13 min read

The role of hydrogen in building a sustainable future for automotive mobility

The pressing need to decarbonize mobility means automotive players are facing key choices around the fuels of the future. Taking a holistic approach, the authors explain why hydrogen is a strong candidate for powering automotive transformation and how a global green hydrogen ecosystem is likely to develop moving forward.

Transportation and mobility need to decarbonize and dramatically lower the sector’s emissions. This is necessary not just from a regulatory perspective, but also because only a truly sustainable transportation and automotive industry will be able to maintain its importance and prosperity in the long run.

Moving to a zero emissions future creates a once-in-a-century bet for the automotive, energy and transportation industries. The introduction of alternative powertrains and their related energy concepts is becoming a choice between battery electric vehicles (BEVs) and fuel cell electric vehicles (FCEVs) powered by hydrogen (H2). Although they are complementary in many ways, the enormous investments required in R&D, production and infrastructure for each of them, combined with the requirements of scale for success, will mean making the wrong bet can potentially endanger the future of established automotive companies. It is likely that investments will only pay out for one of the two approaches in specific applications if they achieve scale. Advantages in scaling will be very difficult to catch up with. The choice for replacing fossil fuel combustion engines splits the industry. The world’s largest manufacturers (VW by volume and Tesla by value), which are focusing solely on BEVs, stand against the second-largest, Toyota (plus Hyundai and some others), which has FCEVs as a core part of its The role of hydrogen in building a sustainable future for automotive mobility strategy. This divide is contentious – Elon Musk of Tesla has described hydrogen as “staggeringly dumb”. However, even a dual strategy (as pursued by the likes of BMW and Daimler) can lead to risk if it dilutes the focus, development speed and scale required for success.

At first glance, multiple factors seem to point to BEVs as the best option for a zero carbon world. They are more efficient than FCEVs, they are ahead in market penetration, and industry and infrastructure around green hydrogen are underdeveloped, which has led to supply constraints. Additionally, as green hydrogen has further vital uses for decarbonizing, some argue that limited supply should be focused on the applications with the highest immediate carbon reduction impact, for example replacing the current grey hydrogen used in industrial sectors such as chemicals, which cannot be easily transformed through electrification.

However, to gain a full perspective, a wider, more holistic approach needs to be taken, looking beyond these perceptions. In this article we argue that taking such an approach shows that hydrogen does indeed have a key role to play in building a sustainable future for the automotive sector, and we illustrate this with some example applications.

Taking a holistic view of the hydrogen economy

Three interlinked factors determine the desirability of supplying hydrogen for automotive applications: First, the global availability of a sufficient and competitive supply; second, the distribution of the available hydrogen supply between the automotive sector and other industry applications; and third, the achievable efficiency of hydrogen versus green electricity. Taking this holistic view enables players to make more informed decisions about their strategy.

1. A global hydrogen economy and ecosystem will emerge Although renewable electricity production in Europe is continuing to grow, there are limitations in its ability to meet the continent’s needs. In Northern Europe, for example, wind power is costly and available onshore space is limited. More generally, in many heavily industrialized regions with high demand, including Europe, Japan, and South Korea, renewable electricity generation is more costly than in other parts of the world. Although nuclear power remains an option, this is still expensive and a growing number of governments have, in any case, ruled it out as an energy source. Nearly all forecasts suggest that a significant part of the energy needs of these regions will need to be imported, which will drive the development of a global hydrogen economy. The greater yield potential of key locations for renewables, such as solar in Namibia, Chile, Australia and Saudi Arabia, will create investment and drive cost-competitiveness for green hydrogen generation. Japan has already signed agreements to import green hydrogen from Australia, for example. Similar projects on exporting hydrogen1 are evolving in Chile, Morocco, Oman, Brazil, Saudi Arabia, southern Europe2 and more.

This new industry opens up opportunities for players in the wider ecosystem, including, for example, generation, distribution, fueling stations, brokerage, and electrolyzers. We expect that this will lead to a sufficient supply of hydrogen globally from 2030 onwards.

