Virtualizing mobile networks

The silver bullet for operators to master 5G?

Executive Summary

Around the globe, achieving today’s customer demands of super-high throughput and ultra-low latencies requires rethinking traditional mobile network architectures. Monolithic telecom infrastructure based on proprietary hardware and closed interfaces has failed to provide the flexibility, scalability and degree of automation that is required in the era of 5G.

Technology developments in the fields of hardware and software disaggregation, network function virtualization and containerization allow for radical architectural changes across mobile network domains. Yet, to fully reap the benefits of network virtualization, telco operators need to rethink sourcing and deployment models as well as corresponding organizational setups.

This report is the first in a series of publications targeted at addressing the issues telco organizations face in deploying their virtualized mobile networks. Here, we focus on the general concept of virtualization and its application to the mobile network domains. In subsequent publications, we will tackle the strategic questions of sourcing and organizational models related to these deployments.

1

Why are new mobile architectures needed and why now?

Today’s mobile networks are in a constant race to keep up with growing demand in coverage, capacity and customer experience (CEX), while average revenues per user are shrinking (or stagnating in the best case). In the era of 5G, these demands are summarized in clearly defined requirements for use cases in ultra-reliable low-latency communication (URLLC) and massive data flow (enhanced mobile broadband [eMBB] and massive machine-type communication [mMTC]) connections. Demands are further magnified by the emergence of new network services such as end-to-end slicing and mobile private networks.

Achieving these objectives requires rethinking traditional mobile network architecture. Monolithic telecom infrastructure based on proprietary hardware and closed interfaces does not provide the flexibility, scalability and degree of automation that mobile players increasingly need. Hence, novel (for the telecom sector, yet not ICT as a whole) architecture concepts are taking hold. These include:

- Edge and far-edge data center (DC) infrastructure – Deployment of virtual network functions (VNFs) close to the customer reduces latency, improving quality of experience (QoE); enables higher security (especially for mission-/safetycritical applications); and provides local data termination to relieve backbone network traffic.

- Disaggregation of hardware (HW) and software (SW) – Unbundling of HW and SW (i.e., using commercial offthe-shelf compute storage and networking hardware) is nothing new, yet it only recently gained general exposure across networking equipment (especially in radio access networks [RANs]) to enable CAPEX reduction and sourcing diversification.

- “Softwarization” and virtualization of network functions – End-to-end software-defined networks (SDNs) allow for the scalability and automation required for future 5G use cases.

- Open interfaces – Standardization of application programming interfaces (APIs) between, as well as within, network domains allows for vendor competition, hence innovation at lower total cost of ownership (TCO).

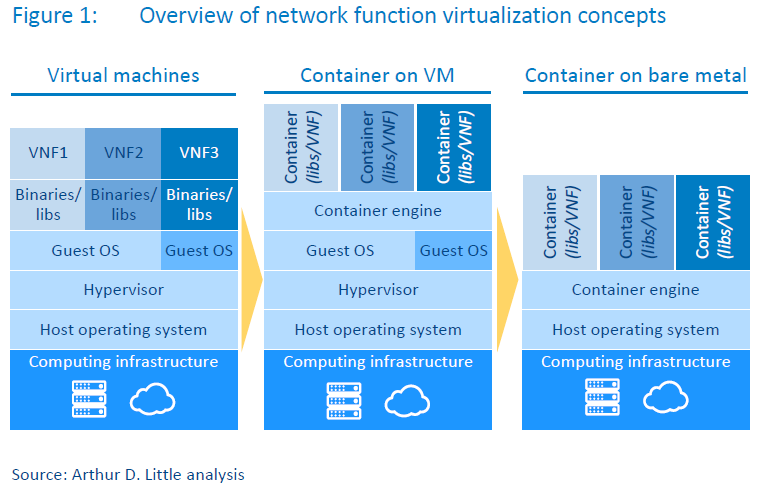

- Containerization of software – Moving from dedicated servers and virtual machines (VMs) to containers on “bare metal” (i.e., running VNFs on a significantly reduced stack) to further increase efficiency and hardware usage and to drive scalability of the network (see Figure 1).

Although some of these trends have been around for some time, we now see three key market trends acting as catalysts for the large-scale adoption of these technologies in the near future:

- Interoperability of vendors within and between the individual network domains (RAN, transport, core and orchestration) is developing at a rapid pace based on standardizations such as Open RAN (O-RAN Alliance).

- As a consequence of this expansion, the vendor landscape has drastically broadened, leading to the availability of competitive solutions for all network domains on the market, thereby fostering a clear paradigm shift of traditional as well as “new” network equipment providers (NEPs) to move from monolithic telecom network infrastructure to softwarebased IT solutions.

- We consider integration efforts and risk for decoupled and disaggregated solutions to be reasonable given expected network TCO savings of up to 40 percent and the establishment of an ecosystem of suitable integration partners.

