progress and improved prevention by continuously expanding insurability.

5

PANDEMIC RISK

Insights

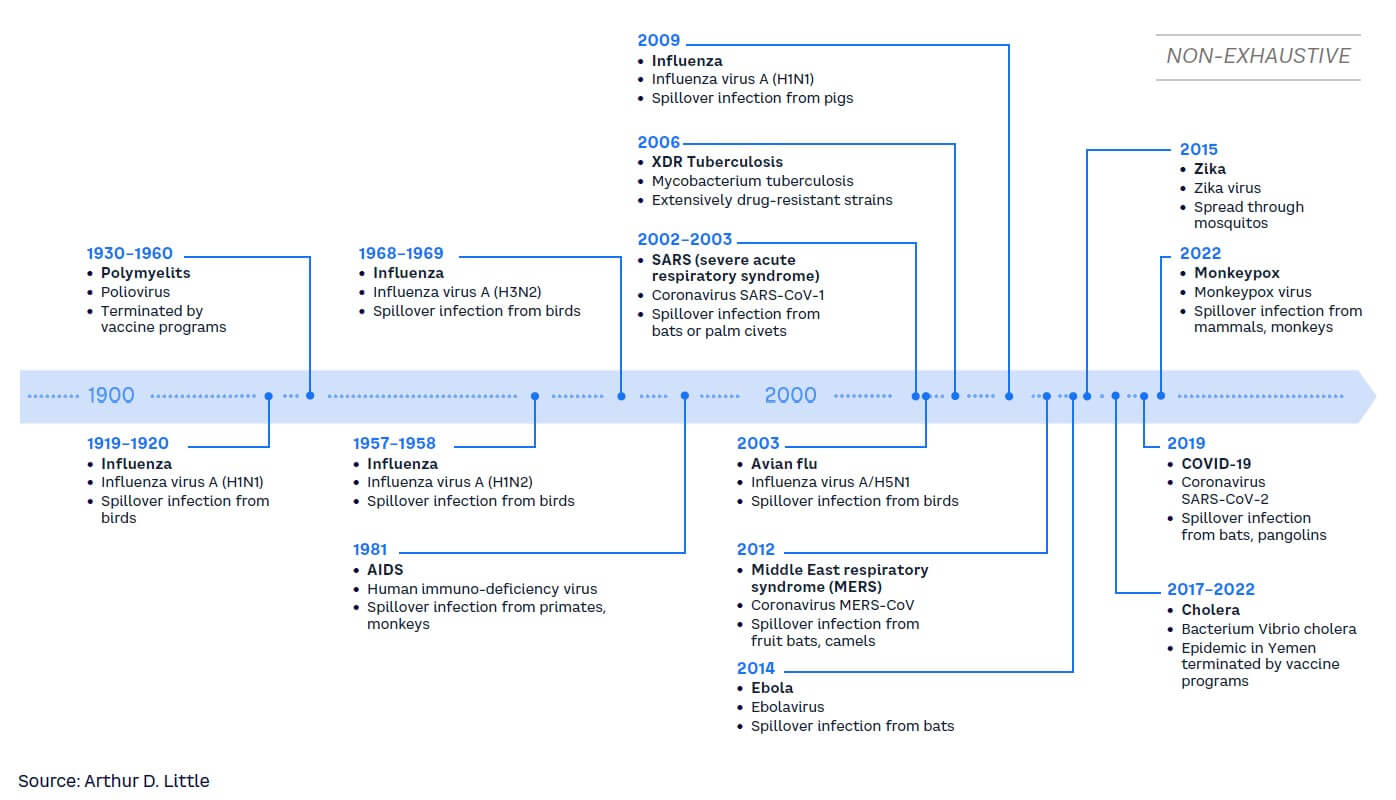

COVID-19, like many previous pandemics, clearly demonstrated how a pathogen can emerge from wild animal hosts and spill over into humans. The increasing proximity between wild animals and humans due to deforestation, change of land use, and urbanization, together with changes in the natural world driven by climate change and loss of biodiversity, are exposing humanity to novel pathogens, thereby raising the likelihood of the next pandemic.