2. It is advantageous to use hydrogen in the automotive as well as industrial sectors When comparing the various uses of hydrogen in a decarbonizing economy, two applications stand out due to their current activities and expected demand. First, the existing chemical industry, which currently uses grey hydrogen (generated from fossil fuels) as feedstock and, second, automotive mobility. Today, with not even 5 percent of current hydrogen produced from green, renewable sources, there is insufficient supply to cover both. Given that BEVs are an available option for automotive mobility, and that their downstream consumption efficiency is higher than that of FCEVs, some therefore argue that green hydrogen use should therefore focus on where it can deliver the greatest overall carbon reduction benefit, such as replacing grey hydrogen in industry. However, this argument misses some key points. Firstly, as we have explained above, we expect that rapidly growing demand will drive a global green hydrogen supply economy that will be sufficient to meet both industrial and automotive needs over the long term, towards 2030 and beyond. Secondly, we expect that pricing levels for green hydrogen will be such that application in the automotive sector will still be relatively attractive versus other industries. Even with increasing CO2 prices and tightening regulation, green hydrogen prices will be substantially higher than taxed grey hydrogen, naturally slowing its adoption. At the same time, automotive emissions regulations are likely to remain stricter than those of heavy industry, driving the use of green energy for automotive applications at even higher cost. Ultimately, many forecasters, such as the German Energy Agency, predict that our global ambition of net zero impact by 2050 will only be met with hydrogen application in multiple sectors, including automotive as well as heavy industry.

3. The real energy efficiency of hydrogen can be much higher than is commonly assumed The majority of studies that compare FCEV and BEV use show clear efficiency gains for battery electric – achieving approximately 75 percent efficiency compared to roughly 25 percent for fuel cells, for example, as shown by Transport & Environment and Traton. However, these studies are based on the presumption that sufficient locally generated renewable energy will always be available to meet demand. As we have mentioned above, in practice this cannot be guaranteed in many high-demand regions, such as Europe.

To understand efficiency better, a broader approach needs to be taken that considers energy production efficiency (upstream), which is specific to each country/region as energy is generated differently, as well as energy consumption efficiency (downstream), which is specific to each application and depends, for example, on powertrain efficiency. This downstream consumption component has been the focus up to now, with, for example, with the “tank-to-wheel” efficiencies that are embodied in current automotive regulations. Essentially, when fossil fuel energy resources are burned, they are lost; hence, it is vital to maximize their consumption efficiency.

In the renewable world a different approach is needed. The sun comes up every day, and the wind continues to blow. They are not used up in the same way as a barrel of oil. This means it is better to define efficiency in relation to the upstream generation resource as well as the downstream consumption component. For example, solar panels or wind power plants have different yields depending on their location: a solar panel in Germany generates 1,000 kWh/kWp p.a., while the same panel generates over 2,000 kWh/kWp in sunny locations such as northern Africa. When comparing these alternatives, electricity in Germany would start off with only 50 percent efficiency. Here, we are using a “panel-to-wheel” definition of efficiency.

Moreover, if surplus renewable power is available but cannot be used or stored, then generating green hydrogen is still the best approach for this surplus. In such a situation generating hydrogen from renewable electricity may be seen as highly efficient.

Furthermore, the efficiency of electricity compared to hydrogen for automotive applications varies dramatically depending on how green energy is produced. (See Figure 1.)

Locally generated green electricity delivers 95 percent efficiency, compared to 55 percent efficiency when using this source to create green hydrogen. However, as green electricity cannot always be generated locally at the time and on the scale needed, some energy generation will be required from remote locations (such as solar parks in the Middle East). In this case, since the produced electrical energy needs to be converted to hydrogen for long-distance transport and back to electricity for local consumption, the efficiency of electrical power drops to 25 percent, around half of the efficiency of hydrogen.

Challenging the assumption that green electricity is limitlessly available in the exact amounts, when and where needed, has an enormous impact on the applicability of BEVs and decreases their efficiency and green credentials. Green electricity production in Europe will not be enough to completely electrify the automotive sector, and even if this happened, the grid would not be able to cope with the transformation. It is also likely to have an impact on pricing, particularly around fast vehicle charging, which will significantly affect the operating costs of BEVs, such as in the heavy-duty/truck sector.

