In the context of a challenging macro environment, the global aviation sector is facing unprecedented change due to advances in aircraft technology, disruptive business models and a new generation of digitally enabled passenger. In light of these “hyper-competitive” pressures, Arthur D. Little re-examines the global alliance model and considers the future of cooperative strategy in the aviation sector as the industry enters a new competitive era.

Introduction: The Era of Hyper-Competition

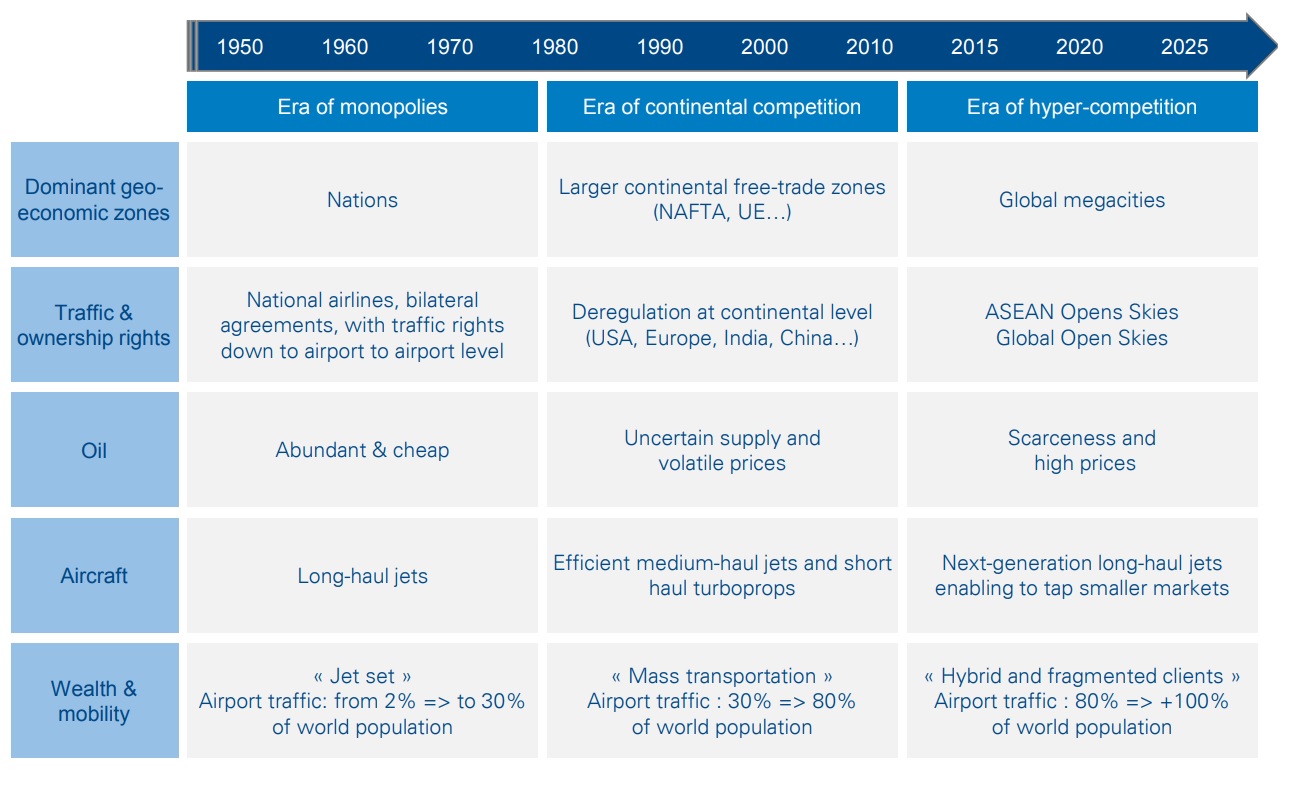

Formed over 15 years ago, at the outset of what Arthur D. Little has described as “the era of hyper-competition”, the global airline alliances have proven to be an enduring feature of the global aviation landscape. In a period characterized by growing competition for resources, airlines face multiple pressures, from high capital replacement costs and disruptive “low-cost” business models, to regulatory change, and the challenges and opportunities posed by rapidly evolving technology

Characteristics of Hyper-Competition

Faced with these pressures, from the late 1990s onwards the leading full-service airlines (FSAs) were quick to secure membership of one of the three mainstream global alliances – SkyTeam, Star Alliance and Oneworld – which in 2013 accounted for around 54% of total seats flown1 . The alliances promised many benefits, from enhanced connectivity, to cost savings and a smoother customer experience.

Yet although alliance membership has continued to expand, disruptive change has the potential to alter the pattern of incentives that determine cooperation between airlines. Some of the most prominent changes over the past 15 years include:

- Consolidation: although the European market remains fragmented, in North America, the industry has consolidated,which has increased the ability to manage capacity

- Technology: mobile and digital technology is reshaping the interfaces between passengers, airlines, airports and thirdpartyproviders, empowering the passenger and creating new opportunities for product and service innovation

- Traffic and Ownership Rights: from the EU-US OpenSkies agreement to changes in ETOPS legislation, regulatory change continues to facilitate ever-closer connectivity

- Oil: sustained fuel price volatility has dramatically reduced airline operating costs, albeit at the expense of capacity discipline in some markets

- Aircraft: the launch of next-generation, composite-based jets is transforming the market, especially in long-haul, enabling a new breed of “long-haul, low-cost” carrier

- Airports: enhanced hub infrastructure and innovative mobile technologies are transforming the airport experience, enabling more efficient transfer of passengers and bags

All of these changes bring profound implications for the global aviation industry, and it is in this context that we consider the implications for the global alliance model and assess the future outlook for cooperative strategy in the global aviation sector