A large pool of as yet uncharacterized viruses and bacteria is circulating in wild animals worldwide, with some of them having pathogenic potential to humans. Changes within the natural habitats of these animals increase the chance of spreading these viruses or bacteria widely across species, including humans. Once transmitted, a global spread of another highly contagious infectious disease like COVID-19 could be possible and, in fact, the current monkeypox outbreak illustrates this point. As of 22 August 2022, just over 40,000 cases have been reported globally, according to the US Centers for Disease Control and Prevention. Though a zoonotic infection most often seen in West and Central Africa, monkeypox is now a global health risk and is a harbinger of potential future health threats.

The highly complex relation between climate change and risk for infectious diseases is demonstrated by an outbreak of anthrax, a severe bacterial infection, in Siberia in 2016.[18] The disease was transmitted by bacterial spores from reindeer corpses that were released from permafrost due to rising temperatures.

Moreover, ice samples from China have been found to contain viruses that were ~15,000 years[19] old as well as more than 750,000-year-old bacteria.[20] These potential pathogens could theoretically give rise to the next global pandemic, as the Arctic and permafrost regions are warming at an unprecedented speed.

But climate change cannot only increase the probability of new or reemerging infectious diseases, already existing diseases also are highly impacted by increasing temperature. In fact, estimations show that 58% of all infectious diseases due to bacteria, virus, or other pathogens have been aggravated by climate hazards in the past.[21] Studies show that approximately 1.7 million viruses residing in mammals and birds are still uncharacterized. Of those, 50% are thought to have the potential to spread to humans. The number of already characterized viruses that are known to spill over to humans is only around ~250. However, as the rapid development and introduction of COVID-19 vaccines and antiviral drugs has shown, current medical technologies enable us to react quickly to emerging viruses.

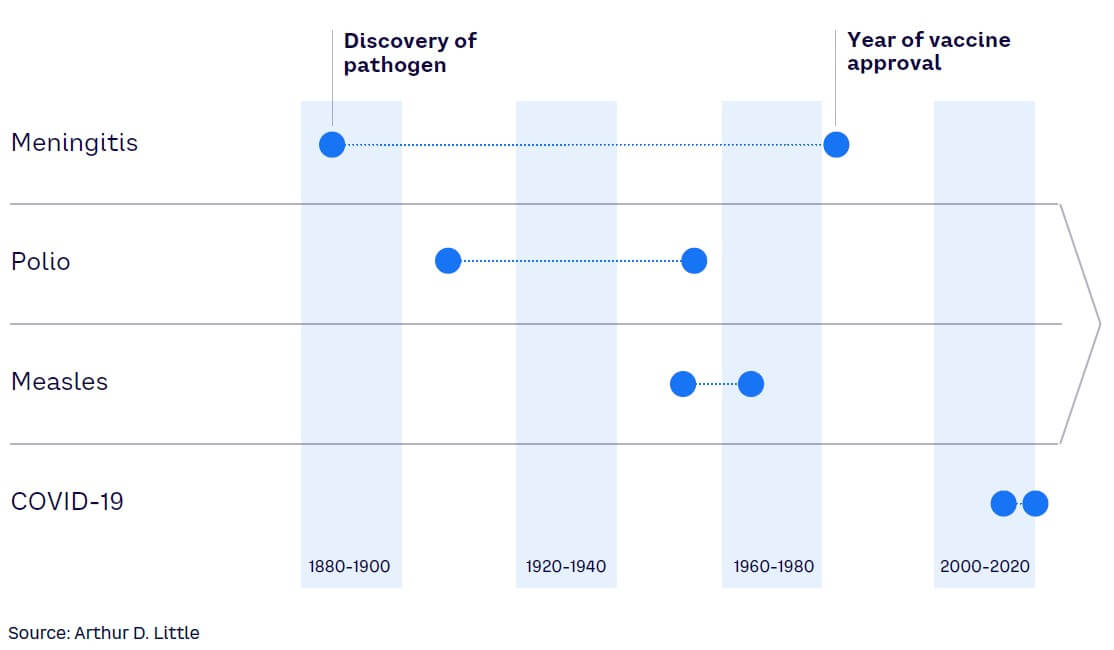

From the initial description of the SARS-CoV-2 virus to the approval of the first mRNA vaccine, it took less than 12 months, which is unprecedented in medical history (see Figure 4). By implementing additional effective public health measures, governments and healthcare systems are likely to improve their resilience for future COVID-19 outbreaks and other pandemics (albeit to varying levels). The incredible success of COVID-19 vaccine development stands as the demarcation point of a new era in which medical science has the tools and knowledge to rapidly analyze pathogens and develop multiple countermeasures against them.[22]