Hydrogen application in automotive mobility

This holistic approach to understanding the hydrogen economy leads us to the conclusion that hydrogen does have a key role to play in the zero carbon automotive sector of the future: there will be sufficient supply, pricing levels should not be prohibitive, and in many situations the real “source-to-wheel” efficiencies will be attractive versus BEVs.

Moving on to look at which automotive applications are likely to be the most attractive for hydrogen-powered fuel cells, heavy-duty trucks is the most obvious application for initial deployment. The large scale of the truck market is such that it can also act as enabler to other applications such as cars; hence, this will be decisive for the sector as a whole.

Assuming for now that both technologies, BEV and FCEV, will achieve technological requirements4, such as lifetime, range, handling of cold weather, vibration and refueling/recharging times, and further assuming that there will be an equal degree of regulation for both, four deciding factors remain:

1. Infrastructure: If needed, both BEV and FCEV infrastructure can and will be built up, but charging and refueling need to fit well to operational processes. Rapid charging of the large batteries needed for trucks is an even bigger challenge than high-performance charging for cars in terms of the infrastructure, parking space and time required. Every minute that a commercial vehicle is off road, it is losing money, which makes minimizing charging time vital.

2. Energy prices: With the decarbonization of electricity generation, electricity costs will be likely to increase substantially, potentially turning the current operatingcost advantage of BEVs into a disadvantage.

3. Autonomous driving: With autonomous driving, which is expected to arrive in this decade for trucks, charging times can no longer double up as mandatory driver breaks. This makes the long-range advantage of FCEVs even more significant.

4. Payload: A decrease in payload would negatively impact the business case. For high-energy demands and long-range requirements, batteries would weigh substantially more than the powertrain of FCEVs.

Strategic options for heavy-duty truck manufacturers

Coming back to the opposing positions in the automotive industry and looking at heavy-duty trucks in particular, manufacturers can take one of three strategic directions, each of which has its risks and relies on particular developments and scenarios taking place.

1. BEV-focused strategy Successful adoption would rely on a combination of low electricity prices, a smooth charging process and substantial, transformative improvements in battery performance. The major risk to this strategy is the impact of autonomous driving on commercial range

2. FCEV-focused strategy This relies on the fast emergence of a hydrogen economy with competitive prices and infrastructure in place. On the technology side, it requires advances in areas such as the durability of fuel cells above current development projections.

3. Dual with both BEVs and FCEVs This is based on the belief that FCEVs and BEVs are both needed for different use cases within heavy-duty trucks, or else are adopted as a strategy to mitigate the risk of choosing one technology above the other. The main risk of this strategy is that the split focus means that insufficient resources are devoted to each, so that the scaling of FCEV (and BEV) technology cannot be achieved within necessary time frames.

Based on our analysis outlined above, which concludes that a strong hydrogen economy will be created with competitive prices independent of the automotive industry, and BEVs will be impacted by relatively high charging prices due to increasing generation costs, high infrastructure investments, and competitive market dynamics, we have determined that:

- By 2030 FCEV trucks will have a lower total cost of ownership (TCO), costing around 1.5 euro cents per km and ton, compared to 1.7 euro cents for a BEV equivalent.

- These costs are likely to fall further post-2030 as the global hydrogen economy accelerates.

Of course, there are still many other things that need to be factored in, for example, potential changes in technology such as advances in battery technology, changes in regulation that impact the current equivalence of FCEV and BEV technology, and any decisions made on the use of nuclear that could impact the local generation and wider use of hydrogen. Furthermore, manufacturer strategies will also need to reflect the current product portfolio, regions targeted and capabilities.

Insights for the executive

Based on this broader perspective it becomes clear that commonly cited concerns around efficiency, prioritization or green hydrogen supply are not barriers to the use of green hydrogen in vehicles.