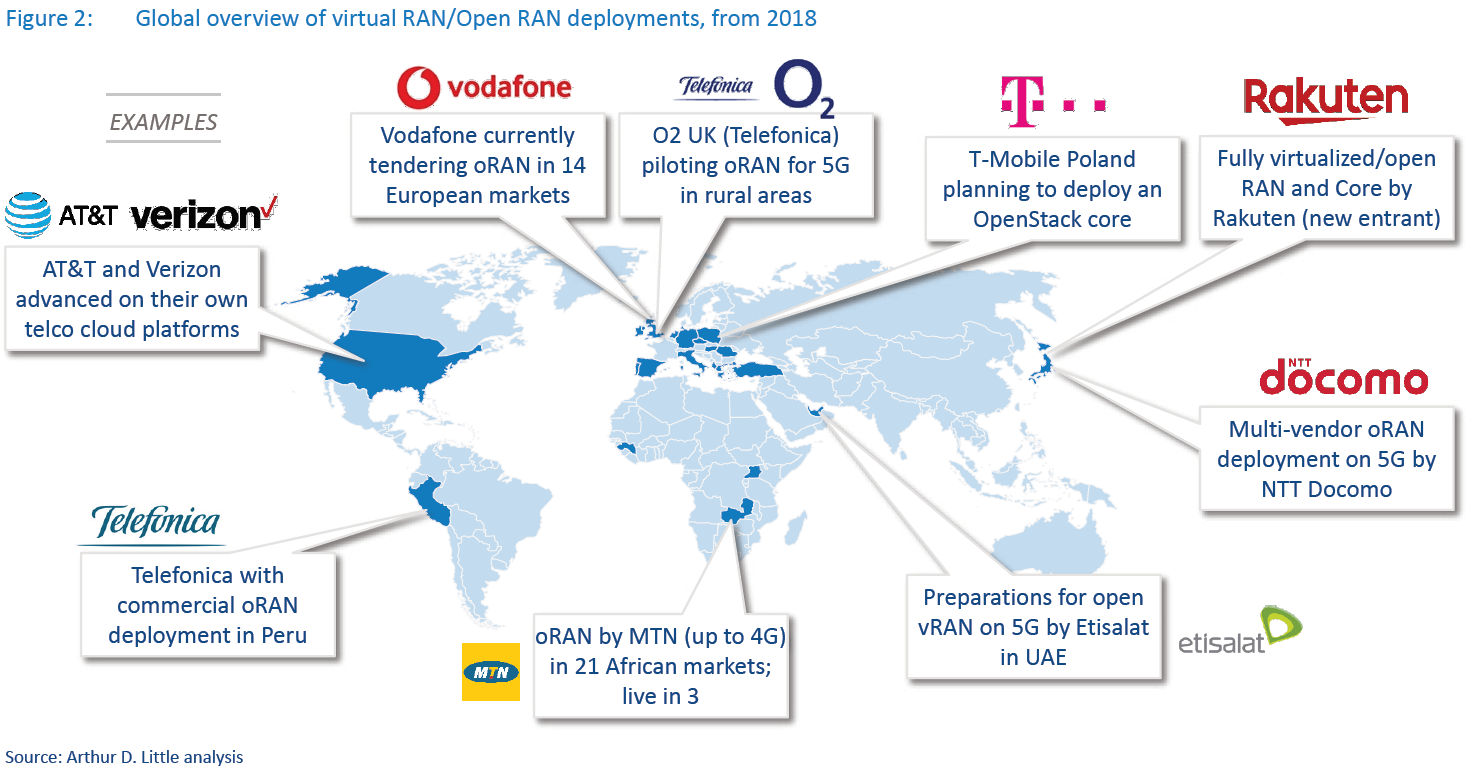

Leading operators across the globe have already taken the first steps toward these target networks, as illustrated in Figure 2.

Although virtualization concepts and subsequent target network architectures remain at an early stage of development, the first live deployments – such as those by Rakuten in Japan, AT&T in the US or Telefonica in selected markets – clearly indicate performance improvements over distributed/centralized network architectures across domains.

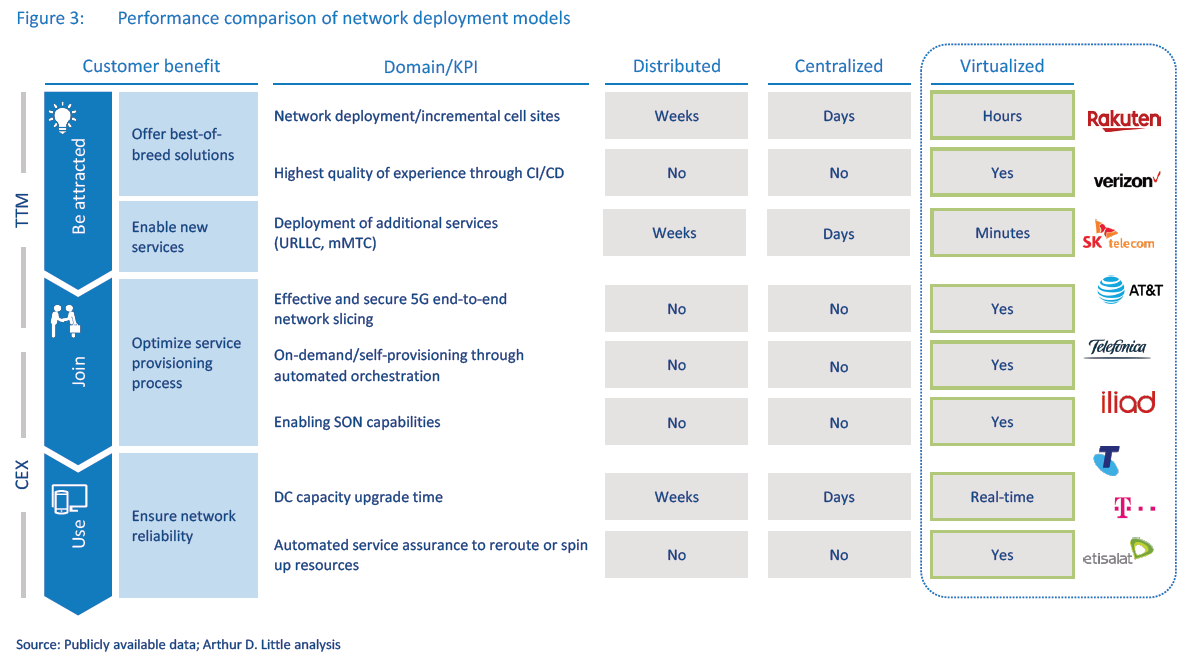

As an example of these improvements, time to market (TTM) for incremental network deployments (mobile sites) as well as for new 5G services such as URLLC or mMTC can be reduced from the current requirement of several days to just a few hours.

Moreover, virtualization and cloudification allow organizations to provide better QoE through continuous integration (CI)/ continuous delivery (CD) and fully automated self-provisioning and self-optimizing network (SON) functions. Figure 3 compares key performance metrics between distributed, centralized and virtualized network deployment models along the customer journey.