In the case of COVID-19, nucleic acid sequencing, lipid nano-particles, and mRNA design were the underlying technologies enabling vaccine development.[23] Going forward, advances in AI that enable modeling of quaternary protein structures, such as antigen/antibody binding, will further enhance vaccine and therapeutics development. These technologies can forecast likely mutation sites in viruses leading to new virus variants. Therefore, it will be possible to preemptively design vaccines for future virus variants or pathogens.[24]

However, beyond potential pandemic risks from viruses, a serious threat of growing antimicrobial (or antibiotic) resistance in healthcare systems is imminent. Antimicrobial resistance causes longer hospital stays, more complications, and higher treatment costs (estimated at an additional $1,400 for each patient with infection),[25] which all contribute to rising costs for healthcare systems and insurance companies. The long-term health effects of surviving an infection with antibiotic-resistant bacteria is less understood but could confer a long-term mortality risk.[26] In the European Union alone, approximately 27,249 deaths (age-standardized) were attributed to antibiotic-resistant bacterial infections in 2015, increasing from 11,144 in 2007.[27]

Developing antimicrobial resistance is a natural evolutionary mechanism, especially in pathogens like bacteria. Antimicrobial agents (or antibiotics) have been in use for almost 100 years and are the main pillar for treatment of serious bacterial infections. As a reaction to exposure with antimicrobial agents, bacteria can adapt and develop strategies that enable them to resist. Antimicrobial resistance is not a new or surprising concept, as already in the 1930s, shortly after the first clinical use of an antibiotic, resistant bacteria were reported.

But today, antimicrobial resistance is a growing problem for healthcare systems worldwide due to variety of factors.

First among these factors is the fact that discovery of novel antibiotics has declined rapidly since the 1960s. In fact, over the last 20 years, just one novel class of antibiotics has been introduced. Second, antibiotic prescriptions have steadily increased until recently, raising the likelihood of antimicrobial resistance due to evolutionary pressure. Also so-called reserve antibiotics, which comprise last-resort antibiotics for targeted use in multidrug-resistant infections, have been increasingly used. These factors can lead to futility in treating severe infections with multi-resistant bacteria, increasing mortality from otherwise well-treatable diseases.

A recent study estimated that approximately 1.3 million people died globally in 2019 due to infections with multi-resistant bacteria.[28] This makes antibiotic-resistant infections one of the major causes of death worldwide, prospectively overtaking malaria and HIV as leading infectious diseases in the future.

Although resistance to major antibiotics is increasing on a global scale, there are astonishing regional differences. For example, the average resistance proportions in Italy or Greece (about 35%) is much higher than in Germany or the UK (about 10%). Notably, some countries, such as the Netherlands or Nordic countries in Europe, have pushed down resistance proportions to about 5%.[29]

Countries that decreased resistance have reduced antibiotic prescriptions, implemented rigorous surveillance system for multi-resistant bacteria, and enacted hygiene regimens and so-called antibiotic stewardship programs that foster the rationale use of antibiotics. The combination of these measures is believed to result in these impressively low levels of antibiotic resistance.

But even these countries are at risk of importing multi-resistant bacteria from different regions or spread from livestock. Resistance to commonly used antibiotics in bacteria from food-producing animals remains high, reaching up to 90% for several antibiotics in animals in some EU countries. To address antimicrobial resistance as a major public health problem, the EU Commission has implemented a so-called “One Health” policy response, which improves surveillance and cooperation between member states.[30] These efforts have led to a reduction of antibiotic use in food-producing animals by 43% between 2011 and 2020.