Efficiency is no argument against hydrogen

The industry needs to take a holistic view of decarbonization. Traditional efficiency measures will be different in a net zero world – inefficiencies in the use of green energy produced in the desert may yet turn out to be acceptable because of its stable, year-round supply. “Source-to-wheel” needs to be the metric to follow. Given that many nations will rely on imported green hydrogen, the only question is whether to convert it to electric power locally in the vehicle, or centrally, and then transfer it to charge large batteries.

A new global hydrogen ecosystem will be created

Hydrogen is a third major pillar in decarbonization, along with energy efficiency and electrification, and can be used in industry and power generation, as well as mobility. For many industrial (feedstock) applications, green hydrogen is the only decarbonization option available if countries are to meet the 95 percent reduction target.

The current view, which states that in regions such as Europe green hydrogen will be produced from renewables, will change as economies switch to green hydrogen generated elsewhere. Although optimal, cost-competitive supply locations are scarce (requiring political stability, wind, sun, space and water), there will not be the same level of dependency as in oil and gas. This is because renewables can be produced in more locations – less optimal sites will simply cost more, adding to the need for fast investment decisions.

Players need to take a holistic view

Given the diametrically opposed moves of the two biggest car builders, the unpredictable nature of regulation and the dependency on scenarios involving technology advancements (such as batteries) and energy supply strategies, players may struggle to place their bets wisely. To manage this well, they need to build a holistic understanding of the situation, with focus on energy supply, regulation and technology, creating a strategic foundation for these make-or-break decisions. The optimal choice will be application-specific – essentially, hydrogen is more advisable the larger the energy demand. A BEV-only strategy based on the perceived inefficiency and unavailability of green hydrogen should be reconsidered, especially for heavy-duty applications. Dual fuel strategies must assure sufficient scaling through partnering.

Define your path now

As decarbonization is a must, every player in the sector, whether a regulator, investor or provider in the field of mobility, needs to define its specific vision and strategy for transformation. A thorough cross-sectoral understanding is needed, for example, to be able to predict future regulations. Scenarios involving energy supply, regulation and technology need to be defined. A basic strategic point of view needs to be developed, covering how much to follow certain trends or whether to rely on a pure holistic sustainability position (akin to a value investor such as Warren Buffett), as well as preferences around risk and gain. The new ecosystem will offer a range of opportunities. Players (whether automotive, chemical or energy) need to position themselves now in the ecosystem, if necessary moving into related fields (e.g., electrolyzers, distribution). The hydrogen race has begun, with a global green hydrogen industry becoming mature post 2030. Organizations therefore need to invest now to secure leading positions in the ecosystem as it emerges.

13 min read

The role of hydrogen in building a sustainable future for automotive mobility

The pressing need to decarbonize mobility means automotive players are facing key choices around the fuels of the future. Taking a holistic approach, the authors explain why hydrogen is a strong candidate for powering automotive transformation and how a global green hydrogen ecosystem is likely to develop moving forward.

DATE

Transportation and mobility need to decarbonize and dramatically lower the sector’s emissions. This is necessary not just from a regulatory perspective, but also because only a truly sustainable transportation and automotive industry will be able to maintain its importance and prosperity in the long run.

Moving to a zero emissions future creates a once-in-a-century bet for the automotive, energy and transportation industries. The introduction of alternative powertrains and their related energy concepts is becoming a choice between battery electric vehicles (BEVs) and fuel cell electric vehicles (FCEVs) powered by hydrogen (H2). Although they are complementary in many ways, the enormous investments required in R&D, production and infrastructure for each of them, combined with the requirements of scale for success, will mean making the wrong bet can potentially endanger the future of established automotive companies. It is likely that investments will only pay out for one of the two approaches in specific applications if they achieve scale. Advantages in scaling will be very difficult to catch up with. The choice for replacing fossil fuel combustion engines splits the industry. The world’s largest manufacturers (VW by volume and Tesla by value), which are focusing solely on BEVs, stand against the second-largest, Toyota (plus Hyundai and some others), which has FCEVs as a core part of its The role of hydrogen in building a sustainable future for automotive mobility strategy. This divide is contentious – Elon Musk of Tesla has described hydrogen as “staggeringly dumb”. However, even a dual strategy (as pursued by the likes of BMW and Daimler) can lead to risk if it dilutes the focus, development speed and scale required for success.

