32 min read • Financial Services

Banking on cryptocurrencies

Riding the wave of uncertainty

Executive Summary

Throughout their existence, currencies like the dollar, euro, and sterling have been issued and regulated by an overarching authority — a privileged position of power held largely by governments, central banks, and even individual banks, at one time.

Then, in 2009, a new form of money was born: the cryptocurrency. Unlike traditional fiat currencies, this was a digital asset without physical form — no notes, no coins — created by a technology called blockchain that has underpinned all the cryptocurrencies and non-fungible tokens (NFTs) that make up the world of digital collectibles ever since.

The first of these cryptocurrencies was Bitcoin. Brought into being by the mysterious figure of Satoshi Nakamoto (probably not one but multiple developers), its aim was to construct a “peer-to-peer version of electronic cash” [that] would “allow online payments to be sent directly from one party to another without going through a financial institution,” as Nakamoto’s original white paper described.[1]

Many believe that such peer-to-peer (P2P) payments have the potential to remove the friction and bias inherent in traditional payment systems, where banks and other intermediaries come between payer and recipient. They can also bring stability to emerging financial networks.

1

IMPROVING FINANCIAL INCLUSION

In sidestepping the dramas of the financial markets, cryptocurrencies potentially have a wider economic role to play. By creating the transparency needed to overcome widespread social trust issues and increasing access to financial services by performing the role of a quasi-bank account, cryptocurrencies have the potential to help alleviate poverty in developing countries and provide a boost to wider economic growth.[2]

In Africa, for instance, where 7.1% of South Africans and 8.5% of Kenyans use them,[3] digital currencies have already found their feet. For the financially marginalized, who find it difficult to open bank accounts and high transaction costs off-putting, crypto is a means to make payments, sending remittances with just a mobile phone and the Internet. Crypto is also appealing to the technically savvy as an investment since it allows them to hold assets that aren’t affected by rising inflation and depreciating local currencies.

And it is as an investment asset that cryptocurrencies are viewed for many, attracted by the potential for significant gain. Indeed, so strong was the demand from both retail and institutional investors that a tsunami of other cryptocurrencies followed in Bitcoin’s wake, launched by fintechs and blockchain start-ups, all trying to differentiate themselves through different value propositions in an ever more crowded market.

The result is seen in the creation of 19,000 cryptocurrencies (compare that to just 180 fiat currencies),[4] with a combined market value of around US $3 trillion by November 2021 and around 18% of Americans and 17% of Europeans said to have invested in some form of crypto-asset.[5] Globally, that figure is even higher, at 23%.[6]

Much of the activity takes place through brokerage platforms, where cryptos are traded for immediate settlement at a spot price. This allows the simultaneous buying and selling of coin. And since there are no barriers to spot market trading, small crypto investors can win (or lose) from high price fluctuations.

Transaction fees tend to be kept relatively low, at 0.1%-0.5% of the trade’s fiat currency value, to attract active day traders. The market leader, Binance, has a flat fee of only 0.1%. Generally, a minimum deposit is required from traders, which can be as much as $50, though Coinbase and Kraken have a $1 minimum.

Other factors that make platforms attractive are the number of currencies traded (50+ at least), along with ease of use. Most crypto-related transactions are done on mobile phones through an app, so ensuring a good user experience is paramount.

And consumers are wanting to do more than simply trade crypto. Increasingly, they are looking for lending and payment services, as well as more sophisticated, riskier options such as cryptocurrency derivatives.

One further element influencing platform choice is location. Given the potential for hacking and theft, local players are often perceived to be more trustworthy, especially if they are regarded as having been properly scrutinized by local or international regulatory authorities. As an example, Austria-based Bitpanda is considered reputable and is chosen by many in Central and Eastern Europe for the offline “cold” wallet storage (where assets are merely stored) it offers.

2

CREATING A WILD WEST

Such is the volatile nature of cryptocurrencies that the market can all too easily enter one of its periodic downturns — what’s referred to as a “crypto winter.” This happened at the end of 2021, when a mixture of adverse macroeconomic conditions and the failure of major crypto projects injected a negative sentiment into the market that is still apparent as we write this Report in the autumn of 2022. The market saw Bitcoin’s price drop 65% from its November 2021 high of $69,000, wiping $2 trillion off the crypto market’s collective worth. Adding to the volatility were large, high-profile purchases and sales like those of Tesla, which in July 2022 offloaded three-quarters of its $2 billion holding in Bitcoin. Previously, CEO Elon Musk had been one of cryptocurrency’s major cheerleaders, with his social media pronouncements often driving surges in trading.

Not surprisingly, risk-averse regulators view such volatility with concern, mindful that the crypto market is bigger than the subprime mortgage market was when it triggered the global financial crisis of 2007-2008. So, when crypto was just an esoteric “topic of interest,” it could be comfortably ignored because traded volumes were light, but that has changed and now it has become a potentially troublesome, heavyweight problem lurking just over the horizon.

In a recent speech, Fabio Panetta of the European Central Bank (ECB) categorized crypto as a “Wild West” investment, describing market activity as a “digital gold rush beyond state control.”[7]

Regulatory authorities like the Basel Committee on Banking Supervision (BCBS) have already signaled their worries that crypto assets might adversely impact banks’ liquidity and risk — market, credit, operational, legal, and reputational — and, consequently, the stability of the entire financial system. Headlines such as “How $60 Billion in Terra Coins Went Up in Algorithmic Smoke”[8] do little other than create a sense that cryptocurrencies are built on shaky ground. The International Monetary Fund (IMF) has commented that: “Crypto-assets are potentially changing the international monetary and financial system in profound ways.”[9]

US Federal Reserve Vice Chair Lael Brainard is someone who has voiced concerns when she said: “It is important that the foundations for sound regulation of the crypto financial system be established now before the crypto ecosystem becomes so large or interconnected that it might pose risks to the stability of the broader financial system.”[10]

And this takes us to the center of the crypto conundrum: regulation. And, most particularly, how much there should be and what form it should take.

Some countries, such as China, Indonesia, and Turkey have banned cryptocurrency transactions outright, citing concerns not just over financial instability but also the use of cryptos for money laundering and terrorist financing. How valid are such concerns? It is difficult to say.

While crypto has long been considered a hotbed of criminal activity, in reality, this could be overstated. Research by blockchain data platform Chainalysis suggested it accounted for under 1% of total crypto activity between 2017-2020.[11] Whether or not this figure is accurate, the truth remains that better know-your-customer (KYC) regulations, periodic reporting, and greater penalties for violations will help dampen bad actor events. This, in turn, will increase trust in cryptocurrencies.

3

CONTROL & MANAGEMENT

Rather than banning crypto, most countries are taking a more pragmatic view by seeking to find ways to better manage its impact. So, driven by Europe, efforts have begun to develop a globally coordinated regulatory approach to crypto assets, improve levels of transparency, and establish new codes of conduct and standards for disclosure and reporting. The Financial Stability Board (FSB), the Basel Committee on Banking Supervision (BCBS), the Committee on Payments and Market Infrastructures (CPMI), the Financial Action Task Force (FATF), and Germany’s Federal Financial Supervisory Authority (BaFin) are some of the key authorities working on the effort.

These discussions tend to focus currently on limiting exposure to unbacked cryptocurrencies and setting specific capital requirements for different types of crypto assets. They also cover areas such as the taxation of crypto assets, strengthening public disclosure and reporting, transparency levels and standards of conduct, as well as anti-money laundering (AML) solutions and combatting the financing of terrorism (CFT).

For the moment, what we are seeing are ad hoc measures being taken by the likes of the Monetary Authority of Singapore, which has said it will broaden its cryptocurrency regulations so more activities are covered.[12] This is in the light of recent failures of various crypto firms with operations in the country.[13]

But there seems to be a growing move toward tighter regulation by governments around the world that are increasingly worried that privately operated, highly volatile digital currencies could undermine their control of financial and monetary systems.

Other nations are now starting to take stronger action against what they see as infringements. As an example, the world’s largest crypto exchange, Binance, was fined $3.4 million by the Dutch Central Bank for operating without authorization in the Netherlands.[14]

There is no doubt that regulation is coming down the line. As Securities and Exchange Commission (SEC) Chair Gary Gensler has pointed out, “Few technologies in history, since antiquity, can persist for long periods of time outside of public policy frameworks.”[15]

The debate will surround the level of regulation that is needed, whether existing rules are being applied, and if the best way to actually supervise the activities of coin issuers is to bring them into the banking system, as some argued in testimony to the US Congress’s House Financial Services Committee in December 2021.[16]

Since then, the US Federal Reserve has issued guidance to banks that might be considering any cryptocurrency activity, making clear that they must notify the authorities of their intentions and make sure that what they are doing is legally permitted.[17] Given the significant fines previously meted out to those considered in contravention of AML, taxation, and consumer protection rules, financial institutions operating in the “gray zone” do so at their peril.