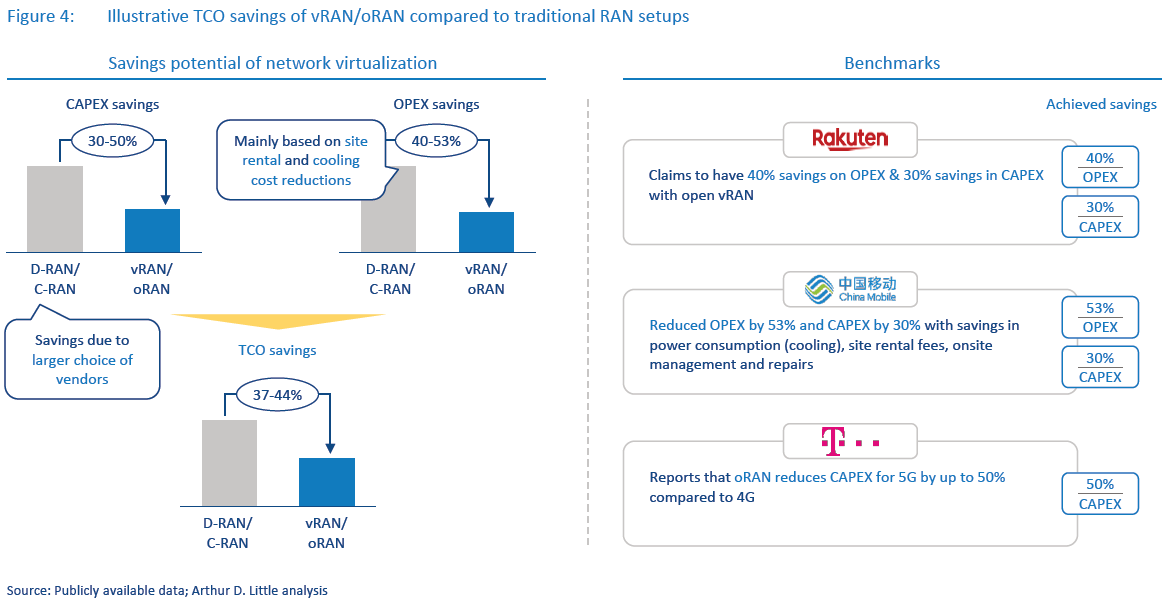

With a broadening vendor landscape, higher interoperability and performance improvements along the customer journey, operators such as Rakuten, China Mobile and T-Mobile US that deploy virtual RAN (vRAN)/Open RAN (oRAN) solutions realize network TCO savings of up to 44 percent compared to traditional distributed/centralized RAN setups (D-RAN/C-RAN).

Whereas CAPEX can be reduced by up to 50 percent due to vendor competition across domains, OPEX savings of up to 53 percent mainly come from efficiencies in deployment and operations, such as zero-touch automation (see Figure 4).

2

How can virtualization be executed across network domains?

To realize the benefits of virtualization, organizations must revisit mobile network architectures across domains and explore the organizational changes and alterations of traditional sourcing models that are required. Next, we outline the key concepts for main mobile network sections.

Radio access network – achieving openness through virtualization

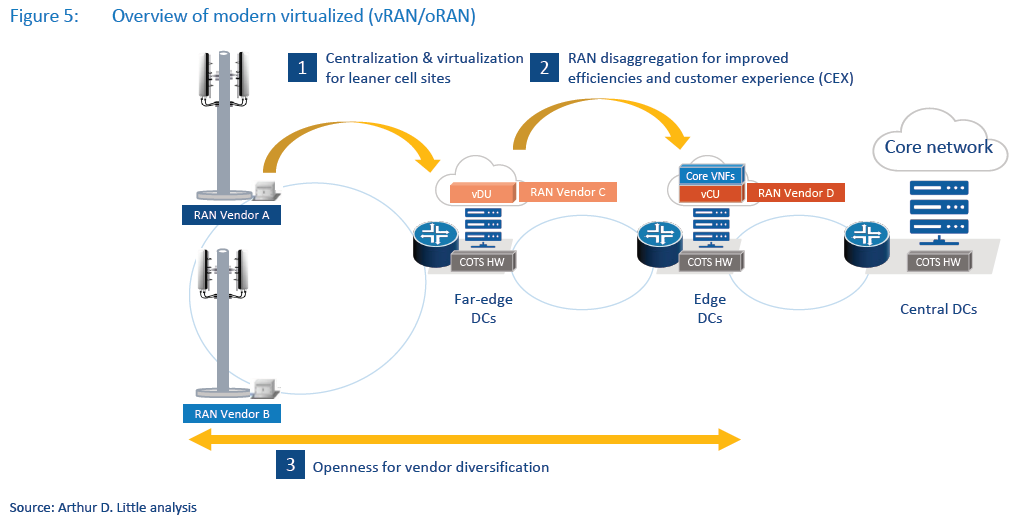

RAN assets are typically the largest investment for the mobile network and are the most rigid and costly to operate and transform. Thus, it is vital that they are made increasingly agile and more cost-efficient. The evolution we see in RAN includes centralization, virtualization and openness (see Figure 5):

- Centralization and virtualization for leaner cell sites.

- RAN disaggregation for improved efficiencies and CEX.

- Openness for vendor diversification.

Centralization and virtualization for leaner cell sites

Avoiding dedicated baseband units (BBUs) at each site allows mobile operators to create centralized BBU pools, driving leaner cell sites that are easier to deploy and maintain. This is a key driver for lowering CAPEX by reducing individual cellsite requirements for shelter and cooling, and the nascent operational effort to maintain equipment-heavy cell sites, as opposed to fewer, centralized locations.