The COVID-19 pandemic could have a major impact on antibiotic resistance of bacteria. Many COVID-19 patients suffered from secondary pulmonary bacterial infection, which is often treated with antibiotics, sometimes even preventively. Although in both the US and EU, overall antibiotic use dropped, certain bacteria in both geographies showed increasing resistance against critically important antibiotics. Moreover, both the US and EU member states have acknowledged reporting gaps or delays in implementing action plans for antibiotic resistance during the pandemic.[31]

Therefore, the long-term impact of the COVID-19 pandemic on antimicrobial resistance needs further investigation but could indeed have exacerbated the situation for treating specific severe infections with several reserve antibiotics.

Impacts

Entering this century, a wave of severe infectious disease outbreaks such as SARS, MERS, and COVID-19 has occurred (see Figure 5). Our global lifestyle and present challenges, such as climate change, enhance the probability of another pandemic like COVID-19 coming sooner rather than later. Some risk models predict the probability of another pandemic of the same or greater magnitude as COVID-19 to be approximately 25% within the next 10 years or 3% within any given year.[32] This would have a large impact on healthcare systems globally.

As a result, governments and policy makers are under pressure to establish strong governmental/regulatory entities and an improved system of surveillance, detection, and alerts to be able to face the risks of upcoming pandemics.[33] There is an increasing need for governance strategies that encompass measures of prevention and create an environment of preparedness and resilience toward pandemics and/or the threat of new and more virulent infectious diseases.[34] Governance policy — and also insurance industry — should strengthen communication of healthcare measures and scientific progress to improve public understanding and prevent a sinister combination of misinformation and disinformation that would undermine the fight against the pandemic.[35]

Similarly, life sciences players must implement strategies that define the necessary processes, responsibilities, and guidelines to prepare for the next pandemic. These strategies must enable a rapid shift of resources and manufacturing capacities toward the development of diagnostics, medical technology equipment and consumables, and therapeutics. They should improve the understanding and resilience in the global supply chains.

Healthcare providers once again will be at the front line when the next pandemic comes our way, and we need to prepare now. Providers must review the pressure and backlog still present from the last pandemic to establish guidelines for ensuring adequate resources (including people and supplies) for future challenges while not overburdening the system. They also need strategies for prevention and should implement an adequate level of preparedness and resilience. This includes the right processes and measures to ensure to address a pandemic, but also to continue to deliver urgent and chronic care, which otherwise could suffer.[36] Supply chain and digital and remote tools will also be equally important.

For insurers, a pandemic can lead to significant losses in the life and health sectors. In fact, the Association of British Insurers reported that COVID-19-related payouts for life insurance claims were £202 million in 2020, rising to £261 million in 2021.[37] Beyond mortality risks, the impact on disability insurance claims due to Long COVID (or post-COVID-19 condition), has been a concern for the industry as well. Long COVID develops more likely following an initially severe infection, which is fortunately the minority of cases. Severely debilitating Long COVID is therefore a relatively rare event.

Notably, the risk for developing Long COVID, can be substantially reduced with COVID-19 vaccines.[38] As such, from a medical perspective we currently only expect a minimal increase by 0.5% in annual total disability claims due to Long COVID compared to pre-pandemic levels for the German private sector, although this minor increase may be due to lower average morbidity and greater vaccination rates among the insured and does not include the whole working population. Other markets might experience a different impact of Long COVID or COVID-19-related mortality, driven by different insurance policies, vaccination rates, and healthcare service to those who are affected.[39]