For their part, banks would welcome clear regulations to enable them to move forward with confidence, rather than overstepping the mark or holding back for fear of making a mistake.

Ultimately, there may be no consensus on regulation, with some regions opting to go light on regulation in an attempt to gain economic advantage, or even doing so at a local level. For example, New York City Mayor Eric Adams is intent on transforming the city into a hotspot for cryptocurrency.[18]

So, while strong reservations remain, there is a growing recognition that crypto is here to stay, though as yet only two countries, both small and with no fiat currency of their own, accept crypto as legal tender. The Central African Republic (CAR) started doing so this year, and El Salvador began accepting Bitcoin in 2021.

While it is too early to assess what is happening in the CAR, El Salvador’s Bitcoin experiment is perhaps not going well. Plans to build the world’s first cryptocurrency city have stalled, and the use of cryptocurrency has failed to catch on. One survey shows that just one-fifth of Salvadorans have downloaded the government’s Bitcoin digital wallet (Chivo) and continued to use it after spending the $30 it came loaded with.[19] And while the government has encouraged Salvadorans abroad to send money home through Chivo, only about 2% of remittances between September 2021 and June 2022 were through the wallet.

Despite such apparent setbacks, the government of President Nayib Bukele says its Bitcoin policy has attracted investment, reduced bank commissions to zero, increased tourism, and promoted financial inclusion. In contrast, the IMF says El Salvador should revoke Bitcoin’s status as legal tender because of financial, economic, and legal concerns.

While making privately owned cryptocurrencies legal tender is still a step too far for most countries, many central banks are now exploring the idea of issuing a digital currency that they will regulate: centralized bank digital currencies (CBDC). A survey by the Bank for International Settlements (BIS) found that 81 were developing projects in this area.[20] China is testing a “digital yuan,” while Nigeria has the e-Naira and Jamaica the JamDex.

With over half of the world’s top banks taking a growing interest in cryptos,[21] after years of resistance the tide may be turning. Even BIS, which has always viewed crypto with some skepticism, is saying that it may allow banks to hold up to 1% of their reserves in Bitcoin and other cryptocurrencies.[22]

4

THE CULLING OF THE CRYPTO HERD

Given the sheer number of cryptocurrencies, it is not difficult to predict that very soon there will be a major retrenchment. How many of today’s standard cryptos can have a long-term future when they are neither distinctive nor have any real purpose other than as a speculative vehicle that can be easily manipulated through “pump and dump” schemes that push up prices, enabling those in the know to sell off their coin and let others take the hit as prices fall?

Because major trust issues remain around crypto, investors may well gravitate toward top-tier currencies that are seen as more reliable or having something extra to offer. This will lead to a game where whoever is left behind loses, as lower layers of stragglers fall by the wayside either through lack of demand (they don’t have the ease of use or level of features sought by users and investors) or from the tightening of regulations that hit those who take too many risks.

Eventually, we are likely to see the majority of cryptos disappearing from the market, leaving perhaps just 30 to 50 ”winners” still standing, regarded as trustworthy, reputable, or reliable by investors. Among the survivors will presumably be the original Bitcoin, still a dominant force, though its position has been diluted by the arrival of so many other cryptos — as of early November, it has less than 40% of the market, according to CoinMarketCap, much lower than the 70% of early 2020. Ethereum, the other big player in the space, had about 18.8% of the crypto total market capitalization at the same time.

Some may survive because they have a well-established local or regional following or because they are ”stablecoins” like Tether and US Dollar Coin, which are backed by a fiat currency and are favored because they are seen as less risky. However, some of these may be stable in name only, since not all issues are supporting their coins with real fiat currency in a bank or are held as they should be. This means there is potential for a run on stablecoins. As the President’s Working Group on Financial Markets observed in its November 2021 report, stablecoins are too big to ignore, but not yet too big to fail from a systemic risk point of view.[23]

We had a small taste of the market’s fragility with the crash of TerraUSD and the subsequent knock-on effects that saw its sister coin, Luna, also fail.[24] This took the market by surprise, since Terra was a stablecoin pegged to a fiat currency (in this case, the US dollar). But at the time of writing, having maintained almost exact parity with the dollar since its release, Terra is worth just $0.00025 (€0.00025). With TerraUSD losing its peg to the dollar, it seems that stablecoins may not be quite as stable as might be believed.

As Steven Maijoor, Executive Director of Supervision, Dutch Central Bank (De Nederlandsche Bank), said in February 2022, “Perhaps the most fundamental question is this: in a system where so many new, previously non-financial players are becoming instrumental in offering financial services, how are we, as financial supervisors, going to ensure that the financial system remains robust and consumers stay safe? How can we make sure that we continue to have the right mandate and effective instruments to ensure that outcome?”

Though not connected to the Terra Luna fallout, there is also the case of Nuri Bank, a crypto-focused digital bank in Germany that recently became insolvent. While the company blamed “significant macroeconomic headwinds” arising from COVID-19 and Russia’s invasion of Ukraine, plus the “cooling down of public and private capital markets,” the primary reason was the bankruptcy of Celsius Network, one of the leading decentralized finance (DeFi) platforms, which had serious knock-on effects in the crypto sector.[25]

Cryptocurrency lender Celsius also crashed in July 2022, with some declaring that this had all the makings of a scam. Paul Romer, a Nobel prize-winning economist at New York University, said that the high interests Celsius had been able to offer “were pure Bernie Madoff,” the American fraudster convicted of running the world’s largest Ponzi scheme.[26]

All this has contributed to a crypto bear market.

DISSECTING THE CRYPTO VALUE CHAIN

The cryptocurrency chain is complex and far-reaching, stretching out as it does across society and the real economy, and involving various regulatory bodies and many different players in multiple marketplaces.

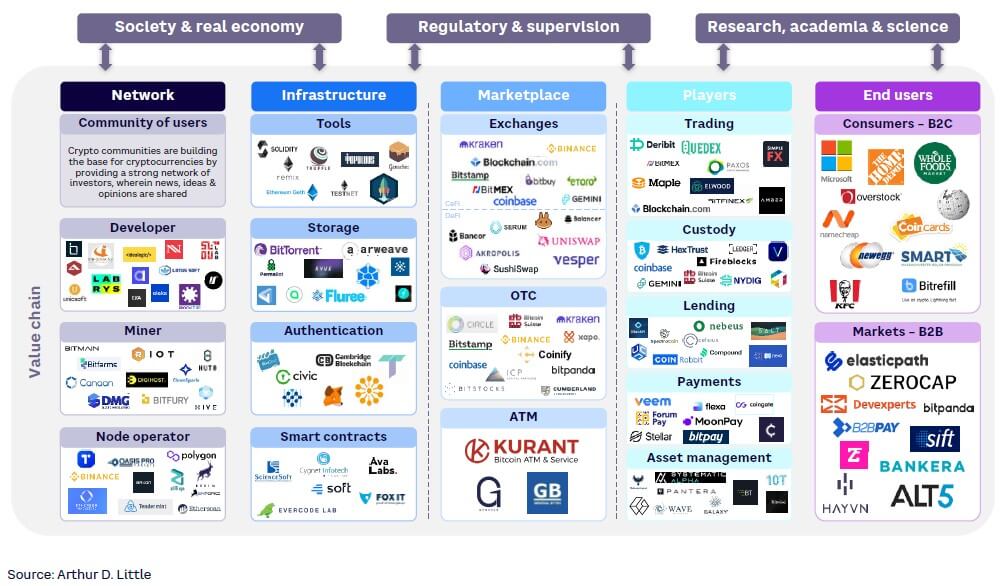

Looking in more detail at who occupies this space, it becomes clear that there is not a decentralized system as it is so often portrayed, given that the crypto infrastructure is actually in the hands of relatively few companies. Figure 1 illustrates the different tiers of players that together make up the crypto environment.

The network tier

-

Developers — create blockchain and software solutions that provide the crypto community with the technical capacity it needs (e.g., Idealogic, Lotus Soft, Blockcypher, Eva).

-

Miners — solve the complex algorithms required to generate new bitcoins and other cryptocurrencies (e.g., Bitfarms, Canaan, BitMain, Bitfury).

-

Node operators — run the high-performance infrastructure that validates any new blocks written to the blockchain and then broadcasts them to the rest of the network (e.g., Polygon, Nyala, Tendermint, Etherscan).

The infrastructure tier

-

Tool creators — provide ancillary software for blockchain testing (e.g., Solidity, Ethereum Geth, Truffle).

-

Storage solution providers — help to organize and share blockchain-secured data (e.g., Fluree, BitTorrent, PermaBot, Arweave).

-

Authentication services — maintain the distributed networks that underpin the blockchain ecosystem (e.g., Cambridge Blockchain, Civic, ShoCard).

-

Smart contract providers — programs automate the execution of agreements on the blockchain (e.g., Evercode Lab, Fox IT, Ava Labs, Cygnet Infotech).