At first glance, multiple factors seem to point to BEVs as the best option for a zero carbon world. They are more efficient than FCEVs, they are ahead in market penetration, and industry and infrastructure around green hydrogen are underdeveloped, which has led to supply constraints. Additionally, as green hydrogen has further vital uses for decarbonizing, some argue that limited supply should be focused on the applications with the highest immediate carbon reduction impact, for example replacing the current grey hydrogen used in industrial sectors such as chemicals, which cannot be easily transformed through electrification.

However, to gain a full perspective, a wider, more holistic approach needs to be taken, looking beyond these perceptions. In this article we argue that taking such an approach shows that hydrogen does indeed have a key role to play in building a sustainable future for the automotive sector, and we illustrate this with some example applications.

Taking a holistic view of the hydrogen economy

Three interlinked factors determine the desirability of supplying hydrogen for automotive applications: First, the global availability of a sufficient and competitive supply; second, the distribution of the available hydrogen supply between the automotive sector and other industry applications; and third, the achievable efficiency of hydrogen versus green electricity. Taking this holistic view enables players to make more informed decisions about their strategy.

1. A global hydrogen economy and ecosystem will emerge Although renewable electricity production in Europe is continuing to grow, there are limitations in its ability to meet the continent’s needs. In Northern Europe, for example, wind power is costly and available onshore space is limited. More generally, in many heavily industrialized regions with high demand, including Europe, Japan, and South Korea, renewable electricity generation is more costly than in other parts of the world. Although nuclear power remains an option, this is still expensive and a growing number of governments have, in any case, ruled it out as an energy source. Nearly all forecasts suggest that a significant part of the energy needs of these regions will need to be imported, which will drive the development of a global hydrogen economy. The greater yield potential of key locations for renewables, such as solar in Namibia, Chile, Australia and Saudi Arabia, will create investment and drive cost-competitiveness for green hydrogen generation. Japan has already signed agreements to import green hydrogen from Australia, for example. Similar projects on exporting hydrogen1 are evolving in Chile, Morocco, Oman, Brazil, Saudi Arabia, southern Europe2 and more.

This new industry opens up opportunities for players in the wider ecosystem, including, for example, generation, distribution, fueling stations, brokerage, and electrolyzers. We expect that this will lead to a sufficient supply of hydrogen globally from 2030 onwards.

2. It is advantageous to use hydrogen in the automotive as well as industrial sectors When comparing the various uses of hydrogen in a decarbonizing economy, two applications stand out due to their current activities and expected demand. First, the existing chemical industry, which currently uses grey hydrogen (generated from fossil fuels) as feedstock and, second, automotive mobility. Today, with not even 5 percent of current hydrogen produced from green, renewable sources, there is insufficient supply to cover both. Given that BEVs are an available option for automotive mobility, and that their downstream consumption efficiency is higher than that of FCEVs, some therefore argue that green hydrogen use should therefore focus on where it can deliver the greatest overall carbon reduction benefit, such as replacing grey hydrogen in industry. However, this argument misses some key points. Firstly, as we have explained above, we expect that rapidly growing demand will drive a global green hydrogen supply economy that will be sufficient to meet both industrial and automotive needs over the long term, towards 2030 and beyond. Secondly, we expect that pricing levels for green hydrogen will be such that application in the automotive sector will still be relatively attractive versus other industries. Even with increasing CO2 prices and tightening regulation, green hydrogen prices will be substantially higher than taxed grey hydrogen, naturally slowing its adoption. At the same time, automotive emissions regulations are likely to remain stricter than those of heavy industry, driving the use of green energy for automotive applications at even higher cost. Ultimately, many forecasters, such as the German Energy Agency, predict that our global ambition of net zero impact by 2050 will only be met with hydrogen application in multiple sectors, including automotive as well as heavy industry.