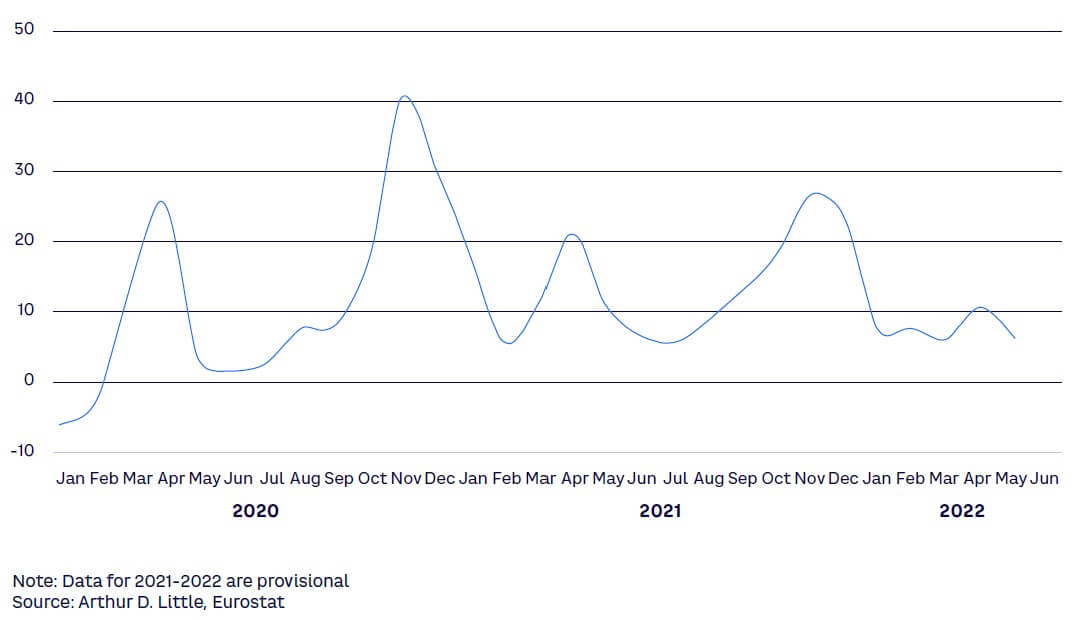

This monthly excess mortality indicator shown in Figure 6 compares the number of people who died of any cause in a given month with a baseline average taken during the pre-pandemic period 2016-2019. The peaks have varied greatly across EU states during the pandemic.

Imperatives for healthcare & life sciences players

The continued impacts of the COVID-19 pandemic emphasize the need for strategies that create a sufficient level of preparedness and resilience for the next pandemic. This must be addressed from all angles in healthcare and life sciences and health policy in the following areas:

- Prevent. Investing in further research and analysis of data generated during the COVID-19 pandemic will strongly enhance the ability to prevent new pandemics. Understanding spread and spill-over effects of pathogens is imperative in developing countermeasures to prevent the emergence of new pandemics. In addition, it will be important to continue to invest in both antibiotic development as well as in measures to curb the development of multi-resistant bacteria strains globally.

- Prepare. Preparation is a key factor in facing the threat of the next pandemic. Healthcare and life sciences players must analyze the lessons learned from COVID-19 to develop a state of preparedness. Going forward, data and data definitions (e.g., what is death due to COVID-19?) would benefit from a consistent approach over time and across territories, wherever possible. Of particular importance is the development of communication plans to instill trust in medical authorities and public pandemic countermeasures.

Local governments must take an active role in planning for future outbreaks by providing consistent funding for both basic and translational scientific research, creating and maintaining medical countermeasure stockpiles, developing logistical planning for triage and treatments, and forging clear guidelines for communications during what is often a rapidly evolving yet long-duration emergency. Post-hoc analysis of the effectiveness of responses to the COVID-19 outbreak should be highly informative in developing future plans.

- Finance. The allocation of financial resources for prevention, preparation, and surveillance is imperative for all players, and it is of vital importance that is accomplished in such a way that these resources are independent of short-term budget resolutions. For example, innovators can allocate financial resources and create initiatives to promote research on upcoming and already-existing threats. Recently, Boehringer Ingelheim, Evotec, and bioMerieux announced in a joint venture that they will pour their resources into fighting antimicrobial resistance.

- Innovate. Healthcare and life sciences players must turn their focus toward investing in innovation. Some pathogens considered as the source for a new pandemic are already known, but innovations to diagnose or treat them remain lacking. And it is imperative that the focus includes bacteria as well as viruses and other pathogens. As an example, an initiative by UNICEF, together with large software and search engine companies, generates and analyzes real-time data that can be used in outbreaks and for preventive measures.