RAN disaggregation for improved efficiencies and CEX

BBUs are shifting from a physical toward a virtual resource and can be further split into virtual distributed units (vDUs) and virtual centralized units (vCUs). Virtual BBU (vBBU) resources can ultimately be more efficiently allocated, increasing average equipment utilization as a lever to reduce necessary CAPEX and improving CEX by reducing the risk of congestion. Virtualization also enables scalability, automaticity and faster adoption of changes (updates or vendor swaps).

Openness for vendor diversification

RAN virtualization facilitates the implementation of open interfaces (oRAN), leading to use cases, such as deploying separate vendors for active antenna units (AAUs) and vBBUs (or vCUs and vDUs), using commercial off-the-shelf (COTS) hardware for vRAN software, or mixing different RAN vendors within the same geographic footprint. Such a multi-vendor setup allows organizations to leverage best-in-breed solutions for each network component while lowering RAN CAPEX through increased vendor competition and reduced reliance on proprietary hardware.

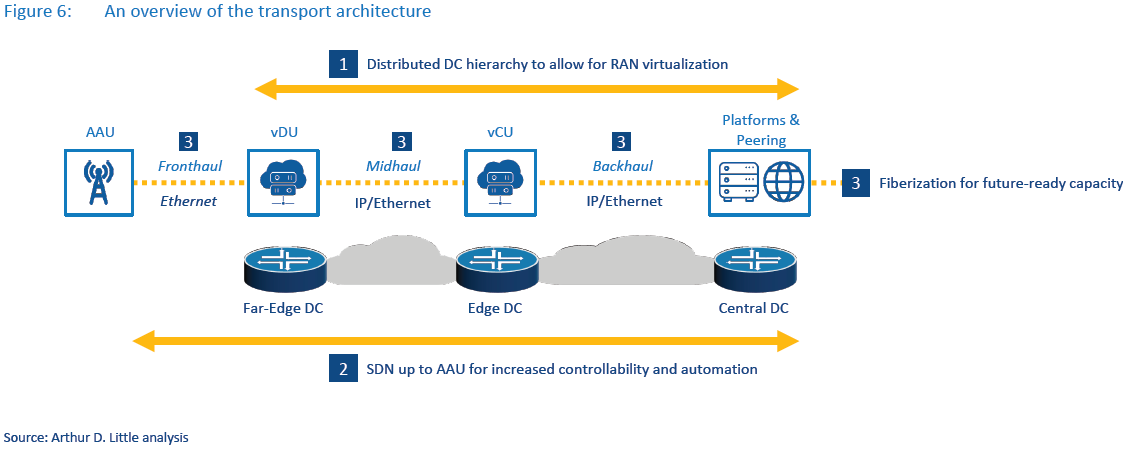

Transport – DC hierarchy and new protocols to enable virtualization

Virtualization and disaggregation of RAN architecture necessitates rethinking how transport and DC infrastructure is deployed and operated (see Figure 6). The evolution for mobile operations includes:

- Distributed DC hierarchy to allow for RAN virtualization.

- SDN up to active antenna units (AAU) for increased controllability and automation.

- Fiberization for future-ready capacity.

Distributed DC hierarchy to allow for RAN virtualization

RAN centralization and virtualization entails cloud infrastructure at the edge. This opens an opportunity for companies to offer latency-sensitive use cases, such as autonomous driving, interactive augmented reality/virtual reality and holographic communications. To achieve this, hundreds, if not thousands, of mini-DCs must be deployed closer to the user. While the buildout effort and change in operating model of the DC infrastructure may seem significant at first, the effort is a fundamental step to unlocking large TCO savings from open and virtualized RAN, as well as to increasing differentiability with better QoE and available services.

As an example, whereas in a classical D-RAN concept each cell site has a dedicated BBU, in a centralized and virtualized network multiple BBUs are consolidated into centralized far-edge DCs and hosted as VNFs, eliminating significant amounts of remote equipment, located on the site, and thereby reducing the overall equipment required, as well as associated maintenance efforts.

The distributed DC infrastructure would also be shared as the basis for all necessary network intelligence coming from RAN, core or other telco domains (e.g., content delivery networks, multi-access edge computing or fixed service).

SDN up to AAU for increased controllability and automation

As a result of RAN virtualization, two new transport domains emerge – fronthaul and midhaul – in addition to the regular mobile backhaul. The Common Public Radio Interface (CPRI) protocol to connect AAUs and BBUs is ill-equipped for larger fronthaul distances. Instead, new eCPRI and IEEE-defined protocols, running on Ethernet, are necessary. To ensure competitive quality of service despite growing user traffic and end-to-end orchestration, operators – and vendors – need to extend SDN controllability and automation to fronthaul transport.

Fiberization for future-ready capacity

The traffic and latency requirements of current and future 5G use cases demand a rapid increase in fiberization to cell sites. While fiber is a heavy investment, it ensures long-term capacity of the transport medium (unlike microwave, which requires frequent upgrades). Operators can approach fiber investment in an intelligent way by decreasing fiber usage per site, either at the level of transport equipment (WDM or L2/L3 switches) or at an architectural level via “ring-structure” of the fronthaul transport as opposed to the typical “star”-shaped structure of current backhaul. This approach will significantly reduce upfront investment into backhaul transport, while ensuring enough capacity to deliver user traffic demand and quality of experience. With an average of around 35 percent of TCO across most recent 5G deployments, fiberization of cell sites will remain a key investment driver for any operator.

Core - distributed VNFs for critical 5G use cases

The core network is increasingly becoming disaggregated, virtualized and distributed, enabling a more agile, efficient and performant network that enables 5G-promised use cases. This is mainly driven by three key factors:

- Microservice-based architecture for critical 5G use cases.

- Containers on “bare metal” for further efficiency.

- Transition to distributed core systems.

Microservice-based architecture for critical 5G use cases

Especially in the context of URLLC and mMTC, organizations must tailor services to specific use cases. To enable these differentiated services, network functions in the packet core will be decoupled into individual microservices. Operators can enhance the quality of service by catering to the demand of each use case, while at the same time optimizing the usage of network resources.