The marketplace tier

-

Exchanges — where crypto can be traded for both conventional fiat currencies and other digital coins. These include more traditional institutions such as the Stuttgart Stock Exchange, which provides a crypto infrastructure for banks (as well as companies like Kraken, Coinbase, Binance, Bitbuy).

-

Over-the-counter (OTC) trading firms — the fintechs that enable buyers and sellers of crypto to trade outside a regular exchange (e.g., Bitpanda, Bitcoin Suisse, Coinify).

-

ATM — automated teller machines where Bitcoin and other cryptos can be bought using cash or a credit card (e.g., Kurant, General Bytes, Genesis).

The players tier

-

Trading companies — provide services to facilitate the buying and selling of cryptocurrencies (e.g., Deribit, Paxos, Maple, Bitfinex, Amber, FirstCoin.de).

-

Custody firms — offer users a secure location to store and manage their digital assets (e.g., Gemini, Fireblocks, Ledger, NYDIG, Metaco, Tangany).

-

Lending companies — allow you to lend and borrow against your digital assets (e.g., BlockFi, CoinRabbit, Nexo).

-

Payment service providers — enable the spending of cryptocurrencies (e.g., BitPay, CoinGate, MoonPay, Veem).

-

Asset management firms — dedicated to managing portfolios of digital assets (e.g., Pantera, Galaxy, Wave Financial, Bitwise).

The end users

-

B2C — major companies that have begun to accept crypto for purchases (e.g., Microsoft, The Home Depot, KFC, Overstock).

-

B2B — providers of crypto-friendly banking accounts (e.g., Bankera, B2Bpay, Zerocap, Elastic Path).

5

HOW SHOULD BANKS ADAPT?

So how should financial institutions position themselves in this new environment where crypto is increasingly legitimate, and in what areas should a bank choose to play? That is very much down to the individual institution, its appetite for risk, and its specific take on the market’s point of arrival.

It could, for instance, eschew this whole area and remain outside the crypto playing field altogether, leaving others to serve the market. If the market doesn’t stabilize and crypto’s reputation continues to be trashed by highly volatile price swings, then this principled approach may be a sensible one. However, it does seem to cut across the direction of travel.

Or an institution can assume that it will enter the market at some point, just not right now. Playing the “wait and see” game is a pragmatic solution, though it could leave one having to play catch-up in a fast-moving marketplace.

Alternatively, financial players could dip test the waters by providing a limited range of crypto services, enabling their customers to participate in the market without actively engaging themselves.

They might, for instance, provide crypto custody services to store digital assets and digital wallets that have a shareable public address, like the IBAN of a bank account, with a private digital key used by the account holder to control access. Cryptocurrency custody has become a highly active area, with 73 new services launched in 2021. Players in this segment now include US Bancorp, Bank of New York Mellon, Deutsche Bank, BNP Paribas, JPMorgan Chase, and HSBC.

However, offering a cryptocurrency custody service is not without risk. While providing offline “cold” wallets, where assets are merely stored is one thing, any bank offering a “hot” wallet that is connected to the Internet and used for trading or payments has to be strongly secured against high-level hacks and thefts. The recent illegal siphoning of $190 million in cryptocurrencies from US crypto firm Nomad clearly demonstrates what can happen, especially when you are the target of well-organized bad actors.[27]

North Korea, for example, has made stealing cryptocurrency part of its strategy to mitigate the country’s financial isolation. In the first half of 2022, crypto-research firm Chainalysis calculated the regime had already stolen over $840 million, mainly from decentralized financial platforms.

There are also unpredictable risks over which you have little influence, such as a bug in a layer 1 protocol (the blockchain layer), which then disrupts the cryptocurrencies and smart contracts that are built on it.

If that were not enough, there are decisions to be made about which cryptocurrencies to support, because that will have a big impact on the IT infrastructure required. If you don’t want to have to change that infrastructure too frequently, you need to be picking “crypto winners.” And that is not easy to do — an infrastructure that would have supported the top 10 cryptocurrencies five years ago would only be capable of supporting three of them today.

Because of this volatile market situation, any organization offering crypto-related products or services must have an IT infrastructure that can react fast and respond flexibly to market changes. And to do this, organizations must be aware of not just factors that impact them directly, but also events and circumstances affecting others they may be connected with. An investment in or collaboration with company A, for instance, could leave you unexpectedly exposed if you are unaware they are heavily invested in Bitcoin, and the crypto market turns. The situation becomes even more opaque if company A is involved with company B, which also has cryptocurrency holdings. Such interconnectedness means additional due diligence is required to identify potential risks.

And unlike most other digital transactions between banks, cryptocurrency transactions are nonreversible, which means that often very little can be done to recover any money. We may have a wealth of knowledge about how to protect physical assets, but measures to keep cryptocurrencies secure are still in their infancy.

Besides crypto custody, more banks are beginning to expand their portfolio of services to include crypto-asset trading. Goldman Sachs was one of the first major US banks to offer OTC trades, while Citigroup is looking to offer Bitcoin futures trading for some institutional clients, dependent on regulatory approval. Even those considered traditional banks are becoming involved. Italy’s Banca Generali, for example, has teamed up with Italian-American cryptocurrency exchange Banca Generali Conio, enabling customers to use an app to buy cryptocurrencies through their regular banking account.

And French fintech Lydia has partnered with the Austrian investment start-up Bitpanda so that its 5.5 million users can now invest in cryptocurrencies, while London-based Revolut is looking to set up an in-house crypto-exchange platform and launch its own token.

Financial institutions that decide to hold cryptocurrencies as assets, provide crypto-based products, or offer crypto-custody services to other institutions will need to revise their operating model to meet regulatory requirements.

Institutions offering cryptocurrency as an asset will need to ensure they have sufficient liquidity and are able to store and transfer assets safely. As a digital custodian, they will also need to be confident that their current AML and KYC capabilities remain compliant for cryptocurrencies. They may have to modify their software ecosystem and processes accordingly.

The illustration of a target operating model of a crypto bank in Figure 2 shows that the main architectural changes required will revolve around connectivity to public or permissioned blockchains, and to other services such as crypto exchanges, as well as crypto brokers and issuers.

Further key, critical changes will be needed to core banking software, where additional applications will be required for functions such as digital custody and tokenization.

There are also potential opportunities in crypto lending and borrowing. Under a crypto-lending model, private investors receive interest payments for allowing lenders to use their cryptocurrency to make loans to institutional and corporate borrowers. Though interest rates vary widely between lending platforms, with each lender having different rates for different coins, typically these fall between 3% to 8%. However, rates for stablecoins are generally higher, at between 10% and 18%.

This is a very fast means of financing — transactions happen within a matter of hours — with much potential for customization of terms. On the flip side, by crypto borrowing, private investors can take out a loan secured against their crypto holdings, usually capped at 50% of asset value.

And since professional investors and high-net-worth individuals hold almost two-thirds of the Bitcoin supply, providing a wealth management service that encompasses crypto assets would be of obvious benefit to banks. However, their wildly deviating prices mean cryptocurrencies must be regarded as a high-risk investment that much like commodities needs to be actively traded, rather than considered a stable store of value that just needs to be managed. Morgan Stanley, Wells Fargo & Co, and Goldman Sachs are just a few of those already in this space.

6

THE FUTURE OF CRYPTO

Gazing into a crystal ball is fraught with uncertainty at the best of times, but particularly so when it comes to the future of cryptocurrencies. But that should not stop us from asking questions about the direction of travel and what the implications might be for financial institutions.

IS CRYPTO HERE TO STAY?

It very much seems so. Even as the market undergoes a crypto winter, venture capitalists (VCs) are looking to pour money into digital currency and blockchain start-ups. Data from PitchBook shows that VCs invested $17.5 billion in such firms during the first half of 2022, which means that the $26.9 billion raised in the whole of last year is likely to be surpassed.

North America has been a particular hotspot, where in contrast to the downturn in VC activity generally, in the six months to June 2022 about $11.4 billion flowed into crypto-related start-ups, not far behind the $15.6 billion for the whole of 2021. VC investment is also strong in Europe, with $2.2 billion in funds raised in the first half of the year.

The financial services sector is increasingly enthusiastic about cryptocurrency applications and the blockchain technology that underpins them — some estimate that around 30% of investment banks’ infrastructure costs could be stripped out by using blockchain.

The market for blockchain in banking and financial services is expected to reach $12.39 billion in 2026, up from $1.17 billion in 2021, a CAGR of around 60%.[28]

WILL CRYPTOCURRENCIES BE PRIMARILY FOR PAYMENTS?