Imperatives for insurance

The threat of a next pandemic is no theoretic scenario for the life and health insurance industries. Their resilience will depend on certain precautions, including:

- Prepare. Existing pandemic preparedness and response plans must be reviewed frequently. In case of an emerging pandemic, insurers should install a monitoring process within their institution to detect early relevant impacts on mortality and disability business and to update underwriting guidelines according to the associated health risks and in consultation with insurance medicine experts.

- Consult. Chief medical officers (CMOs) and their insurance medicine teams have the expertise to analyze and interpret, very early in a pandemic, important clinical studies, such as for COVID-19. Their medical research and development can make an early impact assessment on mortality and morbidity possible.

- Identify. Infectious risk from non-pandemic pathogens, such as bacterial epidemics, can differ from market to market. With the help of the CMO, identify important differences in antibiotic resistance and public health countermeasures to enable a correct risk assessment for mortality and morbidity risks.

Notes

[1] “Projected Global Digital Health Market Size from 2019 to 2025.” Statista, accessed September 2022.

[2] “Digital Health in Immunology — Thematic Research.” GlobalData, 10 December 2021.

[3] “Digital Transformation and Emerging Technology in the Healthcare Industry — 2021 Edition.” GlobalData, 30 November 2021.

[4] Kernebeck, Sven, et al. “Adherence to Digital Health Interventions: Definitions, Methods, and Open Questions.” Bundesgesundheitsblatt, Vol. 64, 2021.

[5] Ebenfeld, Lara, et al. “Evaluating a Hybrid Web-Based Training Program for Panic Disorder and Agoraphobia: Randomized Controlled Trial.” Journal of Medical Internet Research, Vol. 23, No. 3, 2021.

[6] Buntrock, Claudia, et al. “Effect of a Web-Based Guided Self-Help Intervention for Prevention of Major Depression in Adults with Subthreshold Depression: A Randomized Clinical Trial.” JAMA, Vol. 315, No. 17, 2016.

[7] “Over $1bn Raised in Venture Capital Funding for Gene Editing in 2021.” GlobalData Healthcare, 27 January 2022.

[8] Wang, Xi, et al. “Targeting Monoamine Oxidase A for T Cell–Based Cancer Immunotherapy.” Science Immunology, Vol. 6, 2021.

[9] Nogrady, Bianca. “Game-Changing Class of Immunotherapy Drugs Lengthen Melanoma Survival Rates.” Nature Index Cancer 2020, 22 April 2020.

[10] “Rare Genetic Diseases.” National Human Genome Research Institute, 2018.

[11] Mueller, Christine M., Gayatri R. Rao, and Katherine I. Miller Needleman. “Precision Medicines’ Impact on Orphan Drug Designation.” Clinical and Translation Science, Vol. 12, No. 6, 11 July 2019.

[12] German Federal Ministry of Health. “Annex XII — Benefit Assessment of Medicinal Products with New Active Substances According to § 35a SGB V: Ipilimumab.” Federal Gazette, Vol. B3, 23 August 2021.

[13] The term “omics” encompasses the scientific field of collecting, quantifying, and analyzing large pools of biologic molecules, from single cells to whole organisms such as the human body, in both normal health or with disease (e.g., cancer). Molecules can be DNA (genomics), all kinds of RNA (transcriptomics), proteins (proteomics), metabolites (metabolomics), lipids (lipidomics), and sugars (glycomics) as well as their interactions (interactomics).

[14] Tie, Jeanne, et al. “Circulating Tumor DNA Analysis Guiding Adjuvant Therapy in Stage II Colon Cancer.” New England Journal of Medicine, Vol. 386, 16 June 2022.

[15] Williams, Stephen A., et al. “Plasma Protein Patterns as Comprehensive Indicators of Health.” Nature Medicine, Vol. 25, 2 December 2019.

[16] Bennike, Tue Bjerg, et al. “A Cost-Effective High-Throughput Plasma and Serum Proteomics Workflow Enables Mapping of the Molecular Impact of Total Pancreatectomy with Islet Autotransplantation.” Journal of Proteome Research, Vol. 17, No. 5, 19 April 2018.

[17] Vowinckel, Jakob, et al. “Cost-Effective Generation of Precise Label-Free Quantitative Proteomes in High-Throughput by MicroLC and Data-Independent Acquisition.” Scientific Reports, Vol. 8, 12 March 2018.