3. The real energy efficiency of hydrogen can be much higher than is commonly assumed The majority of studies that compare FCEV and BEV use show clear efficiency gains for battery electric – achieving approximately 75 percent efficiency compared to roughly 25 percent for fuel cells, for example, as shown by Transport & Environment and Traton. However, these studies are based on the presumption that sufficient locally generated renewable energy will always be available to meet demand. As we have mentioned above, in practice this cannot be guaranteed in many high-demand regions, such as Europe.

To understand efficiency better, a broader approach needs to be taken that considers energy production efficiency (upstream), which is specific to each country/region as energy is generated differently, as well as energy consumption efficiency (downstream), which is specific to each application and depends, for example, on powertrain efficiency. This downstream consumption component has been the focus up to now, with, for example, with the “tank-to-wheel” efficiencies that are embodied in current automotive regulations. Essentially, when fossil fuel energy resources are burned, they are lost; hence, it is vital to maximize their consumption efficiency.

In the renewable world a different approach is needed. The sun comes up every day, and the wind continues to blow. They are not used up in the same way as a barrel of oil. This means it is better to define efficiency in relation to the upstream generation resource as well as the downstream consumption component. For example, solar panels or wind power plants have different yields depending on their location: a solar panel in Germany generates 1,000 kWh/kWp p.a., while the same panel generates over 2,000 kWh/kWp in sunny locations such as northern Africa. When comparing these alternatives, electricity in Germany would start off with only 50 percent efficiency. Here, we are using a “panel-to-wheel” definition of efficiency.

Moreover, if surplus renewable power is available but cannot be used or stored, then generating green hydrogen is still the best approach for this surplus. In such a situation generating hydrogen from renewable electricity may be seen as highly efficient.