At the moment, cryptocurrencies are generally considered an investment rather than a vehicle for payments. However, there is a widespread belief that they offer great potential as a means to improve financial inclusion in countries that don’t have cheap and easy-to-use banking systems. The World Economic Forum, for instance, advocates the use of blockchain technology and cryptocurrencies to help create more open and democratic financial systems.[29]

Crypto could, for instance, help people transact without the need for intermediaries, which would be of real advantage to the many around the world who do not have bank accounts and depend instead on checks, money orders, and cash. With some 1.7 billion people in the world today considered “unbanked,” according to the World Bank — which means as many as six out of 10 adults in some countries — cryptocurrencies are a way to promote financial inclusion. Cryptos are already regular means of payment in Vietnam, India, and Pakistan.

Cross-border payments to other countries have traditionally been expensive, operationally complex, and may take up to several days to be credited. However, international payments could be made simpler and cheaper by embracing crypto and blockchain solutions. So, rather than having to wait days for payments to be credited, as happens for instance between EU and non-EU countries, by using Ripple’s XRP Ledger, banks could not only achieve operational advantages but also be able to offer customers low-cost, real-time transfers.

Where banking systems are more developed, there are further opportunities, such as programmable payments that are executed automatically when certain conditions are met. This type of payment already exists in the form of standing orders and direct debits. However, far more complex business processes could be embedded into automated payments by using blockchain technology and smart contracts.

For example, autonomous electric vehicles could pay for their own power at charging stations, with that payment automatically divided in predefined proportions between the electricity provider, the charging station manufacturer, the station operator, and the car manufacturer — all done through smart contracts.

HOW WILL COIN RISK & RETURN PROFILES CHANGE?

It is almost certain that the crypto markets will become ever more regulated, and this is likely to have a profound impact on the risk and return profile of crypto generally. But it is difficult to say what those changes will be, not only because of fast-changing market conditions, but also because of how the regulatory framework might evolve. And the implications for the whole industry, not just individual coins, can be enormous.

For instance, a lawsuit being brought by the Securities and Exchange Commission (SEC) against three workers at Coinbase will determine whether a crypto asset should be classified as a security. If it is deemed that it is, anyone issuing crypto would need to register with the SEC and comply with a long list of disclosure rules. This would potentially mean a massive shift for the industry, undoubtedly sounding the death knell for many issuers of cryptocurrencies unable to comply with those regulations.

CAN CRYPTOCURRENCIES EVER BE SUSTAINABLE?

Crypto mining has generally been a highly energy-intensive process requiring many powerful computers to solve the complex math problems on which blockchains are based. In fact, about a third of the world’s computing power is now dedicated to mining Bitcoin, with the US the global center since China banned crypto mining in the autumn of 2021.

This raises significant ethical and environmental concerns that may be at odds with an organization’s environmental, social, and governance (ESG) position.

As an industry, crypto mining is now consuming more energy than entire countries. The annual energy consumption used to mine Bitcoin, for example, is the same as the total electricity consumed by the Netherlands in a year — the energy consumption of Bitcoin is 110 TWh and that of the Netherlands 108 TWh, according to research by Cambridge University. Globally, crypto-asset activity consumes more electricity than Argentina every year. This makes the mining of $1 of Bitcoin more carbon-intensive than digging a dollar’s worth of gold out of the ground.

The problem arises from the proof of work (PoW), the process used by many cryptocurrencies, including Bitcoin. Anonymous miners compete to solve the complex mathematical problems that are part of verifying blockchain transactions in return for payment in Bitcoins. The more difficult the problem, the more energy is needed.

Emissions data from just three of the largest Bitcoin mining companies — Bit Digital, Greenidge, and Stronghold — indicate that their operations create 1.6 million tons of CO2 annually, an amount produced by nearly 360,000 cars.

There is also the adverse impact on energy prices. In Upstate New York, US, for example, annual electricity bills are some $165 million higher for small businesses and $79 million for individuals than they would be without crypto mining.[30]

If governments and regulators chose to restrict energy use for crypto mining, that would have a significant impact on those still using PoW, which could see high-energy consumption coins being regulated out of existence in favor of less environmentally damaging alternatives.

There are signs that the crypto industry recognizes it has an ESG problem and must do more to address this issue, for instance, switching Bitcoin mining from PoW to proof of stake (PoS) mining, where someone on the network is chosen to make the next update rather than everyone competing for a piece of the pie.

One of the largest players, Ethereum, recently completed a long-planned move to PoS (Ethereum 2.0), something that will not only make transactions in this currency faster but also much more sustainable. If PoS were adopted wholesale, it could reduce the collective carbon footprint of Bitcoin alone by more than 99%.[31]

This leads us perhaps to the biggest question of all. Given the global climate crisis and the massive energy price spike triggered by the Ukraine war, can we actually afford crypto? It’s a legitimate question and one that may have increasing potency if the industry cannot find ways soon to dramatically reduce its energy consumption.

SHOULD A BANK CREATE ITS OWN COIN?

Some banks are already doing so. JPMorgan Chase & Co, for instance, has set up the world’s first bank-led blockchain platform, Onyx, complete with its own JPM coin and blockchain-based interbank payment network.

However, since many established financial institutions are notoriously overburdened with inappropriately high levels of legacy tech, rather than adding to the layers with new crypto apps and hardware, they may choose instead to plug into another’s expertise. So, even as the sector is hit by a run of bankruptcies, Barclays has taken a stake in Copper, a prominent cryptocurrency firm providing custody, prime broking, and settlement services to institutional investors.

WHAT WILL A NEXT-GENERATION CRYPTO BANK LOOK LIKE?

Figure 3 neatly sets out the core components of a crypto bank. Not only will this have a strong technology core to underpin what it does, but it will also be highly customer-centric, as well as having the capacity to continually adapt to a changing marketplace.

Due to the current volatility of most cryptocurrencies and the unclear legal situation surrounding them, crypto is potentially a high-risk area for banks that could certainly pose a risk to the stability of a financial institution. This means that banks must think carefully about where in this area they are going to play.

For instance, if they want to offer a crypto-trading service to their customers, they will have to perform due diligence checks on traded currencies, update their risk management framework accordingly, set up internal cryptocurrency governance protocols, and make sure that a robust, ongoing risk assessment is in place. Besides this, all banking processes will need to be reviewed and then changed if they are found wanting.

Measures to combat money laundering, terrorist financing, compliance, and consumer protection all become more complex because of the lack of transparency surrounding crypto assets. For instance, provision needs to be made to ensure no transactions are made using wallets blacklisted by regulatory authorities.

Banks also need to think about the consequences of operating in countries where crypto may be banned or heavily regulated to ensure that no customers there can access cryptocurrencies and that the functions of data centers are appropriately ring-fenced.

Financial institutions will also need to look beyond normal regulatory and legal requirements. The technology used in cryptocurrencies is relatively young, which makes it potentially vulnerable to security risks. Banks should be aware of the need to build resilient systems against quantum computer attacks, for example.

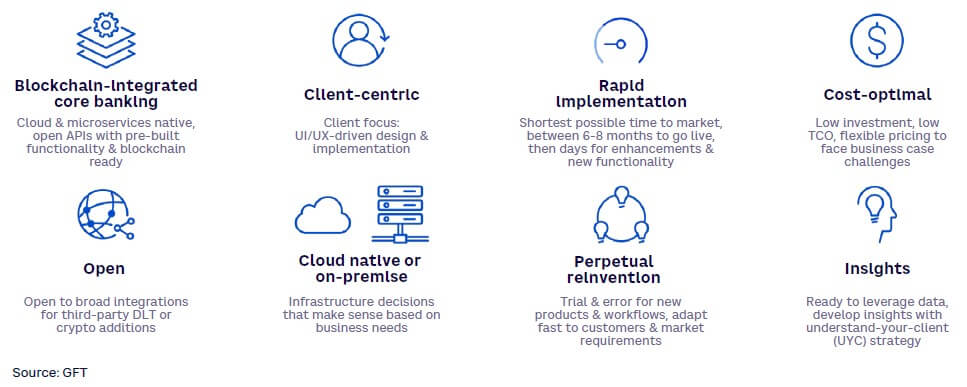

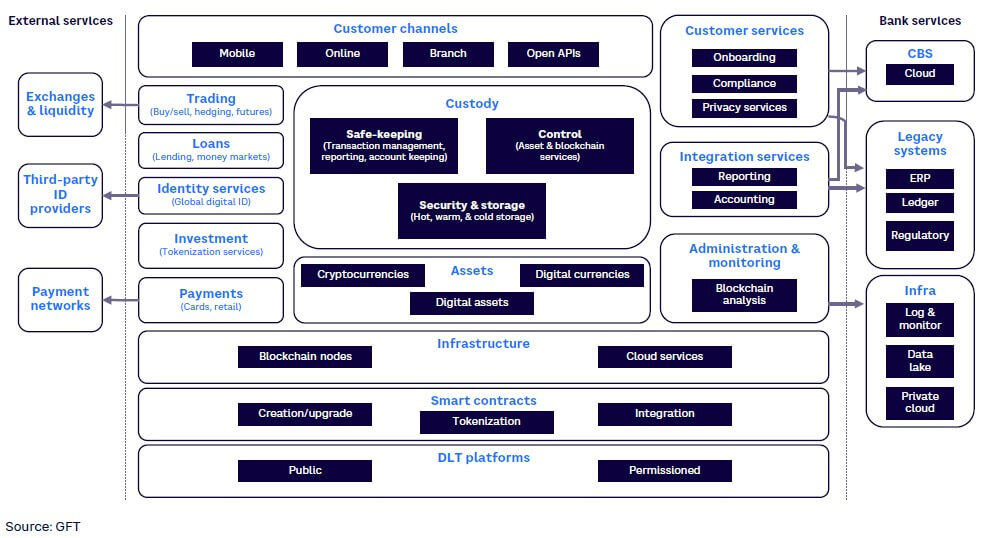

Though it’s a complex process, it is possible for banks to begin offering crypto services relatively quickly. GFT, for instance, offers a crypto-bank architecture, CryptoSandbox (see Figure 4) — a process that should enable banks to have a preproduction crypto offering ready in just eight weeks and be able to go fully live in five to six months.