Containers on “bare metal” for further efficiency

Moving toward a microservices-based architecture requires more scalability and simplification in the orchestration of the packet core. Hence, an evolution toward containers on “bare metal” will be an inevitable step. Containerization allows core VNFs to scale-in faster and in a more cost-efficient way (compared to VMs) by significantly reducing the required underlaying physical resources and time.

Transition to distributed core systems

The combination of two trends – microservices and containerization – will allow operators to move from a centralized toward a distributed core network. The latter means dynamic and real-time deployment of microservices anywhere in the network, based on the distinct requirements of a service provided to a specific customer. Automation will allow the customer to directly initiate these services, enabling selfservice, mass customization and faster provisioning.

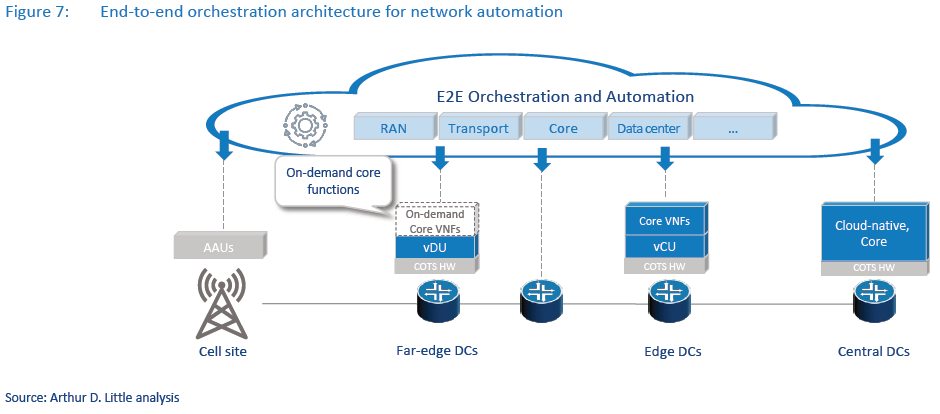

Orchestration and automation – moving toward “zero-touch” operations

Last but not least, to achieve a design that meets operators’ business objectives, the target mobile network architecture requires advancements in automation and end-to-end orchestration. Specifically, we see the following three key trends driving end-to-end automation and orchestration (see Figure 7):

- Integration of separate domains to a single orchestration system.

- From rule-based to artificial intelligence (AI)-based orchestration.

- Self-provisioning of services for full automation.

Integration of separate domains to a single orchestration system

Current network operations are based on configuration and monitoring of separate systems – or “silos” – that must be patched together to achieve automation and end-to-end service provisioning. Hence, future networks will move from this isolated approach toward achieving true orchestration. The journey requires initially combining various systems into “domains” (e.g., mobile and transport) and eventually achieving cross-domain orchestration via open APIs. This cross-domain orchestration will enable not only a path to true automation, but also the necessary capabilities for complex and dynamic services, such as network slicing, while maintaining the necessary quality of service across heterogenous underlying network systems.

From rule-based to AI-based orchestration

Current automation is typically achieved via pre-established templates of configurations or, in the best case, rule-/policybased automation. These types of automation often face a mismatch between the goals and results of the rule or template, requiring additional manual adjustments. Closed-loop automation would feedback from the results of actions and selfadjust to achieve a target result (e.g., service quality) rather than a target action.

Telcos’ end goal is “zero-touch” operations, enabling significant OPEX reductions and better real-time optimization of network performance. AI is a necessary tool to achieve the degree of automation that is required. Presumably, only AI-supported systems would be able to navigate the complex relations of network components. Without AI, it is unlikely that organizations can achieve the dynamic service orchestration and scaling at the network’s edge or network slicing.

Self-provisioning of services for full automation

With this level of automation, our understanding of connectivity provisioning will shift to service-centric orchestration, which allows for automated provisioning of on-demand services triggered and configured directly by the customer. Selfconfiguration enables a whole new playing field for operators around differentiability, tapping into new customer segments and further optimization potential across other commercial or technical company units. Customer-facing self-service portals, enabling customer-defined service parameters at low production cost and fast deployment, will be a new differentiator enabled for early adopters and a basic expectation in the long run.

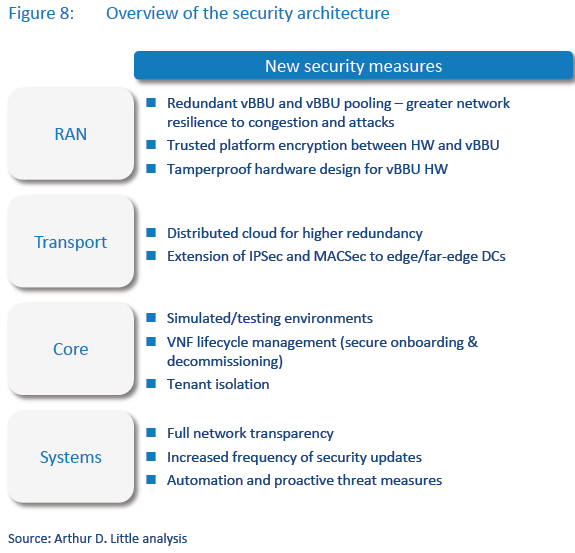

Network security – increased protection through trusted platforms and tenant isolation

Virtualization fundamentally changes the risk profile of mobile networks. Whereas in physical networks the largest security threat came from an “arms race” of malware with increasingly professionalized “toolkits,” virtualization exposes network functions to IT security threats that have not been present before. Moreover, the usage of COTS hardware prevents vendorlevel security encryption (a trusted execution environment), and multi-tenant use of physical infrastructure (i.e., slicing, third-party apps) creates risks for security “backdoors” between different security grade systems.

Yet along with the emergence of network function virtualization, preventive security measures are improving as well. Concepts such as trusted platform encryption between HW and vBBU and tamperproof hardware design for vBBUs have significantly improved security levels in the RAN domain. In addition, the extension of IPSec and MACSec to edge and far-edge data center locations has provided further protection to the transport network. Tenant isolation and full network transparency, among others, elevate security levels in the core and systems domains (see Figure 8).