[18] Stella, Elisa, et al. “Permafrost Dynamics and the Risk of Anthrax Transmission: A Modelling Study.” Scientific Reports, Vol. 10, No. 16460, 7 October 2020.

[19] Zhong, Zhi-Ping, et al. “Glacier Ice Archives Nearly 15,000-year-old Microbes and Phages.” Microbiome, Vol. 9, No. 160, 2021.

[20] Christner, Brent C., et al. “Bacterial Recovery from Ancient Glacial Ice.” Environmental Microbiology, Vol. 5, No. 5, 2003.

[21] Mora, Camilo, et al. “Over Half of Known Human Pathogenic Diseases Can Be Aggravated by Climate Change.” Nature Climate Change, Vol. 12, 2022.

[22] Ball, Philip. “The Lightning-Fast Quest for COVID Vaccines — And What It Means for Other Diseases.” Nature, 18 December 2020.

[23] Dolgin, Elie. “The Tangled History of mRNA Vaccines.” Nature, 14 September 2021.

[24] Schmidt, Fabian, et al. “High Genetic Barrier to SARS-CoV-2 Polyclonal Neutralizing Antibody Escape.” Nature, Vol. 600, 20 September 2021.

[25] Thorpe, Kenneth E., Peter Joski, and Kenton J. Johnston. “Antibiotic-Resistant Infection Treatment Costs Have Doubled Since 2002, Now Exceeding $2 Billion Annually.” Health Affairs, Vol. 37, No. 4, 21 March 2018.

[26] Drummond, Rebecca A., et al. “Long-Term Antibiotic Exposure Promotes Mortality After Systemic Fungal Infection by Driving Lymphocyte Dysfunction and Systemic Escape of Commensal Bacteria.” Cell Host & Microbe, Vol. 30, No. 7, 13 July 2020.

[27] Cassini, Alessandro, et al. “Attributable Deaths and Disability-Adjusted Life-Years Caused by Infections with Antibiotic-Resistant Bacteria in the EU and the European Economic Area in 2015: A Population-Level Modelling Analysis.” The Lancet Infectious Diseases, Vol. 19, No. 1, 5 November 2018.

[28] “Global Burden of Bacterial Antimicrobial Resistance in 2019: A Systematic Analysis.” The Lancet, Vol. 399, No. 10325, 19 January 2022.

[29] “Stemming the Superbug Tide: Just A Few Dollars More.” OECD Health Policy Studies, OECD Publishing, 7 November 2018.

[30] “Antimicrobial Resistance in the EU/EEA — A One Health Response.” OECD, 2022.

[31] “Antimicrobial Resistance in the EU/EEA — A One Health Response.” OECD, 2022.

[32] Cheney, Catherine. “How Might Probability Inform Policy on Pandemics? Metabiota Has Ideas.” Devex, 31 July 2021.

[33] Clark, Helen, et al. “Transforming or Tinkering: The World Remains Unprepared for the Next Pandemic Threat.” The Lancet, 18 May 2022.

[34] Moeti, Matshidiso, George F. Gao, and Helen Herrman. “Global Pandemic Perspectives: Public Health, Mental Health, and Lessons for the Future.” The Lancet, 4 August 2022.

[35] Goetz, Miriam, and Lena Christiaans. “Health Insurance Communication in the COVID-19 Pandemic: A Comparative Analysis of Crisis Communication on Websites.” Prävention und Gesundheitsförderung, Vol. 17, 7 May 2021.

[36] Kendzerska, Tetyana, et al. “The Effects of the Health System Response to the COVID-19 Pandemic on Chronic Disease Management: A Narrative Review.” Risk Management and Healthcare Policy, Vol. 14, 15 February 2021.

[37] “Record Amount Paid Out to Help Families Cope with Bereavement, Ill Health, and Injury.” The Association of British Insurers (ABI), 14 April 2021.

[38] Ayoubkhani, Daniel, et al. “Trajectory of Long COVID Symptoms After COVID-19 Vaccination: Community-Based Cohort Study.” BMJ, Vol. 377, 18 May 2022.