The architecture shown in Figure 4 is a hybrid model in which some systems use traditional banking systems while others are based on blockchain technology.

WILL CRYPTOCURRENCIES EVER BE MAINSTREAM?

Does crypto have that degree of leverage? Some calculations suggest that the widespread use of digital finance could add $3.7 trillion to the annual GDP of all emerging economies and create an additional 95 million jobs across all sectors by 2025.[32] Similarly, it could dramatically cut the cost of cross-border transfers, saving corporations as much as $120 billion a year in transaction costs.[33]

Reducing the price volatility of cryptos and addressing regulators’ worries about financial instability and money laundering might lead to a higher degree of trust and public confidence in these assets.

CONCLUSION

THE UNKNOWN UNKNOWNS

It is certainly an interesting time for cryptocurrencies. On the one hand, they are going through a period of swift and significant falling prices, while in parallel they are being taken perhaps more seriously than they ever have been by mainstream financial institutions. As we have seen, central banks have become more comfortable with digital assets, with the BIS seemingly minded allowing a small percentage of banks’ reserves to be held in cryptocurrencies. And individual banks themselves have begun to enter the market despite their previous reluctance.

Having been left out in the cold for so long, crypto is now becoming hot, though there remains the question of the market’s volatility. The demise of many cryptocurrencies, something we see as inevitable, should bring some stability to the market, as will the introduction of tighter regulation. So will cryptos be a safer bet in five years? Probably. But as with much else with digital assets, it is much easier to ask questions about them than to answer them. To paraphrase one-time US Defense Secretary Donald Rumsfeld, the world of crypto is too filled with “things we don’t know we don’t know” — the “unknown unknowns” — to predict the future with any kind of confidence.

With that said, if they are to become players in a game that, despite its frequent setbacks, seems to be on an upward trajectory, then banks need to decide where they are going to play and what degree of risk they are willing to accept all along the crypto value chain. However, with the market currently so volatile, deciding which risks are acceptable will not be an easy question to answer.

Notes

[1] Nakamoto, Satoshi. “Bitcoin: A Peer-to-Peer Electronic Cash System.” Satoshi Nakamoto Institute, 31 October 2008.

[2] “The Impact of Crypto Currencies on Developing Countries.” NewsWatch, 23 June 2021.

[3] “All that Glitters Is Not Gold: The High Cost of Leaving Cryptocurrencies Unregulated.” United Nations Conference on Trade and Development (UNCTAD), Policy Brief No. 100, June 2022.

[4] Kharpal, Arjun. “Crypto Firms Say Thousands of Digital Currencies Will Collapse, Compare Market to Early Dotcom Days.” CNBC, 3 June 2022.

[5] Hurst, Luke. “Crypto Adoption in Europe Lags Behind Most of the World — But This EU Country Is the Most Responsive.” Euronews.next, 4 April 2022.

[6] Ibid.

[7] Panetta, Fabio. “For a Few Cryptos More: The Wild West of Crypto Finance.” Speech at Columbia University, 25 April 2022.

[8] Shen, Muyao. “How $60 Billion in Terra Coins Went Up in Algorithmic Smoke.” Bloomberg, 21 May 2022.

[9] Adrian, Tobias, Dong He, and Aditya Narain. “Global Crypto Regulation Should be Comprehensive, Consistent, and Coordinated.” International Monetary Fund (IMF) Blog, 9 December 2021.

[10] Macheel, Tanaya. “Fed’s Brainard Says Crypto Needs Regulation Now Before It Becomes So Big That It Threatens Financial System.” CNBC, 8 July 2022.

[11] The 2022 Crypto Crime Report.” Chainalysis, 2022.

[12] Ghosh, Suvashree, and Faris Mokhtar. “Singapore Plans to Broaden Crypto Regulations After Shakeout.” Bloomberg, 19 July 2022.

[13] Lagerkranser, Philip, and Anuchit Nguyen. “Crypto Woes Spread as Celsius, Babel Links Hit Another Firm.” Bloomberg, 21 July 2022.

[14] Browne, Ryan. “Crypto Exchange Binance Fined $3.4 Million by Dutch Central Bank for Operating Illegally.” CNBC, 18 July 2022.

[15] Kiernan, Paul. “SEC Had ‘Interesting’ Meetings with Crypto Firms, Gensler Says.” The Wall Street Journal, 7 December 2021.

[16] Livni, Ephrat. “Congress Gets a Crash Course on Cryptocurrency.” The New York Times, 8 December 2021.

[17] Schroeder, Pete, and Hannah Lang. “Federal Reserve Issues Guidance for Banks Considering Crypto Activities.” Reuters, 16 August 2022.

[18] Sigalos, MacKenzie. “New York’s Incoming Mayor Says Crypto Should Be Taught in Schools.” CNBC, 8 November 2021.

[19] Renteria, Nelson. “A Year on, El Salvador’s Bitcoin Experiment Is Stumbling.” Reuters, 7 September 2022.

[20] Kosse, Anneke, and Ilaria Mattei. “Gaining Momentum — Results of the 2021 BIS Survey on Central Bank Digital Currencies.” Bank for International Settlements (BIS) Paper, No. 125, May 2022.

[21] “Top Banks Investing in Crypto and Blockchain May 2022 Update.” Blockdata, 4 September 2022.

[22] Khatri, Amara. “BIS May Allow Banks to Hold 1% of Reserves in BTC.” Crypto Daily, 1 July 2022.

[23] President’s Working Group on Financial Markets, the Federal Deposit Insurance Corporation, and the Office of the Comptroller of the Currency. “Report on Stablecoins.” US Department of the Treasury, November 2021.

[24] Shen, Muyao. “How $60 Billion in TerraCoins Went Up in Algorithmic Smoke.” Bloomberg, 21 May 2022.

[25] Asmakov, Andrew. “German Crypto Bank Nuri Files for Insolvency, Says ‘All Funds Are Safe.’” Decrypt, 10 August 2022.

[26] Fortson, Danny. “How the Bitcoin Boom Led to ‘A Giant Fleecing of Ordinary People.’” The Sunday Times, 21 August 2022.

[27] Whitney, Lance. “Hackers Steal Almost $200 Million from Crypto Firm Nomad.” TechRepublic, 3 August 2022.

[28] “The Rising Use of Cryptocurrency Is Expected to Drive the Blockchain in Banking and Financial Services Market.” The Business Research Company, 9 August 2022.

[29] Moy, Christine, and Jill Carlson. “Cryptocurrencies Can Enable Financial Inclusion. Will You Participate?” World Economic Forum, 9 June 2021.

[30] Parshley, Lois. “How Bitcoin Mining Devastated This New York Town.” MIT Technology Review, 18 April 2022.

[31] Cleanupbitcoin.com, accessed October 2022.

[32] “Digital Finance for All: Powering Inclusive Growth in Emerging Economies.” McKinsey & Company, September 2016.

[33] Ekberg, Jason, et al. “Unlocking $120 Billion Value in Cross-Border Payments.” OliverWyman, 2021.

DOWNLOAD THE FULL REPORT

DATE

Executive Summary

Throughout their existence, currencies like the dollar, euro, and sterling have been issued and regulated by an overarching authority — a privileged position of power held largely by governments, central banks, and even individual banks, at one time.

Then, in 2009, a new form of money was born: the cryptocurrency. Unlike traditional fiat currencies, this was a digital asset without physical form — no notes, no coins — created by a technology called blockchain that has underpinned all the cryptocurrencies and non-fungible tokens (NFTs) that make up the world of digital collectibles ever since.

The first of these cryptocurrencies was Bitcoin. Brought into being by the mysterious figure of Satoshi Nakamoto (probably not one but multiple developers), its aim was to construct a “peer-to-peer version of electronic cash” [that] would “allow online payments to be sent directly from one party to another without going through a financial institution,” as Nakamoto’s original white paper described.[1]

Many believe that such peer-to-peer (P2P) payments have the potential to remove the friction and bias inherent in traditional payment systems, where banks and other intermediaries come between payer and recipient. They can also bring stability to emerging financial networks.