Conclusions

With changing customer requirements and increasing competition, now is the time for telcos to transform their mobile networks. Telecom operators should make use of new technologies to transition from legacy network architecture to a flexible, virtual, open and automated network that is more resilient and programmable, enabling adjustment in the face of unforeseen future market demands.

Time will tell if telcos can achieve such a transition while managing the migration effort efficiently. It is our strong belief that such a shift requires not only significant financial and operational investment but also a transformation in the organizational setup and capabilities. Telcos will no longer be able to source and operate in their usual mode of plan – build – run. In particular, this transition will have two major impacts on organizations:

- Telco operators must rethink their sourcing strategy. Disaggregation of hardware and software in combination with subsequent network function virtualization allows for moving toward greater vendor diversity and ultimately raises the strategic question of whether to buy pre-integrated solutions from traditional network equipment providers or to source highly specialized IT-based solutions from upcoming “new kids on the block” vendors. To answer this question, operators must weigh cost and risk profiles versus openness, agility and innovativeness of their target network designs.

- Mobile operators will no longer be able to work in separate silos (e.g., with isolated teams for RAN, transport, core and systems). Rather, organizations will have to establish a “network architecture” team responsible for the orchestration of the entire network and to increase cross-segment coordination. Moreover, telco operators will need to broaden the technical capabilities of their network teams. These include those competencies associated with IT in order to orchestrate the cloudification of all network segments and establish new, iterative cycles of working as opposed to rigid plan-build-run cycles.

In our 2019 report “Who Dares Wins!” Arthur D. Little covered how CxOs, as well as operational and commercial teams, can address some of the challenges of virtualization. In subsequent articles in this series, we will explore these implications in more detail and share best practices of mobile network operators from around the globe that have embarked on this journey. Stay tuned!

DOWNLOAD THE FULL REPORT

Virtualizing mobile networks

The silver bullet for operators to master 5G?

DATE

Executive Summary

Around the globe, achieving today’s customer demands of super-high throughput and ultra-low latencies requires rethinking traditional mobile network architectures. Monolithic telecom infrastructure based on proprietary hardware and closed interfaces has failed to provide the flexibility, scalability and degree of automation that is required in the era of 5G.

Technology developments in the fields of hardware and software disaggregation, network function virtualization and containerization allow for radical architectural changes across mobile network domains. Yet, to fully reap the benefits of network virtualization, telco operators need to rethink sourcing and deployment models as well as corresponding organizational setups.

This report is the first in a series of publications targeted at addressing the issues telco organizations face in deploying their virtualized mobile networks. Here, we focus on the general concept of virtualization and its application to the mobile network domains. In subsequent publications, we will tackle the strategic questions of sourcing and organizational models related to these deployments.

1

Why are new mobile architectures needed and why now?

Today’s mobile networks are in a constant race to keep up with growing demand in coverage, capacity and customer experience (CEX), while average revenues per user are shrinking (or stagnating in the best case). In the era of 5G, these demands are summarized in clearly defined requirements for use cases in ultra-reliable low-latency communication (URLLC) and massive data flow (enhanced mobile broadband [eMBB] and massive machine-type communication [mMTC]) connections. Demands are further magnified by the emergence of new network services such as end-to-end slicing and mobile private networks.

Achieving these objectives requires rethinking traditional mobile network architecture. Monolithic telecom infrastructure based on proprietary hardware and closed interfaces does not provide the flexibility, scalability and degree of automation that mobile players increasingly need. Hence, novel (for the telecom sector, yet not ICT as a whole) architecture concepts are taking hold. These include:

- Edge and far-edge data center (DC) infrastructure – Deployment of virtual network functions (VNFs) close to the customer reduces latency, improving quality of experience (QoE); enables higher security (especially for mission-/safetycritical applications); and provides local data termination to relieve backbone network traffic.

- Disaggregation of hardware (HW) and software (SW) – Unbundling of HW and SW (i.e., using commercial offthe-shelf compute storage and networking hardware) is nothing new, yet it only recently gained general exposure across networking equipment (especially in radio access networks [RANs]) to enable CAPEX reduction and sourcing diversification.

- “Softwarization” and virtualization of network functions – End-to-end software-defined networks (SDNs) allow for the scalability and automation required for future 5G use cases.

- Open interfaces – Standardization of application programming interfaces (APIs) between, as well as within, network domains allows for vendor competition, hence innovation at lower total cost of ownership (TCO).

- Containerization of software – Moving from dedicated servers and virtual machines (VMs) to containers on “bare metal” (i.e., running VNFs on a significantly reduced stack) to further increase efficiency and hardware usage and to drive scalability of the network (see Figure 1).

Although some of these trends have been around for some time, we now see three key market trends acting as catalysts for the large-scale adoption of these technologies in the near future:

- Interoperability of vendors within and between the individual network domains (RAN, transport, core and orchestration) is developing at a rapid pace based on standardizations such as Open RAN (O-RAN Alliance).

- As a consequence of this expansion, the vendor landscape has drastically broadened, leading to the availability of competitive solutions for all network domains on the market, thereby fostering a clear paradigm shift of traditional as well as “new” network equipment providers (NEPs) to move from monolithic telecom network infrastructure to softwarebased IT solutions.

- We consider integration efforts and risk for decoupled and disaggregated solutions to be reasonable given expected network TCO savings of up to 40 percent and the establishment of an ecosystem of suitable integration partners.

Leading operators across the globe have already taken the first steps toward these target networks, as illustrated in Figure 2.

Although virtualization concepts and subsequent target network architectures remain at an early stage of development, the first live deployments – such as those by Rakuten in Japan, AT&T in the US or Telefonica in selected markets – clearly indicate performance improvements over distributed/centralized network architectures across domains.

As an example of these improvements, time to market (TTM) for incremental network deployments (mobile sites) as well as for new 5G services such as URLLC or mMTC can be reduced from the current requirement of several days to just a few hours.