[39] Suchy, Christiane, et al. “Post COVID-19 Condition and Its Potential Impact on Disability — A Proposal for a Calculation Basis for the Disability Insurance Sector.” Zeitschrift für die gesamte Versicherungswissenschaft, Vol. 111, 19 July 2022.

DOWNLOAD THE FULL REPORT

DATE

FOREWORD

Dear reader,

We are living in an era of rapid scientific progress. It spans across multiple disciplines and is changing not only the medicines available to patients, but also entire healthcare systems, inclusive of researchers, clinicians, payers, providers, regulatory agencies, and untold numbers of patients.

The revolution occurring in healthcare is forcing stakeholders across the industry and all who benefit from healthcare to face a variety of questions: What are the societal implications of these changes? How do they protect health and improve the individual’s chance of cure? And how do they affect the business environment for companies in life and health insurance and the life sciences industry?

We believe that the magnitude and impact of these discoveries and the current changes across healthcare are so significant that they cannot be adequately captured by an isolated view. That is why Arthur D. Little and Munich Re have combined their knowledge, as well as analytical skills, and consolidated them into this joint Life Science Report.

Here we provide a compact and clearly structured overview of the major trends in medicine and healthcare. This Life Science Report provides insights, reveals impacts, and sets forth imperatives for both the insurance and life sciences industries. The common goal: to bring innovations to patients faster and to push the boundaries of insurability.

The Life Science Report highlights some highly relevant global trends and innovations that are already shaping the healthcare of tomorrow. We hope that sharing our experiences and insights in this Report will evoke your interest for further discussion. We invite you to reach out to share your view with us and to shape the future of health together.

— Dr. Ulrica Sehlstedt, Managing Partner, Global Practice Leader Healthcare & Life Sciences, Arthur D. Little

— Anke Idstein, Chief Executive Life & Health Munich, Continental Europe (w/o Iberia, Italy, Malta) and Israel, Munich Re

EXECUTIVE SUMMARY

Aging populations, changing urban and work environments, technical innovations in data processing and analysis, and current advances in diagnosing and treating diseases will not only dramatically transform healthcare but also our way of living. This will have impacts, both positive and negative, on the life sciences and insurance industries, as it is their purpose to provide solutions that prevent and mitigate current and future risks.

The COVID-19 pandemic has demonstrated how developments in multiple areas of medicine and society, as well as ways of living and working, can accelerate dramatically under pressure. As such, medical technologies, digitization of the healthcare system, and telehealth have made significant progress in the last two years. Home care solutions for elderly or chronic disease patients are on the rise, incorporating digital and medical technologies.

This fosters an ongoing decentralization of the patient journey that can provide a higher quality of care, potentially improving quality-of-life and patient-centered outcomes. Decentralization and a rise in home care solutions are necessary and likely beneficial for the aging patient population worldwide. By 2060, twice as many people in the EU will be 65 years or older as those younger than 15 years, and the proportion of very old people will triple. We are seeing these aforementioned changes now. But novel developments in the area of life sciences are on the horizon and will need to be analyzed, understood, and evaluated for their impact.

For this Report, our team has defined five focus topics that reflect the latest developments in the healthcare space that impact players in life sciences as well as in insurance.

Digital health is our starting point and the title of our first chapter. It illustrates tangibly how data and digital technologies will change the patient journey and open the opportunity space for innovative digital health solutions that insurance and healthcare players can learn from. The second chapter looks at new and advanced treatments like immunotherapies, gene therapy, and cell-based therapeutics, and is followed by a chapter about new ways to analyze large-scale biologic data including genomics, as it is a major research field for the development of diagnostics and therapeutics.

Another highly relevant healthcare area that has gained pace and therefore its deserved attention in recent years, especially during the pandemic, is mental health. In an expert interview, world-renowned depression expert Prof. Dr. Dr. Florian Holsboer and Dr. Alban Senn, Chief Medical Officer at Munich Re, discuss current challenges and future solutions in this field. And finally, we explore what is next after COVID-19, what is the threat of the next pandemic, and how life sciences players and insurers could and should prepare to support a more resilient healthcare ecosystem.

1

DIGITAL HEALTH

Insights