1

IMPROVING FINANCIAL INCLUSION

In sidestepping the dramas of the financial markets, cryptocurrencies potentially have a wider economic role to play. By creating the transparency needed to overcome widespread social trust issues and increasing access to financial services by performing the role of a quasi-bank account, cryptocurrencies have the potential to help alleviate poverty in developing countries and provide a boost to wider economic growth.[2]

In Africa, for instance, where 7.1% of South Africans and 8.5% of Kenyans use them,[3] digital currencies have already found their feet. For the financially marginalized, who find it difficult to open bank accounts and high transaction costs off-putting, crypto is a means to make payments, sending remittances with just a mobile phone and the Internet. Crypto is also appealing to the technically savvy as an investment since it allows them to hold assets that aren’t affected by rising inflation and depreciating local currencies.

And it is as an investment asset that cryptocurrencies are viewed for many, attracted by the potential for significant gain. Indeed, so strong was the demand from both retail and institutional investors that a tsunami of other cryptocurrencies followed in Bitcoin’s wake, launched by fintechs and blockchain start-ups, all trying to differentiate themselves through different value propositions in an ever more crowded market.

The result is seen in the creation of 19,000 cryptocurrencies (compare that to just 180 fiat currencies),[4] with a combined market value of around US $3 trillion by November 2021 and around 18% of Americans and 17% of Europeans said to have invested in some form of crypto-asset.[5] Globally, that figure is even higher, at 23%.[6]

Much of the activity takes place through brokerage platforms, where cryptos are traded for immediate settlement at a spot price. This allows the simultaneous buying and selling of coin. And since there are no barriers to spot market trading, small crypto investors can win (or lose) from high price fluctuations.

Transaction fees tend to be kept relatively low, at 0.1%-0.5% of the trade’s fiat currency value, to attract active day traders. The market leader, Binance, has a flat fee of only 0.1%. Generally, a minimum deposit is required from traders, which can be as much as $50, though Coinbase and Kraken have a $1 minimum.

Other factors that make platforms attractive are the number of currencies traded (50+ at least), along with ease of use. Most crypto-related transactions are done on mobile phones through an app, so ensuring a good user experience is paramount.

And consumers are wanting to do more than simply trade crypto. Increasingly, they are looking for lending and payment services, as well as more sophisticated, riskier options such as cryptocurrency derivatives.

One further element influencing platform choice is location. Given the potential for hacking and theft, local players are often perceived to be more trustworthy, especially if they are regarded as having been properly scrutinized by local or international regulatory authorities. As an example, Austria-based Bitpanda is considered reputable and is chosen by many in Central and Eastern Europe for the offline “cold” wallet storage (where assets are merely stored) it offers.

2

CREATING A WILD WEST

Such is the volatile nature of cryptocurrencies that the market can all too easily enter one of its periodic downturns — what’s referred to as a “crypto winter.” This happened at the end of 2021, when a mixture of adverse macroeconomic conditions and the failure of major crypto projects injected a negative sentiment into the market that is still apparent as we write this Report in the autumn of 2022. The market saw Bitcoin’s price drop 65% from its November 2021 high of $69,000, wiping $2 trillion off the crypto market’s collective worth. Adding to the volatility were large, high-profile purchases and sales like those of Tesla, which in July 2022 offloaded three-quarters of its $2 billion holding in Bitcoin. Previously, CEO Elon Musk had been one of cryptocurrency’s major cheerleaders, with his social media pronouncements often driving surges in trading.

Not surprisingly, risk-averse regulators view such volatility with concern, mindful that the crypto market is bigger than the subprime mortgage market was when it triggered the global financial crisis of 2007-2008. So, when crypto was just an esoteric “topic of interest,” it could be comfortably ignored because traded volumes were light, but that has changed and now it has become a potentially troublesome, heavyweight problem lurking just over the horizon.

In a recent speech, Fabio Panetta of the European Central Bank (ECB) categorized crypto as a “Wild West” investment, describing market activity as a “digital gold rush beyond state control.”[7]

Regulatory authorities like the Basel Committee on Banking Supervision (BCBS) have already signaled their worries that crypto assets might adversely impact banks’ liquidity and risk — market, credit, operational, legal, and reputational — and, consequently, the stability of the entire financial system. Headlines such as “How $60 Billion in Terra Coins Went Up in Algorithmic Smoke”[8] do little other than create a sense that cryptocurrencies are built on shaky ground. The International Monetary Fund (IMF) has commented that: “Crypto-assets are potentially changing the international monetary and financial system in profound ways.”[9]

US Federal Reserve Vice Chair Lael Brainard is someone who has voiced concerns when she said: “It is important that the foundations for sound regulation of the crypto financial system be established now before the crypto ecosystem becomes so large or interconnected that it might pose risks to the stability of the broader financial system.”[10]

And this takes us to the center of the crypto conundrum: regulation. And, most particularly, how much there should be and what form it should take.

Some countries, such as China, Indonesia, and Turkey have banned cryptocurrency transactions outright, citing concerns not just over financial instability but also the use of cryptos for money laundering and terrorist financing. How valid are such concerns? It is difficult to say.

While crypto has long been considered a hotbed of criminal activity, in reality, this could be overstated. Research by blockchain data platform Chainalysis suggested it accounted for under 1% of total crypto activity between 2017-2020.[11] Whether or not this figure is accurate, the truth remains that better know-your-customer (KYC) regulations, periodic reporting, and greater penalties for violations will help dampen bad actor events. This, in turn, will increase trust in cryptocurrencies.

3

CONTROL & MANAGEMENT

Rather than banning crypto, most countries are taking a more pragmatic view by seeking to find ways to better manage its impact. So, driven by Europe, efforts have begun to develop a globally coordinated regulatory approach to crypto assets, improve levels of transparency, and establish new codes of conduct and standards for disclosure and reporting. The Financial Stability Board (FSB), the Basel Committee on Banking Supervision (BCBS), the Committee on Payments and Market Infrastructures (CPMI), the Financial Action Task Force (FATF), and Germany’s Federal Financial Supervisory Authority (BaFin) are some of the key authorities working on the effort.

These discussions tend to focus currently on limiting exposure to unbacked cryptocurrencies and setting specific capital requirements for different types of crypto assets. They also cover areas such as the taxation of crypto assets, strengthening public disclosure and reporting, transparency levels and standards of conduct, as well as anti-money laundering (AML) solutions and combatting the financing of terrorism (CFT).

For the moment, what we are seeing are ad hoc measures being taken by the likes of the Monetary Authority of Singapore, which has said it will broaden its cryptocurrency regulations so more activities are covered.[12] This is in the light of recent failures of various crypto firms with operations in the country.[13]

But there seems to be a growing move toward tighter regulation by governments around the world that are increasingly worried that privately operated, highly volatile digital currencies could undermine their control of financial and monetary systems.

Other nations are now starting to take stronger action against what they see as infringements. As an example, the world’s largest crypto exchange, Binance, was fined $3.4 million by the Dutch Central Bank for operating without authorization in the Netherlands.[14]

There is no doubt that regulation is coming down the line. As Securities and Exchange Commission (SEC) Chair Gary Gensler has pointed out, “Few technologies in history, since antiquity, can persist for long periods of time outside of public policy frameworks.”[15]

The debate will surround the level of regulation that is needed, whether existing rules are being applied, and if the best way to actually supervise the activities of coin issuers is to bring them into the banking system, as some argued in testimony to the US Congress’s House Financial Services Committee in December 2021.[16]

Since then, the US Federal Reserve has issued guidance to banks that might be considering any cryptocurrency activity, making clear that they must notify the authorities of their intentions and make sure that what they are doing is legally permitted.[17] Given the significant fines previously meted out to those considered in contravention of AML, taxation, and consumer protection rules, financial institutions operating in the “gray zone” do so at their peril.

For their part, banks would welcome clear regulations to enable them to move forward with confidence, rather than overstepping the mark or holding back for fear of making a mistake.

Ultimately, there may be no consensus on regulation, with some regions opting to go light on regulation in an attempt to gain economic advantage, or even doing so at a local level. For example, New York City Mayor Eric Adams is intent on transforming the city into a hotspot for cryptocurrency.[18]

So, while strong reservations remain, there is a growing recognition that crypto is here to stay, though as yet only two countries, both small and with no fiat currency of their own, accept crypto as legal tender. The Central African Republic (CAR) started doing so this year, and El Salvador began accepting Bitcoin in 2021.

While it is too early to assess what is happening in the CAR, El Salvador’s Bitcoin experiment is perhaps not going well. Plans to build the world’s first cryptocurrency city have stalled, and the use of cryptocurrency has failed to catch on. One survey shows that just one-fifth of Salvadorans have downloaded the government’s Bitcoin digital wallet (Chivo) and continued to use it after spending the $30 it came loaded with.[19] And while the government has encouraged Salvadorans abroad to send money home through Chivo, only about 2% of remittances between September 2021 and June 2022 were through the wallet.