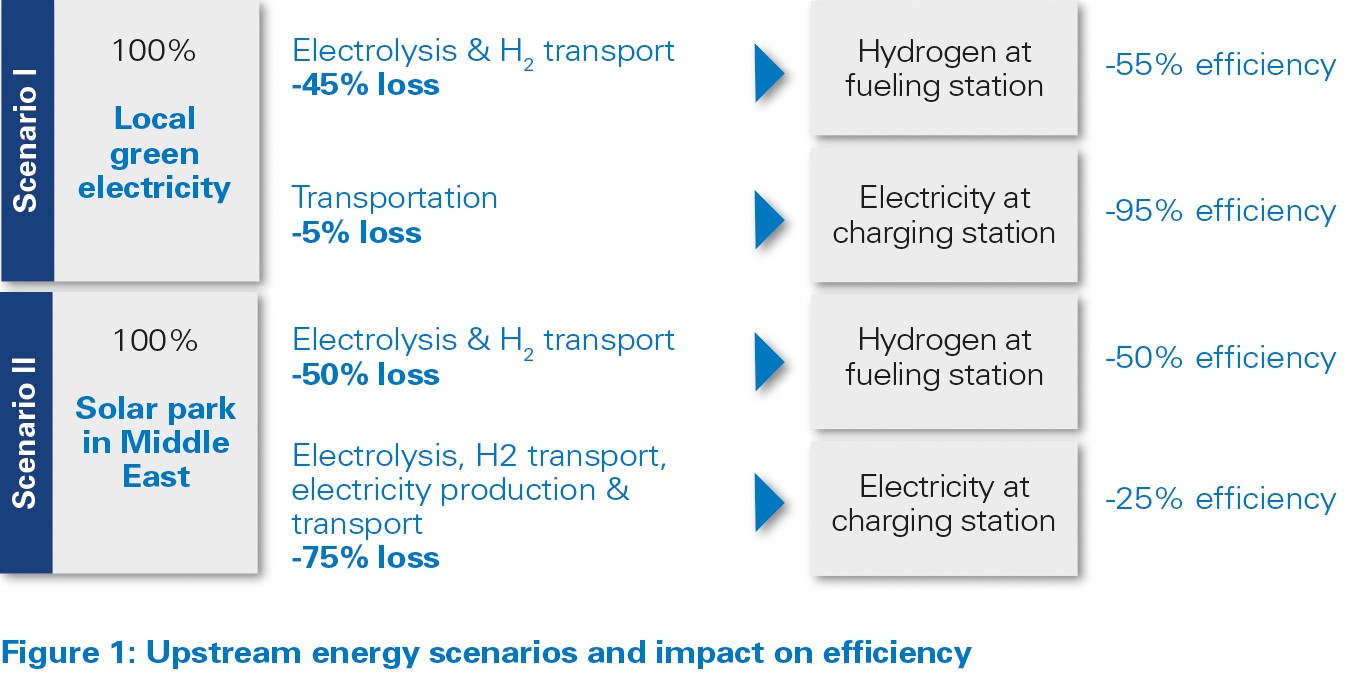

Furthermore, the efficiency of electricity compared to hydrogen for automotive applications varies dramatically depending on how green energy is produced. (See Figure 1.)

Locally generated green electricity delivers 95 percent efficiency, compared to 55 percent efficiency when using this source to create green hydrogen. However, as green electricity cannot always be generated locally at the time and on the scale needed, some energy generation will be required from remote locations (such as solar parks in the Middle East). In this case, since the produced electrical energy needs to be converted to hydrogen for long-distance transport and back to electricity for local consumption, the efficiency of electrical power drops to 25 percent, around half of the efficiency of hydrogen.

Challenging the assumption that green electricity is limitlessly available in the exact amounts, when and where needed, has an enormous impact on the applicability of BEVs and decreases their efficiency and green credentials. Green electricity production in Europe will not be enough to completely electrify the automotive sector, and even if this happened, the grid would not be able to cope with the transformation. It is also likely to have an impact on pricing, particularly around fast vehicle charging, which will significantly affect the operating costs of BEVs, such as in the heavy-duty/truck sector.

Hydrogen application in automotive mobility

This holistic approach to understanding the hydrogen economy leads us to the conclusion that hydrogen does have a key role to play in the zero carbon automotive sector of the future: there will be sufficient supply, pricing levels should not be prohibitive, and in many situations the real “source-to-wheel” efficiencies will be attractive versus BEVs.

Moving on to look at which automotive applications are likely to be the most attractive for hydrogen-powered fuel cells, heavy-duty trucks is the most obvious application for initial deployment. The large scale of the truck market is such that it can also act as enabler to other applications such as cars; hence, this will be decisive for the sector as a whole.

Assuming for now that both technologies, BEV and FCEV, will achieve technological requirements4, such as lifetime, range, handling of cold weather, vibration and refueling/recharging times, and further assuming that there will be an equal degree of regulation for both, four deciding factors remain:

1. Infrastructure: If needed, both BEV and FCEV infrastructure can and will be built up, but charging and refueling need to fit well to operational processes. Rapid charging of the large batteries needed for trucks is an even bigger challenge than high-performance charging for cars in terms of the infrastructure, parking space and time required. Every minute that a commercial vehicle is off road, it is losing money, which makes minimizing charging time vital.

2. Energy prices: With the decarbonization of electricity generation, electricity costs will be likely to increase substantially, potentially turning the current operatingcost advantage of BEVs into a disadvantage.

3. Autonomous driving: With autonomous driving, which is expected to arrive in this decade for trucks, charging times can no longer double up as mandatory driver breaks. This makes the long-range advantage of FCEVs even more significant.

4. Payload: A decrease in payload would negatively impact the business case. For high-energy demands and long-range requirements, batteries would weigh substantially more than the powertrain of FCEVs.

Strategic options for heavy-duty truck manufacturers

Coming back to the opposing positions in the automotive industry and looking at heavy-duty trucks in particular, manufacturers can take one of three strategic directions, each of which has its risks and relies on particular developments and scenarios taking place.

1. BEV-focused strategy Successful adoption would rely on a combination of low electricity prices, a smooth charging process and substantial, transformative improvements in battery performance. The major risk to this strategy is the impact of autonomous driving on commercial range

2. FCEV-focused strategy This relies on the fast emergence of a hydrogen economy with competitive prices and infrastructure in place. On the technology side, it requires advances in areas such as the durability of fuel cells above current development projections.