Moreover, virtualization and cloudification allow organizations to provide better QoE through continuous integration (CI)/ continuous delivery (CD) and fully automated self-provisioning and self-optimizing network (SON) functions. Figure 3 compares key performance metrics between distributed, centralized and virtualized network deployment models along the customer journey.

With a broadening vendor landscape, higher interoperability and performance improvements along the customer journey, operators such as Rakuten, China Mobile and T-Mobile US that deploy virtual RAN (vRAN)/Open RAN (oRAN) solutions realize network TCO savings of up to 44 percent compared to traditional distributed/centralized RAN setups (D-RAN/C-RAN).

Whereas CAPEX can be reduced by up to 50 percent due to vendor competition across domains, OPEX savings of up to 53 percent mainly come from efficiencies in deployment and operations, such as zero-touch automation (see Figure 4).

2

How can virtualization be executed across network domains?

To realize the benefits of virtualization, organizations must revisit mobile network architectures across domains and explore the organizational changes and alterations of traditional sourcing models that are required. Next, we outline the key concepts for main mobile network sections.

Radio access network – achieving openness through virtualization

RAN assets are typically the largest investment for the mobile network and are the most rigid and costly to operate and transform. Thus, it is vital that they are made increasingly agile and more cost-efficient. The evolution we see in RAN includes centralization, virtualization and openness (see Figure 5):

- Centralization and virtualization for leaner cell sites.

- RAN disaggregation for improved efficiencies and CEX.

- Openness for vendor diversification.

Centralization and virtualization for leaner cell sites

Avoiding dedicated baseband units (BBUs) at each site allows mobile operators to create centralized BBU pools, driving leaner cell sites that are easier to deploy and maintain. This is a key driver for lowering CAPEX by reducing individual cellsite requirements for shelter and cooling, and the nascent operational effort to maintain equipment-heavy cell sites, as opposed to fewer, centralized locations.

RAN disaggregation for improved efficiencies and CEX

BBUs are shifting from a physical toward a virtual resource and can be further split into virtual distributed units (vDUs) and virtual centralized units (vCUs). Virtual BBU (vBBU) resources can ultimately be more efficiently allocated, increasing average equipment utilization as a lever to reduce necessary CAPEX and improving CEX by reducing the risk of congestion. Virtualization also enables scalability, automaticity and faster adoption of changes (updates or vendor swaps).

Openness for vendor diversification

RAN virtualization facilitates the implementation of open interfaces (oRAN), leading to use cases, such as deploying separate vendors for active antenna units (AAUs) and vBBUs (or vCUs and vDUs), using commercial off-the-shelf (COTS) hardware for vRAN software, or mixing different RAN vendors within the same geographic footprint. Such a multi-vendor setup allows organizations to leverage best-in-breed solutions for each network component while lowering RAN CAPEX through increased vendor competition and reduced reliance on proprietary hardware.

Transport – DC hierarchy and new protocols to enable virtualization

Virtualization and disaggregation of RAN architecture necessitates rethinking how transport and DC infrastructure is deployed and operated (see Figure 6). The evolution for mobile operations includes:

- Distributed DC hierarchy to allow for RAN virtualization.

- SDN up to active antenna units (AAU) for increased controllability and automation.

- Fiberization for future-ready capacity.

Distributed DC hierarchy to allow for RAN virtualization

RAN centralization and virtualization entails cloud infrastructure at the edge. This opens an opportunity for companies to offer latency-sensitive use cases, such as autonomous driving, interactive augmented reality/virtual reality and holographic communications. To achieve this, hundreds, if not thousands, of mini-DCs must be deployed closer to the user. While the buildout effort and change in operating model of the DC infrastructure may seem significant at first, the effort is a fundamental step to unlocking large TCO savings from open and virtualized RAN, as well as to increasing differentiability with better QoE and available services.

As an example, whereas in a classical D-RAN concept each cell site has a dedicated BBU, in a centralized and virtualized network multiple BBUs are consolidated into centralized far-edge DCs and hosted as VNFs, eliminating significant amounts of remote equipment, located on the site, and thereby reducing the overall equipment required, as well as associated maintenance efforts.

The distributed DC infrastructure would also be shared as the basis for all necessary network intelligence coming from RAN, core or other telco domains (e.g., content delivery networks, multi-access edge computing or fixed service).

SDN up to AAU for increased controllability and automation

As a result of RAN virtualization, two new transport domains emerge – fronthaul and midhaul – in addition to the regular mobile backhaul. The Common Public Radio Interface (CPRI) protocol to connect AAUs and BBUs is ill-equipped for larger fronthaul distances. Instead, new eCPRI and IEEE-defined protocols, running on Ethernet, are necessary. To ensure competitive quality of service despite growing user traffic and end-to-end orchestration, operators – and vendors – need to extend SDN controllability and automation to fronthaul transport.

Fiberization for future-ready capacity

The traffic and latency requirements of current and future 5G use cases demand a rapid increase in fiberization to cell sites. While fiber is a heavy investment, it ensures long-term capacity of the transport medium (unlike microwave, which requires frequent upgrades). Operators can approach fiber investment in an intelligent way by decreasing fiber usage per site, either at the level of transport equipment (WDM or L2/L3 switches) or at an architectural level via “ring-structure” of the fronthaul transport as opposed to the typical “star”-shaped structure of current backhaul. This approach will significantly reduce upfront investment into backhaul transport, while ensuring enough capacity to deliver user traffic demand and quality of experience. With an average of around 35 percent of TCO across most recent 5G deployments, fiberization of cell sites will remain a key investment driver for any operator.

Core - distributed VNFs for critical 5G use cases

The core network is increasingly becoming disaggregated, virtualized and distributed, enabling a more agile, efficient and performant network that enables 5G-promised use cases. This is mainly driven by three key factors:

- Microservice-based architecture for critical 5G use cases.