Despite such apparent setbacks, the government of President Nayib Bukele says its Bitcoin policy has attracted investment, reduced bank commissions to zero, increased tourism, and promoted financial inclusion. In contrast, the IMF says El Salvador should revoke Bitcoin’s status as legal tender because of financial, economic, and legal concerns.

While making privately owned cryptocurrencies legal tender is still a step too far for most countries, many central banks are now exploring the idea of issuing a digital currency that they will regulate: centralized bank digital currencies (CBDC). A survey by the Bank for International Settlements (BIS) found that 81 were developing projects in this area.[20] China is testing a “digital yuan,” while Nigeria has the e-Naira and Jamaica the JamDex.

With over half of the world’s top banks taking a growing interest in cryptos,[21] after years of resistance the tide may be turning. Even BIS, which has always viewed crypto with some skepticism, is saying that it may allow banks to hold up to 1% of their reserves in Bitcoin and other cryptocurrencies.[22]

4

THE CULLING OF THE CRYPTO HERD

Given the sheer number of cryptocurrencies, it is not difficult to predict that very soon there will be a major retrenchment. How many of today’s standard cryptos can have a long-term future when they are neither distinctive nor have any real purpose other than as a speculative vehicle that can be easily manipulated through “pump and dump” schemes that push up prices, enabling those in the know to sell off their coin and let others take the hit as prices fall?

Because major trust issues remain around crypto, investors may well gravitate toward top-tier currencies that are seen as more reliable or having something extra to offer. This will lead to a game where whoever is left behind loses, as lower layers of stragglers fall by the wayside either through lack of demand (they don’t have the ease of use or level of features sought by users and investors) or from the tightening of regulations that hit those who take too many risks.

Eventually, we are likely to see the majority of cryptos disappearing from the market, leaving perhaps just 30 to 50 ”winners” still standing, regarded as trustworthy, reputable, or reliable by investors. Among the survivors will presumably be the original Bitcoin, still a dominant force, though its position has been diluted by the arrival of so many other cryptos — as of early November, it has less than 40% of the market, according to CoinMarketCap, much lower than the 70% of early 2020. Ethereum, the other big player in the space, had about 18.8% of the crypto total market capitalization at the same time.

Some may survive because they have a well-established local or regional following or because they are ”stablecoins” like Tether and US Dollar Coin, which are backed by a fiat currency and are favored because they are seen as less risky. However, some of these may be stable in name only, since not all issues are supporting their coins with real fiat currency in a bank or are held as they should be. This means there is potential for a run on stablecoins. As the President’s Working Group on Financial Markets observed in its November 2021 report, stablecoins are too big to ignore, but not yet too big to fail from a systemic risk point of view.[23]

We had a small taste of the market’s fragility with the crash of TerraUSD and the subsequent knock-on effects that saw its sister coin, Luna, also fail.[24] This took the market by surprise, since Terra was a stablecoin pegged to a fiat currency (in this case, the US dollar). But at the time of writing, having maintained almost exact parity with the dollar since its release, Terra is worth just $0.00025 (€0.00025). With TerraUSD losing its peg to the dollar, it seems that stablecoins may not be quite as stable as might be believed.

As Steven Maijoor, Executive Director of Supervision, Dutch Central Bank (De Nederlandsche Bank), said in February 2022, “Perhaps the most fundamental question is this: in a system where so many new, previously non-financial players are becoming instrumental in offering financial services, how are we, as financial supervisors, going to ensure that the financial system remains robust and consumers stay safe? How can we make sure that we continue to have the right mandate and effective instruments to ensure that outcome?”

Though not connected to the Terra Luna fallout, there is also the case of Nuri Bank, a crypto-focused digital bank in Germany that recently became insolvent. While the company blamed “significant macroeconomic headwinds” arising from COVID-19 and Russia’s invasion of Ukraine, plus the “cooling down of public and private capital markets,” the primary reason was the bankruptcy of Celsius Network, one of the leading decentralized finance (DeFi) platforms, which had serious knock-on effects in the crypto sector.[25]

Cryptocurrency lender Celsius also crashed in July 2022, with some declaring that this had all the makings of a scam. Paul Romer, a Nobel prize-winning economist at New York University, said that the high interests Celsius had been able to offer “were pure Bernie Madoff,” the American fraudster convicted of running the world’s largest Ponzi scheme.[26]

All this has contributed to a crypto bear market.

DISSECTING THE CRYPTO VALUE CHAIN

The cryptocurrency chain is complex and far-reaching, stretching out as it does across society and the real economy, and involving various regulatory bodies and many different players in multiple marketplaces.

Looking in more detail at who occupies this space, it becomes clear that there is not a decentralized system as it is so often portrayed, given that the crypto infrastructure is actually in the hands of relatively few companies. Figure 1 illustrates the different tiers of players that together make up the crypto environment.

The network tier

-

Developers — create blockchain and software solutions that provide the crypto community with the technical capacity it needs (e.g., Idealogic, Lotus Soft, Blockcypher, Eva).

-

Miners — solve the complex algorithms required to generate new bitcoins and other cryptocurrencies (e.g., Bitfarms, Canaan, BitMain, Bitfury).

-

Node operators — run the high-performance infrastructure that validates any new blocks written to the blockchain and then broadcasts them to the rest of the network (e.g., Polygon, Nyala, Tendermint, Etherscan).

The infrastructure tier

-

Tool creators — provide ancillary software for blockchain testing (e.g., Solidity, Ethereum Geth, Truffle).

-

Storage solution providers — help to organize and share blockchain-secured data (e.g., Fluree, BitTorrent, PermaBot, Arweave).

-

Authentication services — maintain the distributed networks that underpin the blockchain ecosystem (e.g., Cambridge Blockchain, Civic, ShoCard).

-

Smart contract providers — programs automate the execution of agreements on the blockchain (e.g., Evercode Lab, Fox IT, Ava Labs, Cygnet Infotech).

The marketplace tier

-

Exchanges — where crypto can be traded for both conventional fiat currencies and other digital coins. These include more traditional institutions such as the Stuttgart Stock Exchange, which provides a crypto infrastructure for banks (as well as companies like Kraken, Coinbase, Binance, Bitbuy).

-

Over-the-counter (OTC) trading firms — the fintechs that enable buyers and sellers of crypto to trade outside a regular exchange (e.g., Bitpanda, Bitcoin Suisse, Coinify).

-

ATM — automated teller machines where Bitcoin and other cryptos can be bought using cash or a credit card (e.g., Kurant, General Bytes, Genesis).

The players tier

-

Trading companies — provide services to facilitate the buying and selling of cryptocurrencies (e.g., Deribit, Paxos, Maple, Bitfinex, Amber, FirstCoin.de).

-

Custody firms — offer users a secure location to store and manage their digital assets (e.g., Gemini, Fireblocks, Ledger, NYDIG, Metaco, Tangany).

-

Lending companies — allow you to lend and borrow against your digital assets (e.g., BlockFi, CoinRabbit, Nexo).

-

Payment service providers — enable the spending of cryptocurrencies (e.g., BitPay, CoinGate, MoonPay, Veem).

-

Asset management firms — dedicated to managing portfolios of digital assets (e.g., Pantera, Galaxy, Wave Financial, Bitwise).

The end users

-

B2C — major companies that have begun to accept crypto for purchases (e.g., Microsoft, The Home Depot, KFC, Overstock).

-

B2B — providers of crypto-friendly banking accounts (e.g., Bankera, B2Bpay, Zerocap, Elastic Path).

5

HOW SHOULD BANKS ADAPT?

So how should financial institutions position themselves in this new environment where crypto is increasingly legitimate, and in what areas should a bank choose to play? That is very much down to the individual institution, its appetite for risk, and its specific take on the market’s point of arrival.

It could, for instance, eschew this whole area and remain outside the crypto playing field altogether, leaving others to serve the market. If the market doesn’t stabilize and crypto’s reputation continues to be trashed by highly volatile price swings, then this principled approach may be a sensible one. However, it does seem to cut across the direction of travel.

Or an institution can assume that it will enter the market at some point, just not right now. Playing the “wait and see” game is a pragmatic solution, though it could leave one having to play catch-up in a fast-moving marketplace.

Alternatively, financial players could dip test the waters by providing a limited range of crypto services, enabling their customers to participate in the market without actively engaging themselves.

They might, for instance, provide crypto custody services to store digital assets and digital wallets that have a shareable public address, like the IBAN of a bank account, with a private digital key used by the account holder to control access. Cryptocurrency custody has become a highly active area, with 73 new services launched in 2021. Players in this segment now include US Bancorp, Bank of New York Mellon, Deutsche Bank, BNP Paribas, JPMorgan Chase, and HSBC.