3. Dual with both BEVs and FCEVs This is based on the belief that FCEVs and BEVs are both needed for different use cases within heavy-duty trucks, or else are adopted as a strategy to mitigate the risk of choosing one technology above the other. The main risk of this strategy is that the split focus means that insufficient resources are devoted to each, so that the scaling of FCEV (and BEV) technology cannot be achieved within necessary time frames.

Based on our analysis outlined above, which concludes that a strong hydrogen economy will be created with competitive prices independent of the automotive industry, and BEVs will be impacted by relatively high charging prices due to increasing generation costs, high infrastructure investments, and competitive market dynamics, we have determined that:

- By 2030 FCEV trucks will have a lower total cost of ownership (TCO), costing around 1.5 euro cents per km and ton, compared to 1.7 euro cents for a BEV equivalent.

- These costs are likely to fall further post-2030 as the global hydrogen economy accelerates.

Of course, there are still many other things that need to be factored in, for example, potential changes in technology such as advances in battery technology, changes in regulation that impact the current equivalence of FCEV and BEV technology, and any decisions made on the use of nuclear that could impact the local generation and wider use of hydrogen. Furthermore, manufacturer strategies will also need to reflect the current product portfolio, regions targeted and capabilities.

Insights for the executive

Based on this broader perspective it becomes clear that commonly cited concerns around efficiency, prioritization or green hydrogen supply are not barriers to the use of green hydrogen in vehicles.

Efficiency is no argument against hydrogen

The industry needs to take a holistic view of decarbonization. Traditional efficiency measures will be different in a net zero world – inefficiencies in the use of green energy produced in the desert may yet turn out to be acceptable because of its stable, year-round supply. “Source-to-wheel” needs to be the metric to follow. Given that many nations will rely on imported green hydrogen, the only question is whether to convert it to electric power locally in the vehicle, or centrally, and then transfer it to charge large batteries.

A new global hydrogen ecosystem will be created

Hydrogen is a third major pillar in decarbonization, along with energy efficiency and electrification, and can be used in industry and power generation, as well as mobility. For many industrial (feedstock) applications, green hydrogen is the only decarbonization option available if countries are to meet the 95 percent reduction target.

The current view, which states that in regions such as Europe green hydrogen will be produced from renewables, will change as economies switch to green hydrogen generated elsewhere. Although optimal, cost-competitive supply locations are scarce (requiring political stability, wind, sun, space and water), there will not be the same level of dependency as in oil and gas. This is because renewables can be produced in more locations – less optimal sites will simply cost more, adding to the need for fast investment decisions.

Players need to take a holistic view

Given the diametrically opposed moves of the two biggest car builders, the unpredictable nature of regulation and the dependency on scenarios involving technology advancements (such as batteries) and energy supply strategies, players may struggle to place their bets wisely. To manage this well, they need to build a holistic understanding of the situation, with focus on energy supply, regulation and technology, creating a strategic foundation for these make-or-break decisions. The optimal choice will be application-specific – essentially, hydrogen is more advisable the larger the energy demand. A BEV-only strategy based on the perceived inefficiency and unavailability of green hydrogen should be reconsidered, especially for heavy-duty applications. Dual fuel strategies must assure sufficient scaling through partnering.

Define your path now

As decarbonization is a must, every player in the sector, whether a regulator, investor or provider in the field of mobility, needs to define its specific vision and strategy for transformation. A thorough cross-sectoral understanding is needed, for example, to be able to predict future regulations. Scenarios involving energy supply, regulation and technology need to be defined. A basic strategic point of view needs to be developed, covering how much to follow certain trends or whether to rely on a pure holistic sustainability position (akin to a value investor such as Warren Buffett), as well as preferences around risk and gain. The new ecosystem will offer a range of opportunities. Players (whether automotive, chemical or energy) need to position themselves now in the ecosystem, if necessary moving into related fields (e.g., electrolyzers, distribution). The hydrogen race has begun, with a global green hydrogen industry becoming mature post 2030. Organizations therefore need to invest now to secure leading positions in the ecosystem as it emerges.