- Containers on “bare metal” for further efficiency.

- Transition to distributed core systems.

Microservice-based architecture for critical 5G use cases

Especially in the context of URLLC and mMTC, organizations must tailor services to specific use cases. To enable these differentiated services, network functions in the packet core will be decoupled into individual microservices. Operators can enhance the quality of service by catering to the demand of each use case, while at the same time optimizing the usage of network resources.

Containers on “bare metal” for further efficiency

Moving toward a microservices-based architecture requires more scalability and simplification in the orchestration of the packet core. Hence, an evolution toward containers on “bare metal” will be an inevitable step. Containerization allows core VNFs to scale-in faster and in a more cost-efficient way (compared to VMs) by significantly reducing the required underlaying physical resources and time.

Transition to distributed core systems

The combination of two trends – microservices and containerization – will allow operators to move from a centralized toward a distributed core network. The latter means dynamic and real-time deployment of microservices anywhere in the network, based on the distinct requirements of a service provided to a specific customer. Automation will allow the customer to directly initiate these services, enabling selfservice, mass customization and faster provisioning.

Orchestration and automation – moving toward “zero-touch” operations

Last but not least, to achieve a design that meets operators’ business objectives, the target mobile network architecture requires advancements in automation and end-to-end orchestration. Specifically, we see the following three key trends driving end-to-end automation and orchestration (see Figure 7):

- Integration of separate domains to a single orchestration system.

- From rule-based to artificial intelligence (AI)-based orchestration.

- Self-provisioning of services for full automation.

Integration of separate domains to a single orchestration system

Current network operations are based on configuration and monitoring of separate systems – or “silos” – that must be patched together to achieve automation and end-to-end service provisioning. Hence, future networks will move from this isolated approach toward achieving true orchestration. The journey requires initially combining various systems into “domains” (e.g., mobile and transport) and eventually achieving cross-domain orchestration via open APIs. This cross-domain orchestration will enable not only a path to true automation, but also the necessary capabilities for complex and dynamic services, such as network slicing, while maintaining the necessary quality of service across heterogenous underlying network systems.

From rule-based to AI-based orchestration

Current automation is typically achieved via pre-established templates of configurations or, in the best case, rule-/policybased automation. These types of automation often face a mismatch between the goals and results of the rule or template, requiring additional manual adjustments. Closed-loop automation would feedback from the results of actions and selfadjust to achieve a target result (e.g., service quality) rather than a target action.

Telcos’ end goal is “zero-touch” operations, enabling significant OPEX reductions and better real-time optimization of network performance. AI is a necessary tool to achieve the degree of automation that is required. Presumably, only AI-supported systems would be able to navigate the complex relations of network components. Without AI, it is unlikely that organizations can achieve the dynamic service orchestration and scaling at the network’s edge or network slicing.

Self-provisioning of services for full automation

With this level of automation, our understanding of connectivity provisioning will shift to service-centric orchestration, which allows for automated provisioning of on-demand services triggered and configured directly by the customer. Selfconfiguration enables a whole new playing field for operators around differentiability, tapping into new customer segments and further optimization potential across other commercial or technical company units. Customer-facing self-service portals, enabling customer-defined service parameters at low production cost and fast deployment, will be a new differentiator enabled for early adopters and a basic expectation in the long run.

Network security – increased protection through trusted platforms and tenant isolation

Virtualization fundamentally changes the risk profile of mobile networks. Whereas in physical networks the largest security threat came from an “arms race” of malware with increasingly professionalized “toolkits,” virtualization exposes network functions to IT security threats that have not been present before. Moreover, the usage of COTS hardware prevents vendorlevel security encryption (a trusted execution environment), and multi-tenant use of physical infrastructure (i.e., slicing, third-party apps) creates risks for security “backdoors” between different security grade systems.

Yet along with the emergence of network function virtualization, preventive security measures are improving as well. Concepts such as trusted platform encryption between HW and vBBU and tamperproof hardware design for vBBUs have significantly improved security levels in the RAN domain. In addition, the extension of IPSec and MACSec to edge and far-edge data center locations has provided further protection to the transport network. Tenant isolation and full network transparency, among others, elevate security levels in the core and systems domains (see Figure 8).

Conclusions

With changing customer requirements and increasing competition, now is the time for telcos to transform their mobile networks. Telecom operators should make use of new technologies to transition from legacy network architecture to a flexible, virtual, open and automated network that is more resilient and programmable, enabling adjustment in the face of unforeseen future market demands.

Time will tell if telcos can achieve such a transition while managing the migration effort efficiently. It is our strong belief that such a shift requires not only significant financial and operational investment but also a transformation in the organizational setup and capabilities. Telcos will no longer be able to source and operate in their usual mode of plan – build – run. In particular, this transition will have two major impacts on organizations:

- Telco operators must rethink their sourcing strategy. Disaggregation of hardware and software in combination with subsequent network function virtualization allows for moving toward greater vendor diversity and ultimately raises the strategic question of whether to buy pre-integrated solutions from traditional network equipment providers or to source highly specialized IT-based solutions from upcoming “new kids on the block” vendors. To answer this question, operators must weigh cost and risk profiles versus openness, agility and innovativeness of their target network designs.

- Mobile operators will no longer be able to work in separate silos (e.g., with isolated teams for RAN, transport, core and systems). Rather, organizations will have to establish a “network architecture” team responsible for the orchestration of the entire network and to increase cross-segment coordination. Moreover, telco operators will need to broaden the technical capabilities of their network teams. These include those competencies associated with IT in order to orchestrate the cloudification of all network segments and establish new, iterative cycles of working as opposed to rigid plan-build-run cycles.

In our 2019 report “Who Dares Wins!” Arthur D. Little covered how CxOs, as well as operational and commercial teams, can address some of the challenges of virtualization. In subsequent articles in this series, we will explore these implications in more detail and share best practices of mobile network operators from around the globe that have embarked on this journey. Stay tuned!

DOWNLOAD THE FULL REPORT