However, offering a cryptocurrency custody service is not without risk. While providing offline “cold” wallets, where assets are merely stored is one thing, any bank offering a “hot” wallet that is connected to the Internet and used for trading or payments has to be strongly secured against high-level hacks and thefts. The recent illegal siphoning of $190 million in cryptocurrencies from US crypto firm Nomad clearly demonstrates what can happen, especially when you are the target of well-organized bad actors.[27]

North Korea, for example, has made stealing cryptocurrency part of its strategy to mitigate the country’s financial isolation. In the first half of 2022, crypto-research firm Chainalysis calculated the regime had already stolen over $840 million, mainly from decentralized financial platforms.

There are also unpredictable risks over which you have little influence, such as a bug in a layer 1 protocol (the blockchain layer), which then disrupts the cryptocurrencies and smart contracts that are built on it.

If that were not enough, there are decisions to be made about which cryptocurrencies to support, because that will have a big impact on the IT infrastructure required. If you don’t want to have to change that infrastructure too frequently, you need to be picking “crypto winners.” And that is not easy to do — an infrastructure that would have supported the top 10 cryptocurrencies five years ago would only be capable of supporting three of them today.

Because of this volatile market situation, any organization offering crypto-related products or services must have an IT infrastructure that can react fast and respond flexibly to market changes. And to do this, organizations must be aware of not just factors that impact them directly, but also events and circumstances affecting others they may be connected with. An investment in or collaboration with company A, for instance, could leave you unexpectedly exposed if you are unaware they are heavily invested in Bitcoin, and the crypto market turns. The situation becomes even more opaque if company A is involved with company B, which also has cryptocurrency holdings. Such interconnectedness means additional due diligence is required to identify potential risks.

And unlike most other digital transactions between banks, cryptocurrency transactions are nonreversible, which means that often very little can be done to recover any money. We may have a wealth of knowledge about how to protect physical assets, but measures to keep cryptocurrencies secure are still in their infancy.

Besides crypto custody, more banks are beginning to expand their portfolio of services to include crypto-asset trading. Goldman Sachs was one of the first major US banks to offer OTC trades, while Citigroup is looking to offer Bitcoin futures trading for some institutional clients, dependent on regulatory approval. Even those considered traditional banks are becoming involved. Italy’s Banca Generali, for example, has teamed up with Italian-American cryptocurrency exchange Banca Generali Conio, enabling customers to use an app to buy cryptocurrencies through their regular banking account.

And French fintech Lydia has partnered with the Austrian investment start-up Bitpanda so that its 5.5 million users can now invest in cryptocurrencies, while London-based Revolut is looking to set up an in-house crypto-exchange platform and launch its own token.

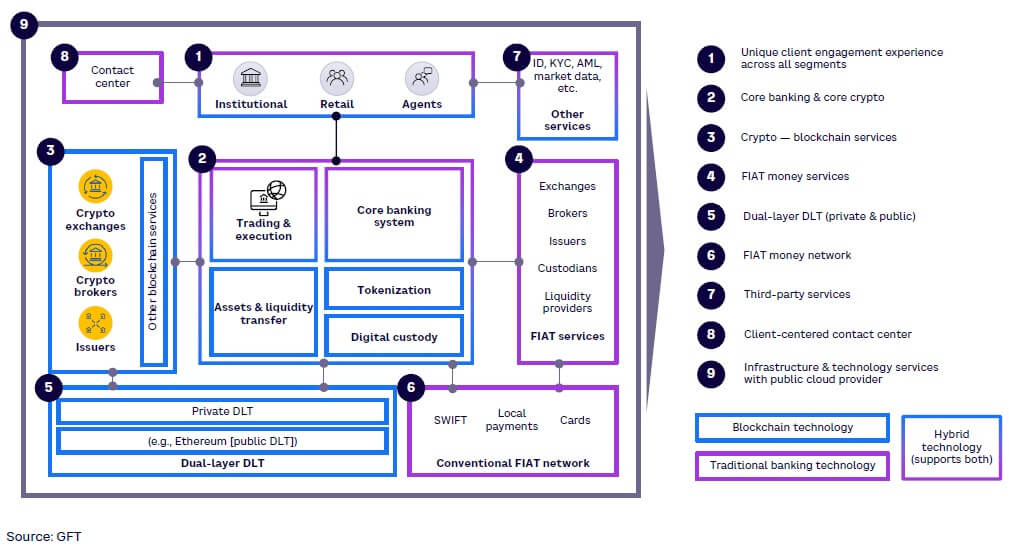

Financial institutions that decide to hold cryptocurrencies as assets, provide crypto-based products, or offer crypto-custody services to other institutions will need to revise their operating model to meet regulatory requirements.

Institutions offering cryptocurrency as an asset will need to ensure they have sufficient liquidity and are able to store and transfer assets safely. As a digital custodian, they will also need to be confident that their current AML and KYC capabilities remain compliant for cryptocurrencies. They may have to modify their software ecosystem and processes accordingly.

The illustration of a target operating model of a crypto bank in Figure 2 shows that the main architectural changes required will revolve around connectivity to public or permissioned blockchains, and to other services such as crypto exchanges, as well as crypto brokers and issuers.

Further key, critical changes will be needed to core banking software, where additional applications will be required for functions such as digital custody and tokenization.

There are also potential opportunities in crypto lending and borrowing. Under a crypto-lending model, private investors receive interest payments for allowing lenders to use their cryptocurrency to make loans to institutional and corporate borrowers. Though interest rates vary widely between lending platforms, with each lender having different rates for different coins, typically these fall between 3% to 8%. However, rates for stablecoins are generally higher, at between 10% and 18%.

This is a very fast means of financing — transactions happen within a matter of hours — with much potential for customization of terms. On the flip side, by crypto borrowing, private investors can take out a loan secured against their crypto holdings, usually capped at 50% of asset value.

And since professional investors and high-net-worth individuals hold almost two-thirds of the Bitcoin supply, providing a wealth management service that encompasses crypto assets would be of obvious benefit to banks. However, their wildly deviating prices mean cryptocurrencies must be regarded as a high-risk investment that much like commodities needs to be actively traded, rather than considered a stable store of value that just needs to be managed. Morgan Stanley, Wells Fargo & Co, and Goldman Sachs are just a few of those already in this space.

6

THE FUTURE OF CRYPTO

Gazing into a crystal ball is fraught with uncertainty at the best of times, but particularly so when it comes to the future of cryptocurrencies. But that should not stop us from asking questions about the direction of travel and what the implications might be for financial institutions.

IS CRYPTO HERE TO STAY?

It very much seems so. Even as the market undergoes a crypto winter, venture capitalists (VCs) are looking to pour money into digital currency and blockchain start-ups. Data from PitchBook shows that VCs invested $17.5 billion in such firms during the first half of 2022, which means that the $26.9 billion raised in the whole of last year is likely to be surpassed.

North America has been a particular hotspot, where in contrast to the downturn in VC activity generally, in the six months to June 2022 about $11.4 billion flowed into crypto-related start-ups, not far behind the $15.6 billion for the whole of 2021. VC investment is also strong in Europe, with $2.2 billion in funds raised in the first half of the year.

The financial services sector is increasingly enthusiastic about cryptocurrency applications and the blockchain technology that underpins them — some estimate that around 30% of investment banks’ infrastructure costs could be stripped out by using blockchain.

The market for blockchain in banking and financial services is expected to reach $12.39 billion in 2026, up from $1.17 billion in 2021, a CAGR of around 60%.[28]

WILL CRYPTOCURRENCIES BE PRIMARILY FOR PAYMENTS?

At the moment, cryptocurrencies are generally considered an investment rather than a vehicle for payments. However, there is a widespread belief that they offer great potential as a means to improve financial inclusion in countries that don’t have cheap and easy-to-use banking systems. The World Economic Forum, for instance, advocates the use of blockchain technology and cryptocurrencies to help create more open and democratic financial systems.[29]

Crypto could, for instance, help people transact without the need for intermediaries, which would be of real advantage to the many around the world who do not have bank accounts and depend instead on checks, money orders, and cash. With some 1.7 billion people in the world today considered “unbanked,” according to the World Bank — which means as many as six out of 10 adults in some countries — cryptocurrencies are a way to promote financial inclusion. Cryptos are already regular means of payment in Vietnam, India, and Pakistan.

Cross-border payments to other countries have traditionally been expensive, operationally complex, and may take up to several days to be credited. However, international payments could be made simpler and cheaper by embracing crypto and blockchain solutions. So, rather than having to wait days for payments to be credited, as happens for instance between EU and non-EU countries, by using Ripple’s XRP Ledger, banks could not only achieve operational advantages but also be able to offer customers low-cost, real-time transfers.

Where banking systems are more developed, there are further opportunities, such as programmable payments that are executed automatically when certain conditions are met. This type of payment already exists in the form of standing orders and direct debits. However, far more complex business processes could be embedded into automated payments by using blockchain technology and smart contracts.